The average full-coverage car insurance in the U.S. now runs between $2,100 and $2,700 annually, depending on which report you read. That’s a lot of money leaving your wallet every year. The good news? Smart choices can shave hundreds of dollars off your bill without leaving you exposed when things go wrong.

Auto insurance is more than just a legal requirement—it’s a crucial financial safety net for drivers. With car insurance premiums climbing above $2,000 a year for many Americans, understanding how auto insurance works is the first step to saving money. Insurance companies offer a range of coverage options, each designed to protect you from different risks on the road.

The three main types of coverage you’ll encounter are liability coverage, comprehensive coverage, and collision coverage. Liability coverage pays for injuries or property damage you cause to others, while comprehensive coverage protects your car from non-collision events like theft or weather damage. Collision coverage, on the other hand, helps repair or replace your car after an accident, regardless of fault.

Because insurance companies offer various discounts and incentives, knowing the basics of each coverage type can help you make smarter choices and lower your insurance costs. By comparing policies and understanding what you’re paying for, you can find ways to reduce your insurance premiums without sacrificing essential protection. Whether you’re buying insurance for the first time or looking to save money on your current policy, a little knowledge goes a long way toward getting the best deal on your car insurance.

Let’s skip the fluff and get straight to what works. Here are moves you can make this week to lower your car insurance premiums:

These aren’t theoretical savings. They’re based on actual market data from 2025 and align with many of the tactics outlined in a broader guide on how to get cheap car insurance with proven savings strategies. The rest of this guide digs deeper into each tactic so you understand exactly how to make them work for your situation.

Car insurance premiums vary by hundreds of dollars based on actuarial risk factors. Many insurers use sophisticated models to predict how likely you are to file a claim, which makes it crucial to understand how much car insurance should cost for your situation. The good news? You can influence many of these factors over time.

Your driving record matters most. A single speeding ticket raises rates 20–30% for three years. An at-fault accident can spike premiums 40–80% for 3–5 years. Maintaining a clean safety record qualifies you for safe driver discounts worth 15–25%.

Age and experience play big roles. Drivers under 25 pay 2–3x more than their parents due to inexperience. Older drivers over 70 may see 10–20% increases due to claim severity data. Rates typically normalize between ages 30–60.

Location affects your rate significantly. Urban ZIP codes with higher theft and crash frequency cost 30–50% more than rural areas. The difference between Miami and rural Florida can exceed $1,500 annually.

Vehicle factors include:

Other factors many insurers consider: Credit scores significantly impact rates in most states (though California, Hawaii, Massachusetts, and Michigan restrict this), marital status, and household drivers. Individuals with effective credit management tend to make fewer claims, which can result in lower insurance costs. Improving your credit score can lead to lower car insurance premiums, as many insurers use credit information to price policies; a dedicated guide on how your credit score affects car insurance rates can help you plan concrete steps.

Liability coverage is the foundation of any auto insurance policy, and it’s what protects you financially if you’re responsible for an accident. This coverage is split into two main parts: bodily injury liability, which pays for medical expenses and lost wages for other people injured in an accident you cause, and property damage liability, which covers repairs or replacement for someone else’s vehicle or property.

Most states require drivers to carry a minimum amount of liability coverage, but these minimums are often not enough to fully protect you in a serious accident. Insurance companies recommend higher limits to ensure you’re not left paying out of pocket for costly claims. For those who want even more protection, some companies offer umbrella policies that extend your liability coverage beyond the standard limits, providing extra peace of mind.

Understanding how liability coverage works—and why it matters—can help you make informed decisions when choosing or updating your auto insurance. Exploring real-life examples of why car insurance is important can also clarify how different coverage types protect you in costly situations. By selecting the right level of coverage, you can avoid unexpected expenses and ensure you’re meeting both legal requirements and your own financial needs.

Here’s a reality check: rates can differ by more than $1,000 per year between companies for the same driver and car. Using a complete guide to getting free auto insurance quotes can help you structure those comparisons and avoid common pitfalls. If your premiums have increased, switching carriers is a viable strategy for finding better rates, especially since many insurers offer senior discounts or enhanced coverage options. If you’re not shopping every 12–24 months, you’re probably overpaying.

Three ways to comparison shop:

Your step-by-step process:

Don’t just chase the lowest price. Check each company’s A.M. Best rating for financial strength (look for A++ like State Farm), review complaint history through your state insurance department, and scan customer reviews.

Timing matters: Start shopping 3–4 weeks before renewal. Many companies offer 5–10% early-quote discounts. Drivers with DUI or at-fault crashes might benefit from specialized carriers, but should still get multiple quotes.

Saving money on car insurance is about smarter coverage, not just buying the bare legal minimum. Underinsuring your liability coverage can be financially devastating—20% of claims exceed $100,000.

