Georgia Car Insurance: Requirements, Costs, and How OCHO Helps You Pay Less Up Front

Finding affordable car insurance in Georgia can feel like navigating rush hour on I-285, confusing, frustrating, and expensive. With rates running well above the national average and large down payments creating barriers for working drivers, understanding your options matters more than ever. This guide breaks down everything you need to know about Georgia auto insurance: what the law requires, what coverage actually protects you, and how OCHO makes it easier to get covered without draining your bank account upfront.

Plus, buying your policy online is fast and convenient, and you could save up to 12% when you buy customized car insurance online.

Introduction to Car Insurance

Auto insurance is a financial safety net for drivers in Georgia. It’s designed to protect you, your vehicle, and others on the road from the high costs that can come with accidents, theft, or unexpected damage. In Georgia, having car insurance isn’t just a smart move, it’s the law. Every driver must carry at least the minimum auto insurance requirements to legally operate a vehicle on public roads.

The right insurance coverage can shield you from paying out of pocket for repairs, medical bills, or property damage after an accident. But the cost of car insurance in Georgia can vary widely. Factors like your age, where you live, your driving record, and even the type of car you drive all play a role in determining your premium. For example, younger drivers or those living in busy cities like Atlanta may see higher rates, while experienced drivers in smaller towns might pay less.

Fortunately, there are ways to find affordable car insurance rates that fit your budget. Many insurance providers in Georgia, such as Liberty Mutual, offer customizable policies so you only pay for the coverage you need. By shopping around and comparing options, most people can save money and still meet the state’s minimum auto insurance requirements. Whether you’re a new driver or just looking to lower your costs, understanding your options is the first step to getting the best value on car insurance in Georgia.

Quick answer: What drivers in Georgia need to know right now

Georgia is a “fault” state, meaning the driver who causes an accident is responsible for the resulting damages. Georgia operates under a traditional tort (at-fault) system, allowing victims to seek compensation for damages from the at-fault driver. The state requires all drivers to carry liability insurance, and costs here run noticeably higher than the national average.

As of 2024, Georgia’s minimum auto insurance requirements are 25/50/25—that’s $25,000 bodily injury liability per person, $50,000 bodily injury per accident, and $25,000 accident property damage liability per accident.

Average annual full-coverage car insurance in Georgia runs around $2,500–$2,600, roughly 15–20% higher than what most people pay nationally. The average cost of car insurance in Georgia was $2,572 in 2024 according to thezebra.com, and this is 18% higher than the national average.

Many Georgia drivers struggle with large down payments that insurers demand upfront. OCHO lets qualified drivers start policies with as little as $0 down through interest-free financing.

Ready to see what you’d pay? Enter your Georgia ZIP code—whether you’re in Atlanta (30303), Savannah (31401), Augusta (30901), or anywhere in GA—to compare real-time quotes with OCHO. You can also get a Georgia auto insurance quote from GEICO right from your computer.

Cheap auto insurance is available for Georgia drivers who compare providers and coverage options.

Thank you! Your submission has been received!

Oops! Something went wrong while submitting the form. Please try again later.

What car insurance is required in Georgia?

Georgia law (Title 33 and Title 40 of the Official Code of Georgia Annotated) requires all vehicles driven or parked on public roads to carry active liability insurance. You cannot legally operate a vehicle in the state without proof of coverage.

The three core required coverage types are:

Bodily Injury Liability – Pays for medical expenses, lost wages, and related costs when you injure someone in an at-fault accident

Property Damage Liability – Covers repairs to vehicles, fences, buildings, or other structures you damage

Uninsured Motorist (UM/UIM) – Optional but extremely common given Georgia’s estimated 10–15% uninsured driver rate

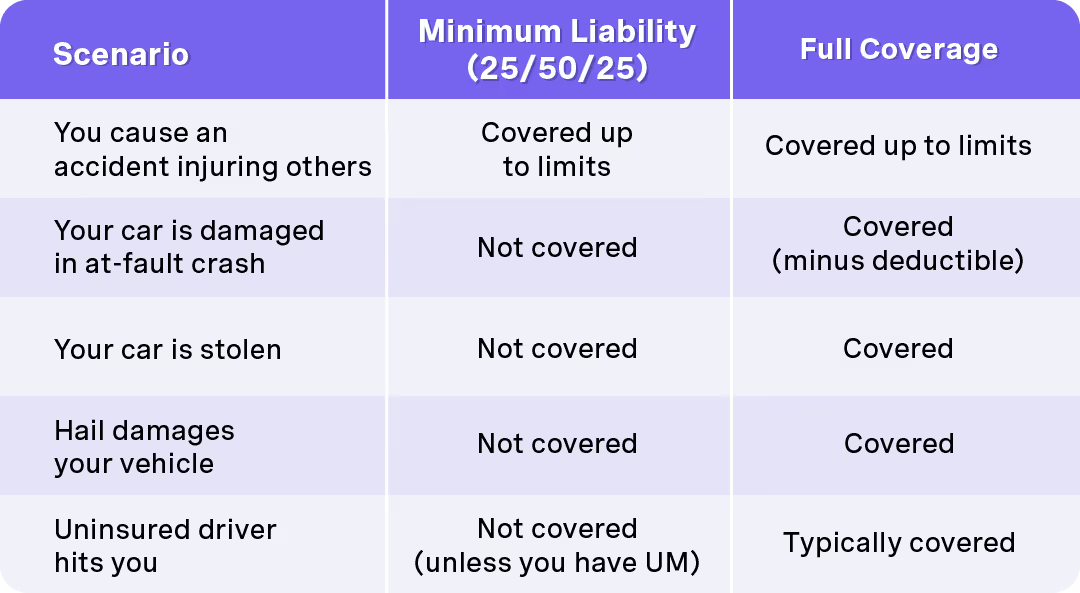

Here’s the key distinction: liability coverage pays for injuries and property damage you cause to others. It does not pay for your own car repairs or your medical bills. That’s a surprise to many drivers who assume their policy protects everything.

Because Georgia is a fault state, the at-fault driver’s insurance typically pays for the other party’s losses. Consider a rear-end collision on I-285 in Atlanta during morning commute traffic. If you’re found at fault, your liability insurance would cover the other driver’s vehicle repairs and medical bills—but not your own.

Or imagine a fender-bender in downtown Macon where you back into a parked car. Your property damage liability would cover repairs to that vehicle, but you’d pay out of pocket for your own bumper damage unless you carry additional collision coverage.

Georgia minimum liability limits (25/50/25)

Georgia’s current legal minimums as of 2024 are:

$25,000 bodily injury per person

$50,000 bodily injury per accident

$25,000 property damage per accident

These are minimums, not recommendations. Many drivers choose higher limits—like 50/100/50 or 100/300/50—to protect their home, savings, and wages from lawsuits exceeding their coverage.

Here’s a simple example: You cause an accident that sends two people to the hospital with injuries totaling $60,000 combined. Your 25/50/25 policy covers up to $50,000 per accident for bodily injury. That leaves $10,000 you’re personally responsible for—money the injured parties can pursue through lawsuits against your personal assets.

With today’s medical costs and vehicle repair expenses (modern cars with sensors and advanced safety systems can easily exceed $25,000 in repairs from a moderate collision), many insurance industry experts recommend limits of at least 100/300/100 for adequate security.

The Georgia Office of Insurance and Safety Fire Commissioner publishes official state requirements. While the 25/50/25 minimums have remained stable for years, drivers should verify current requirements when purchasing or renewing policies.

Optional coverages Georgia drivers should consider

While only liability is required by law, lenders and lessors often require additional coverages to protect their collateral. Many Georgia drivers also opt for more protection simply because minimum coverage leaves too much exposed.

Full coverage – Full coverage typically includes comprehensive and collision insurance, as well as uninsured or underinsured motorist insurance, providing broad financial protection in a variety of accident scenarios.