Recommended liability minimums: Most drivers should carry at least 100/300/100:

This costs only $200–$400 more annually than state minimums but provides vastly better protection.

Consider umbrella liability if you have significant assets. An extra $1 million in coverage typically costs $250–$300 per year when bundled with auto insurance.

When to drop collision and comprehensive coverage: Use this rule of thumb: if annual premium costs for these coverages exceed 10% of your car’s actual cash value, consider dropping them.

Example: A 2015 Ford Focus worth $4,000 with $500 annual comprehensive and collision coverage (12.5% of value) is a candidate for dropping. Potential savings: $800–$1,200 yearly.

Use Kelley Blue Book, NADA, or TrueCar to estimate your vehicle’s current value before making changes, and make sure you understand how car insurance covers theft through comprehensive coverage when deciding whether to keep or drop that part of your policy.

Review optional add-ons:

Two of the fastest ways to lower premiums: increase your deductible and claim every discount you qualify for.

The higher deductible math: Raising comprehensive and collision deductibles from $500 to $1,000 typically cuts those premium costs by 15–25%. On a policy where physical damage coverage runs $1,200 annually, that’s $180–$300 saved.

Critical requirement: Have an emergency fund that can cover your chosen deductible before making this change.

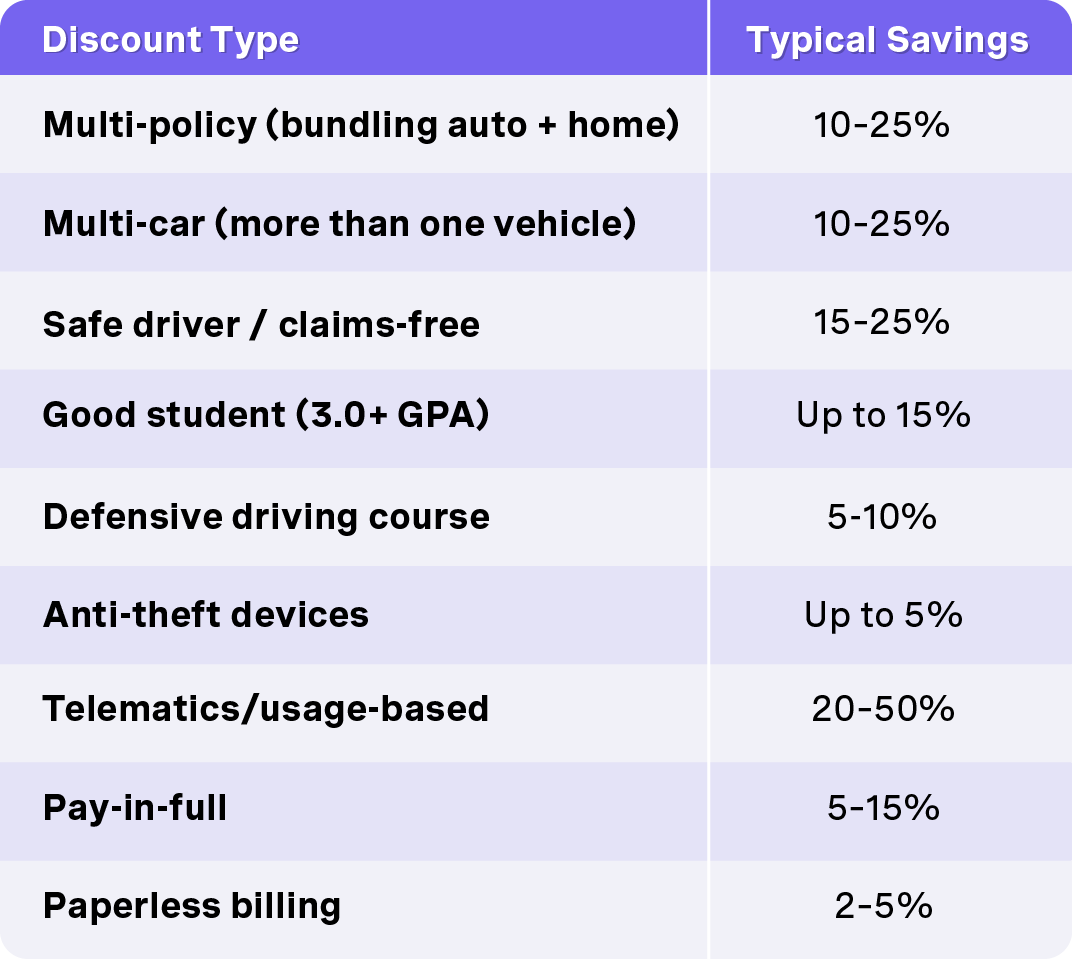

Insurer offers a wide range of discounts and benefits to help you save, including options like multi-car insurance for households with several vehicles:

Defensive driving course example: AARP’s 8-hour online course costs $20–30 and provides 5–10% off for three years. Many states require retaking every 3–5 years to maintain the discount. Your state insurance department website lists approved driver education courses.