Collision insurance – Pays to repair or replace your vehicle after a crash, regardless of fault. Whether you hit a guardrail on I-75 or another driver rear-ends you, collision insurance covers your car’s damage minus your deductible. It is a key component of full coverage, helping protect you from costly repairs after an accident.

Comprehensive coverage – Pays for non-collision events: theft (a significant concern in metro Atlanta), vandalism, hail damage in North Georgia, falling trees after storms, or hitting a deer in rural counties like Walker or Coffee. Comprehensive coverage pays for damage caused by anything other than a collision.

Uninsured/Underinsured Motorist (UM/UIM) coverage – With Georgia’s high rate of uninsured drivers, this coverage matters. It protects you when an at-fault driver has no insurance or not enough insurance to cover your damages.

Medical Payments (MedPay) – Helps with hospital bills for you and your passengers, regardless of fault. This can be especially valuable if you have high-deductible health insurance.

These options are how Georgia drivers achieve what’s commonly called “full coverage”—and they’re essential for protecting both your vehicle and your finances, especially if you drive a newer car or have limited savings to absorb unexpected costs.

“Full coverage” in Georgia: What it usually includes

“Full coverage” isn’t a legal term in Georgia. There’s no official definition in state law. However, most people and insurance professionals use it to describe a policy that includes:

Liability coverage (often at higher limits than 25/50/25)

Collision coverage

Comprehensive coverage

Uninsured/Underinsured Motorist (UM/UIM)

Sometimes Medical Payments (MedPay)

For example, a typical full-coverage package for a financed 2021 Toyota Camry in Atlanta might include 100/300/100 liability limits, $500 deductibles for collision and comprehensive, and UM/UIM matching the liability limits.

Why these extras? Lenders and leasing companies require collision and comprehensive until the loan or lease is paid off. They need assurance that their collateral can be repaired or replaced if something happens.

State-minimum liability only vs. full coverage:

(February 2026)

What does Georgia car insurance cost in 2024?

Average annual full-coverage premiums in Georgia hover around $2,500–$2,600 as of 2024—significantly above the national average. That translates to roughly $200–$220 per month for comprehensive protection.

Minimum-liability-only coverage can be much cheaper, often around $900–$1,300 per year for a clean-driving adult. But remember: that bare-bones policy offers far less protection and leaves you personally exposed for your own vehicle and injury costs.

Geographic location makes a major difference. Big metro areas like Atlanta, Savannah, Columbus, and Augusta tend to have higher rates than smaller towns. More traffic means more accidents. Higher population density means more theft and vandalism claims.

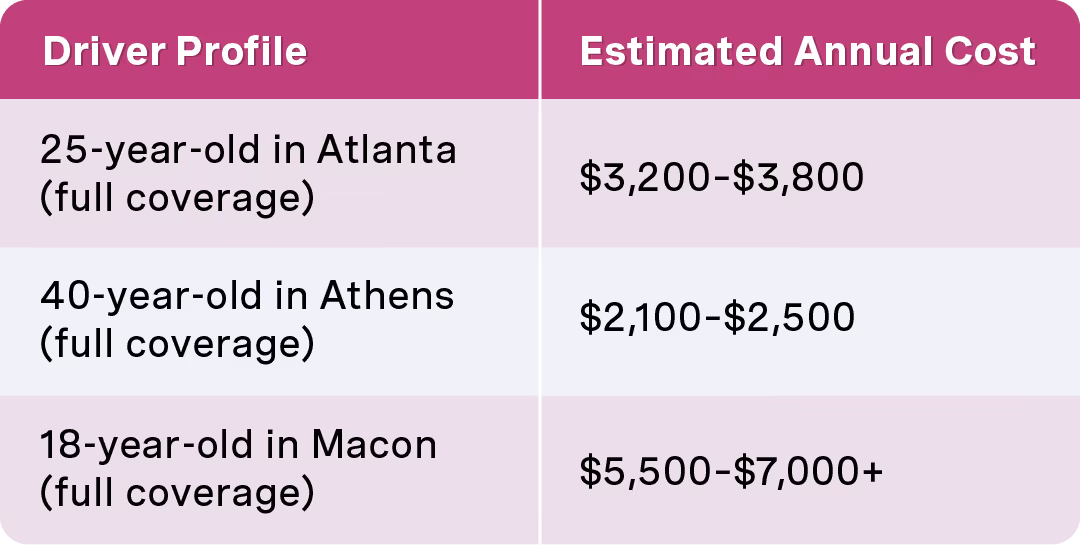

Estimated yearly costs by driver profile:

(February 2026)

Age and location combine to create dramatic price differences. A young driver in a major metro area faces premiums that can exceed what some drivers pay for their actual car payment.

OCHO doesn’t set these insurance prices—carriers do. What OCHO does is help shoppers compare real-time quotes from multiple insurers, then smooth out those demanding upfront costs with flexible payment options that align with your budget.

Factors that influence your Georgia auto insurance rate

Insurance companies consider multiple factors when calculating your premiums:

Age – Younger drivers (especially under 25) pay significantly more due to inexperience

Driving record – At-fault accidents, DUIs, and speeding tickets sharply raise rates

Credit-based insurance score – Where allowed, insurers use credit history as a rating factor

ZIP code – Fulton and DeKalb counties typically cost more than rural areas

Vehicle type – Newer cars with expensive parts and advanced tech cost more to insure

Annual mileage – More time on the road means more exposure to risk

Coverage level – Higher limits and lower deductibles increase premiums

Prior insurance history – Lapses in coverage can trigger higher rates

Georgia-specific factors matter too. A driver with a clean record in Savannah might pay $1,800 annually, while a similar driver with one at-fault accident in the past three years could face $2,800 or more—a 55% increase that lasts for years.

High risk drivers with multiple violations or DUIs may find themselves paying double or triple standard rates, making affordable insurance rates even harder to achieve.

Who has cheap car insurance in Georgia—and what “cheap” really means

No single company is cheapest for every Georgia driver. Rates vary dramatically based on your specific profile, city, car type, and credit. State Farm might offer the best rate for one driver while GEICO beats everyone for another.

Chasing the absolute lowest price can backfire. That rock-bottom quote might mean:

Bare-minimum 25/50/25 limits that leave you exposed

Sky-high deductibles you can’t afford if you file a claim

A company with poor claims service when you actually need help

Instead of calling every carrier individually, OCHO works as a broker that lets you compare prices from multiple insurers side by side in real time. You see your actual coverage options and costs in one place.

Consider a driver in Atlanta comparing a bare-minimum 25/50/25 policy at $85/month versus a 50/100/50 policy at $98/month. That extra $13 monthly buys substantially more protection—money that could save thousands if you’re ever in a serious accident.

Cheap liability-only policies can leave you devastated financially. Total a newer vehicle? You’re still making payments on a car you can’t drive. Cause injuries exceeding your $25,000 per person limit? The injured party can sue for your personal assets.

Smart coverage means meeting Georgia legal requirements while not creating financial catastrophe after an accident.

How OCHO helps make Georgia car insurance more affordable

OCHO’s core value is simple: we split that large upfront down payment into smaller, interest-free installments aligned with your pay cycle. Qualified drivers can often start coverage with $0 down. In Georgia, the average downpayment for auto insurance is $445.30. With OCHO, that same deposit goes down to $222.85. The same quality coverage, just less costs straight away.

Here’s how it works:

OCHO partners with established insurers, so you get the same coverage you’d receive directly from major carriers

No late fees for approved schedule changes when life happens

Extra time to pay when needed, helping working-class drivers avoid lapses and cancellations

On-time payments can support credit-building for drivers with thin or imperfect credit files

Real scenario: A rideshare driver in Atlanta needs coverage to stay on the road and earning. The insurer wants $600 down. That’s a week’s worth of income he can’t afford to part with at once. With OCHO, he spreads that $600 across smaller installments aligned with his weekly earnings—getting instant proof of insurance today without the cash crunch.