Seeking hidden discounts for specific occupations or memberships can also provide lower rates.

Annual audit tip: Review your declarations page yearly to confirm all discounts remain applied. They sometimes drop off after system changes or renewal processing.

Insurance companies reward lower-risk usage patterns. Aligning your insurance policy with actual driving habits generates real savings.

Low-mileage tiers:

If you work from home, retired recently, or shortened your commute, report updated mileage immediately. Changes in your driving habits, such as driving less, can lead to lower car insurance premiums.

Telematics programs monitor braking, acceleration, time of day, and mileage. Good drivers earn 20–40% discounts. Allowing companies to monitor driving habits via an app can save 10% to 15%. Warning: poor driving (hard braking, speeding, late-night driving) can increase rates 10–30%. Most programs offer 30–90 day opt-out windows.

Privacy considerations: Programs collect driving data typically retained 6–12 months and may share anonymized data with affiliates. Read terms before enrolling.

Consider paying minor damage out of pocket. A single-car scrape costing $500 isn’t worth the 20–40% surcharge that filing could trigger. However, always report accidents involving injuries or the other driver.

Maintaining a clean driving record and practicing safe driving are the best long-term strategies. Moving violations affect your auto premiums for 3–5 years.

Major life events trigger rate changes—and present opportunities to review your insurance coverage.

Marriage: Combining policies often saves 10–15% for couples with clean records. But adding a spouse with tickets can increase costs. Request quotes both together and separately before deciding to stay with the same insurer or switch. Bundling multiple policies, such as auto and home insurance, with the same company can provide additional savings.

Moving: Relocating from a dense city to suburbs can cut premiums 20–40%. Moving to hurricane zones or high-theft areas raises them. Life changes such as moving to a new area can significantly impact car insurance premiums. Shop around whenever you change addresses.

Adding a teen driver: Expect insurance costs to jump $1,500–$2,500 annually, as adding a teen driver to your policy can increase your premiums significantly due to their higher risk profile. Cost effective strategies:

Employment changes: Shorter commutes, public transportation use, or permanent remote work qualify for lower ratings. Getting a new job that requires a shorter commute can lower your car insurance premiums. Update your insurance agent promptly.

Older drivers (70+): Premiums may rise modestly due to claim severity data. Consider cars with current safety features, take senior-focused defensive driving courses, and maintain regular vision checks.

Managing your insurance policy effectively is key to getting the most value for your money and ensuring you’re always properly protected. One of the easiest ways to save money on auto insurance is to take advantage of the many discounts insurance companies offer. For example, you might qualify for a low mileage discount if you don’t drive much, a good student discount for maintaining strong grades, or a discount for completing a defensive driving course.

Bundling your auto insurance with other policies, like homeowners or renters insurance, can also lead to significant savings through multi-policy discounts. It’s smart to shop around and compare rates from different insurance companies regularly—what was the best deal last year might not be the lowest price today.

Don’t forget to review your insurance policy at least once a year. A step-by-step explainer on how to read your car insurance policy can make this review much easier. Life changes, such as a new job, moving, or adding a driver, can affect your insurance costs and coverage needs. Many insurers offer discounts for safe drivers with a clean driving record, and some have usage-based insurance programs that reward defensive driving habits with lower premiums.

By staying proactive—claiming every discount, comparing offers from different insurers, and keeping your policy up to date—you can keep your premiums low and your coverage strong. Managing your insurance policy isn’t just about paying bills; it’s about making sure you’re always getting the best deal and the right protection for your needs.

Most people handle buying insurance decisions fine on their own. But certain situations call for professional help or regulatory intervention.

Work with an independent agent when you have:

Independent agents access multiple companies and their fees are typically embedded in commissions—not charged separately.

Contact your state insurance department if you encounter:

The National Association of Insurance Commissioners and the Insurance Information Institute provide educational resources on policy language and filing complaints.

Bottom line: Review your insurance policy annually. Comparison shop at least every two years. Use higher premiums strategically, claim every discount, and adjust coverage as your life changes. Saving money on car insurance isn’t about cutting corners—it’s about making smart choices that keep you protected while eliminating waste.

Your next step? Pull up your declarations page today and verify every discount is applied. Then get three quotes before your next renewal. The best deal is out there—you just have to look for it.

Compara y obtén cobertura rápido

Encuentra y compara seguros de auto en minutos y obtén su puntaje de crédito gratis.

Elige cuando pagar

Selecciona fechas de pago que coincidan con tu día de pago de sueldo.

Gestiona todo en un solo lugar

Realiza un seguimiento de tu póliza, administra los pagos y solicita una extensión de pago directamente desde tu perfil.

.svg)