Want to check your eligibility and see quotes? The process won’t affect your credit score, and you’ll see exactly what you qualify for before committing to anything.

Georgia penalties for driving without insurance

Driving without insurance in Georgia is a misdemeanor offense. The consequences go far beyond a simple traffic ticket.

First-time offenders may face:

Fines up to approximately $1,000

Potential jail time up to 12 months

Suspension of vehicle registration

Suspension of driver’s license

Reinstatement fees often exceeding $200

Driving without a valid driver's license or allowing your license to be suspended due to lack of insurance can result in additional penalties, including further fines or even jail time.

Georgia requires electronic verification of insurance coverage. When you purchase a policy, your insurer reports it to a state database. If your coverage lapses—even briefly—the system flags it automatically, triggering notices and potential penalties without anyone pulling you over. Many insurers do not cover drivers who found themselves without insurance for six months or more, but that's not an issue at The General.

Being caught in an at-fault accident without coverage creates even worse consequences. Injured parties can sue you personally. Courts can garnish wages. The financial damage can follow you for years.

Example: A driver is stopped in DeKalb County for speeding. The officer runs her plates and finds no active insurance coverage. Now she faces the speeding ticket plus a no-insurance citation, potential license suspension, mandatory SR-22 filing for high risk drivers, and court costs. What started as a minor traffic violation becomes a $2,000+ problem.

OCHO’s flexible payment plans help Georgia drivers avoid exactly this situation. When you can afford your down payment in smaller chunks, you’re less likely to let coverage lapse because you can’t pay that big renewal deposit.

Special rules and tips for Georgia drivers

Georgia has specific laws that interact with your insurance needs in practical ways.

Georgia is a “comparative negligence” state. In an accident, fault can be shared between drivers. If you’re found 20% at fault and the other driver is 80% at fault, your claim payout is reduced by your 20% share. This makes having enough insurance even more important—you may collect less than full damages even when you’re mostly not at fault.

Law enforcement in Georgia can verify your insurance coverage electronically during traffic stops or after crashes. While you should still carry proof of insurance (digital proof on your phone is accepted), officers have access to the state database to confirm your coverage status.

Uninsured motorist coverage can be rejected in Georgia—insurers must offer it, but you can decline. Think carefully before doing so. Medical bills and repair costs add up fast, and if an uninsured driver hits you, UM/UIM coverage may be your only financial protection.

Georgia laws for teen drivers

Georgia’s Graduated Driver Licensing (GDL) system creates a structured path for new drivers:

Age 15 – Instructional permit (must hold for at least 12 months and complete 40 hours supervised driving)

Age 16–17 – Class D intermediate license (some permit or license conditions, such as holding a clean record, may have a six-month duration before certain restrictions are lifted)

Age 18 – Full Class C license

School attendance and conduct can impact driving eligibility for teenagers in Georgia, as students may lose their license or permit if they are not enrolled in school or have serious disciplinary issues.

Joshua’s Law requires teens under 18 seeking a Class D license to complete an approved driver education course and log supervised driving hours. This law exists because teen drivers face significantly higher accident rates.

Intermediate license holders face restrictions:

No driving between midnight and 6 a.m. (with limited exceptions)

No more than 3 passengers under 21 who aren’t family members

No cell phone use, even hands-free

Adding a teen driver to your policy can dramatically increase premiums. In Gwinnett County, a family might see their annual premium jump from $2,400 to $4,200 when adding a 17-year-old—a 75% increase.

Comparing quotes through OCHO when adding a teen helps manage this cost shock. Different insurers weight teen driver risk differently, so shopping around matters more than ever.

Georgia registration and proof of insurance

New residents must register their vehicles and usually obtain a Georgia title within 30 days of establishing residency. Missing this deadline can result in penalties.

Key registration requirements:

Most vehicles model year 1986 or newer require a Georgia certificate of title before registration

Your county Tax Commissioner’s Office typically handles registration

Many counties require new residents to appear in person

You’ll need proof of insurance in Georgia to complete registration

Georgia’s electronic insurance database means any lapse in coverage gets flagged automatically. The state sends notices, and continued lapses lead to registration suspension and reinstatement fees.

OCHO provides instant digital proof of insurance that works for registration at your county office and satisfies verification at traffic stops. No waiting for cards in the mail—you’re covered and can prove it immediately.

First Car Owners: Tips and Advice

Getting your first car is an exciting milestone, but it also comes with new responsibilities—especially when it comes to car insurance. If you’re a first-time car owner in Georgia, here are some essential tips to help you navigate the world of auto insurance and make smart, affordable choices.

1. Know the State Requirements:Before you hit the road, make sure you understand Georgia’s minimum auto insurance requirements. You’ll need liability insurance to legally operate your vehicle, but it’s wise to consider additional coverage options like collision or comprehensive coverage for extra protection.

2. Shop Around for Affordable Car Insurance: Don’t settle for the first quote you receive. Insurance rates can vary significantly between companies, so compare multiple auto insurance quotes to find the most affordable car insurance rates for your situation. Online tools and brokers like OCHO make it easy to see your options side by side.

3. Consider Your Coverage Needs:While it might be tempting to choose the cheapest policy, make sure you have enough insurance to cover your assets and protect yourself in case of an accident. Think about your vehicle’s value, your budget for deductibles, and whether you need coverage for theft, vandalism, or uninsured drivers.

4. Understand What Affects Your Premium: Factors like your age, driving history, location, and even your credit score can impact your insurance costs. Safe driving, maintaining a clean record, and taking a defensive driving course can help you qualify for discounts and save money.

5. Ask About Discounts:Many insurers offer discounts for things like bundling policies, having good grades (for students), or installing safety features in your car. Don’t be afraid to ask what you qualify for, every bit of savings helps.

6. Keep Proof of Insurance Handy:You’ll need to show proof of insurance when registering your car, during traffic stops, or after an accident. Most companies now offer digital proof you can keep on your phone for convenience.

Owning your first car is a big step, but with the right information and a little research, you can find affordable car insurance in Georgia that keeps you protected and on the road with confidence.

Thank you! Your submission has been received!

Oops! Something went wrong while submitting the form. Please try again later.

How to compare Georgia car insurance quotes with OCHO

Getting covered through OCHO follows a simple process:

Enter your Georgia ZIP code – Whether you’re in Atlanta, Savannah, Augusta, Columbus, or a rural county

Answer basic questions – About yourself, your driving history, and your vehicle

Choose your coverage level – From state-minimum liability to comprehensive full coverage

Review real-time quotes – See options from multiple partner insurers side by side

Select a plan and payment schedule – Pick what works for your budget

Customers can conveniently purchase their policy online, making the process fast and easy.

Because OCHO is a broker, not a single insurer, you see options from multiple companies at once. No calling around. No filling out the same information repeatedly. OCHO and its partner insurers are known for building long-standing relationships and providing personalized service to customers.

When reviewing insurer options, note that The General's mobile app allows customers to manage their policy, report claims, and make payments easily.

Once you choose a policy, OCHO helps break up the insurer’s required down payment into smaller, interest-free installments. Whether you’re paid weekly, biweekly, or monthly, your payment schedule can align with when money actually hits your account.

Qualified drivers can start coverage with $0 or low money down while receiving instant proof of insurance. You’re legal on Georgia roads immediately, with a payment plan you can actually afford.

When considering coverage, The General offers full coverage that includes comprehensive and collision insurance, as well as uninsured or underinsured motorist insurance.

Ready to see your options? Georgia drivers from Atlanta’s busiest interstates to Savannah’s historic streets to Augusta’s suburban neighborhoods can save hundreds on upfront costs while getting the coverage they need.

Enter your ZIP code now to get your auto insurance quote and discover how OCHO makes car insurance in Georgia work for your budget—not against it.

Thank you! Your submission has been received!

Oops! Something went wrong while submitting the form. Please try again later.

Georgia Driver Resources

New to Georgia?

New residents have 30 days to:

Register their vehicle in Georgia

Obtain a Georgia driver's license

Secure Georgia auto insurance

Teen Drivers

Instructional permit at age 15

Intermediate license at age 16 (with Joshua's Law requirements)

Full license at age 18

Special Considerations for Georgia Cities

Metro Atlanta Region

Highest insurance rates in the state due to population density

Complex highway systems (I-75, I-85, I-285) affect risk factors

Higher likelihood of accidents and claims

Significant traffic congestion impacts

Coastal Georgia

Storm and flood risks in Savannah and Brunswick areas

Seasonal tourist traffic considerations

Salt air exposure concerns

Hurricane preparation needs

North Georgia Mountains

Weather-related driving challenges

Rural road considerations

Wildlife collision risks

Limited repair facility access

Middle Georgia (Macon, Columbus)

Mixed urban and rural driving conditions

Military installation considerations

University area traffic patterns

Moderate insurance rates

Tips for Georgia Drivers

Maintaining Coverage in Georgia

Continuous coverage is crucial in Georgia for several reasons:

Avoid state penalties and license suspension

Maintain lower insurance rates long-term

Protect against the state's uninsured drivers

Keep your vehicle registration valid

Prevent gaps that could increase future rates

When to Update Your Coverage

Review your insurance when:

Relocating within Georgia

Adding new drivers to your household

Changing vehicles

Your commute distance changes

After life events like marriage or graduation

Following any traffic violations

OCHO's Georgia Commitment

We're dedicated to helping Georgia drivers navigate insurance requirements while keeping coverage affordable. Our local expertise means we understand:

OCHO understands that Georgia drivers need affordable options without compromising on coverage. Here are ways we help you save:

Payment Timing: Align insurance payments with your paycheck schedule

Coverage Bundling: Combine different insurance types for better rates

Safe Driver Benefits: Maintain a clean record for continued savings

Credit Building: Use on-time payments to potentially improve your credit score*

Flexible Down Payments: Options starting at $0 down for qualified drivers

Teen Driver Discounts: Special rates for completion of approved driver education courses

Multi-Car Savings: Cover multiple vehicles for additional discounts

Why Insurance Shopping with OCHO is the Smart Choice

At OCHO, we believe car insurance should be simple and fair for everyone. Ever had the experience of going through a whole quote process, only to have the cost jumping up at the last minute? That’s why we created OCHO PriceCheck—to help you find the best deal without the hassle. When it comes to buying car insurance in Georgia, guessing won’t save you money—comparing will. Instead of spending hours calling insurers or settling for the first quote you get, PriceCheck does the work for you, searching across multiple options to find the most affordable coverage.

On average, our Georgia customers save $544 when they use PriceCheck! Why overpay when a better deal is just a click away? Get real savings, real fast.

You'll see the PriceCheck button right before you lock in your final price.

Pay-As-You-Go Car Insurance in Georgia

For many Georgia drivers, traditional car insurance plans with monthly or annual payments can feel inflexible. We understand that you need payment options that fit around your life, so you can actually afford to have insurance without stressing about your other bills.

That’s why OCHO offers pay-as-you-go car insurance options designed to meet the needs of budget-conscious individuals. So it’s a standard, normal insurance policy, but we break it down for you into a customized payment plan that you can keep up with.

You get all the benefits of day by day insurance, but with a regular plan. Why is that a big deal? Well, it means that you have set, steady payments that you can rely on. A big problem with other pay-as-you-go plans is that the price can go up and down unexpectedly. It also means that you face the problem of having multiple cancellations. Cancellations can actually increase your insurance premiums by a lot.

With OCHO, you not only get an affordable pay-as-you-go plan, but we also give you extra days to pay when you need it most. This means that you get your insurance and you keep it. Protecting you from unfair price increases that you can and will incur from having cancellations on your record.

How OCHO’s Pay-As-You-Go Insurance Works

Small Payments: Manage your budget with smaller payments aligned with your paydays.

Low or No Down Payment: Begin your policy without breaking the bank.

Customizable Coverage: Select the level of protection that makes sense for you, without paying for extras you don’t need.

Flexible Plans That Build Stability: Consistent payments help you avoid coverage gaps and potentially qualify for lower premiums over time.

OCHO vs. Other Pay-As-You-Go Insurance

OCHO Pay-As-You-Go Advantages

Payments every two weeks (or whenever your paycheck is) to match your cash flow.

No coverage gaps—ensure continuous protection.

Transparent terms with no hidden spikes in fees.

Build credit with each payment.

Challenges with Other Companies

Unexpected price hikes and policy cancellations.

Less flexible payment timing.

Reduced opportunities to lower insurance rates.

At OCHO, we prioritize transparency and reliability, so you always know where your money goes.

Thank you! Your submission has been received!

Oops! Something went wrong while submitting the form. Please try again later.

Conclusion

Navigating car insurance in Georgia doesn’t have to be overwhelming or expensive. By understanding the state’s minimum auto insurance requirements, exploring your coverage options, and comparing quotes from multiple providers, you can find affordable car insurance rates that fit your needs and budget. Whether you’re a new driver, a first-time car owner, or simply looking to save money, tools like OCHO make it easier to get the coverage you need without a hefty upfront payment.

Remember, having the right insurance in Georgia isn’t just about following the law—it’s about protecting yourself, your family members, and your vehicle from life’s unexpected moments. Take the time to review your options, ask questions, and choose a policy that gives you peace of mind on every drive.

Ready to see how much you could save? Enter your Georgia ZIP code today to get your auto insurance quote and discover how OCHO can help you pay less up front while staying fully protected on the road.

Thank you! Your submission has been received!

Oops! Something went wrong while submitting the form. Please try again later.

Common Questions About Georgia Car Insurance

How much does car insurance cost in Georgia?

The average cost in Georgia is about $2,572 annually, but rates vary based on factors like location and driving history. OCHO offers affordable options with flexible payment plans to fit your budget.

Can I get car insurance with no down payment in Georgia?

Yes! OCHO specializes in $0 down payment options for Georgia drivers, making it easier to get the coverage you need today.

What is Georgia's Joshua's Law?

This law requires 16-year-olds to complete an approved driver education course and 40 hours of supervised driving (including 6 hours at night) to obtain a Class D license.

Who has the cheapest car insurance in Georgia?

While many companies claim to offer the cheapest rates, actual costs vary significantly based on individual factors. OCHO focuses on making insurance affordable through flexible payment plans, $0 down options, and personalized coverage solutions that fit your budget.

How much is car insurance in Georgia per month?

Monthly premiums in Georgia typically range from $100 to $250. With OCHO, you can split these payments into smaller bi-weekly amounts that align with your paycheck schedule, making coverage more manageable.

In Georgia, what are the requirements for liability car insurance?

Georgia requires minimum liability coverage of $25,000 per person/$50,000 per accident for bodily injury and $25,000 for property damage. OCHO can help you understand if these minimums are sufficient for your needs or if additional coverage would be beneficial.

Do you have to have car insurance in Georgia?

Yes, car insurance is mandatory in Georgia. Driving without insurance can result in fines, license suspension, and other penalties. OCHO makes it easy to stay compliant with flexible payment options and instant coverage.

Is Georgia a no-fault insurance state?

No, Georgia is an "at-fault" state, meaning the driver responsible for an accident is liable for damages.

Why Choose OCHO in Georgia?

Local Understanding: We know Georgia drivers' needs

Affordable Options: Flexible plans for every budget

Instant Coverage: Get insured today

Bilingual Support: English and Spanish assistance available

Digital-First Experience: Manage everything from your phone

Get Covered Today

Enter your ZIP code below to see how much you could save with OCHO's flexible Georgia car insurance options.

Thank you! Your submission has been received!

Oops! Something went wrong while submitting the form. Please try again later.

.svg)