Getting behind the wheel legally in America requires car insurance. But what happens when insurance companies demand a massive chunk of your paycheck before they’ll even start your coverage? For many drivers, this upfront barrier feels like an impossible hurdle.

Here’s the reality in 2026: you don’t necessarily need to empty your bank account to get insured. Low down payment car insurance exists, and understanding how it works can save you both stress and money.

Low down payment car insurance refers to policies that minimize the initial amount due while still providing legal coverage. This isn’t a special type of policy—it’s a payment structure offered by many standard insurance providers.

In 2026, most insurers typically require at least the first month’s premium, or a fixed percentage of the 6- or 12-month term, before coverage starts. The term “down payment” in car insurance is actually a bit misleading because it’s not an additional fee. It’s simply the first portion of your total premium that becomes due immediately when your insurance policy activates.

Low down payment options are especially popular with drivers facing upfront cash-flow challenges. Students juggling tuition and living expenses, gig workers with variable income, families adding a second or third vehicle—these are the people who benefit most from flexible payment options. If you’ve ever been stuck between paying rent and paying for insurance, you understand exactly why this matters.

Don’t let high upfront costs hold you back from getting the protection you need. OCHO is revolutionizing car insurance with no deposit policies that deliver instant, affordable coverage. Say goodbye to the stress of scraping together a lump sum just to get on the road. With OCHO, there’s no financial barrier to getting covered today—and no surprises later.

Our innovative approach ensures you can drive with confidence, knowing your policy starts working the moment you’re approved. It’s car insurance on your terms: flexible, affordable, and built for real life.

Let’s get specific about numbers. The down payment is simply a portion of the total premium, not an extra fee tacked on top.

In 2026, many insurance companies ask for around 8%–33% of the total six- or twelve-month premium as a starting payment. The range varies based on your driving history, the coverage options you select, and which insurer you choose.

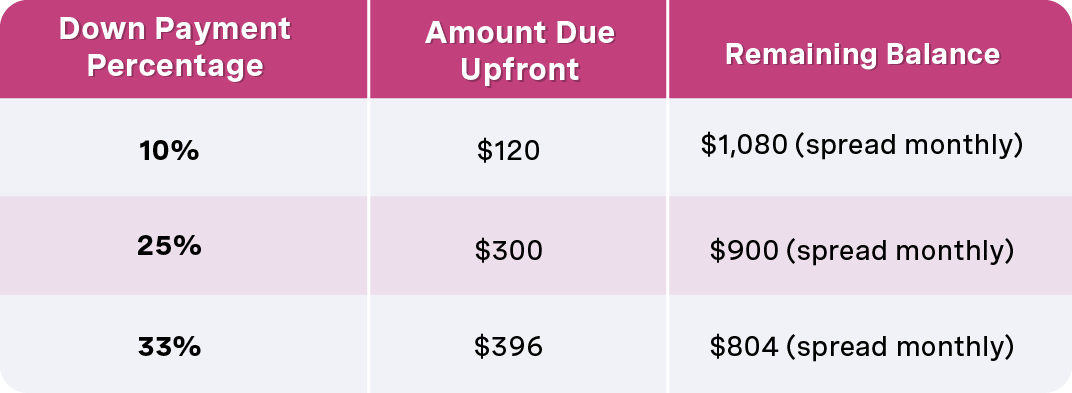

Here’s a concrete example using a $1,200 annual premium on a 2023 Toyota Camry:

The trade-off is straightforward: lower down payments usually mean higher monthly installments. If you put down $120 and spread the remaining $1,080 over 11 months, you’re looking at roughly $98 per month. Put down $396 upfront, and your monthly cost drops to about $73.

There’s another catch many drivers miss. Installment or billing fees—often $1 to $5 or more per payment—can subtly increase the total cost when choosing a very small down payment. Pay in monthly installments for a year, and those $3 fees add up to $36 extra. That’s real money leaving your pocket.

Finding cheap car insurance with a low down payment starts with one critical step: comparison shopping. Collect at least 3–5 car insurance quotes online or from local agents before committing.

Here’s your action plan:

Filter for flexible insurers. Look for car insurance companies that explicitly advertise flexible billing options, low initial payments, or phrases like “start with just your first month.” Some carriers are more accommodating than others.

Adjust your coverage levels. Choosing minimum coverage instead of full coverage dramatically reduces both your premium and your upfront payment. Just understand the trade-off—minimum liability protects others but leaves your own vehicle unprotected if you cause an accident.

Tweak your deductibles. Opting for a higher deductible on comprehensive and collision coverage lowers your premium. A $1,000 deductible instead of $500 can cut your insurance rate significantly.

Remove unnecessary add-ons. Roadside assistance, rental reimbursement, and other extras increase your premium. If you already have AAA or your credit card offers rental coverage, you might be paying for duplicate protection.

Provide accurate information. Your mileage, garaging address, and vehicle safety features all affect your car insurance costs. A car with anti-theft devices, airbags, and backup cameras often qualifies for lower premiums.

Drivers with a clean driving record—no at-fault accidents or major violations for at least three years—are more likely to qualify for lower initial payments. Most insurers reward safe driving with competitive rates and more flexible payment structures.

Let’s be clear: true “no deposit car insurance” is essentially a myth. The phrase gets thrown around in marketing, but reputable insurers all require some payment upfront before coverage begins.

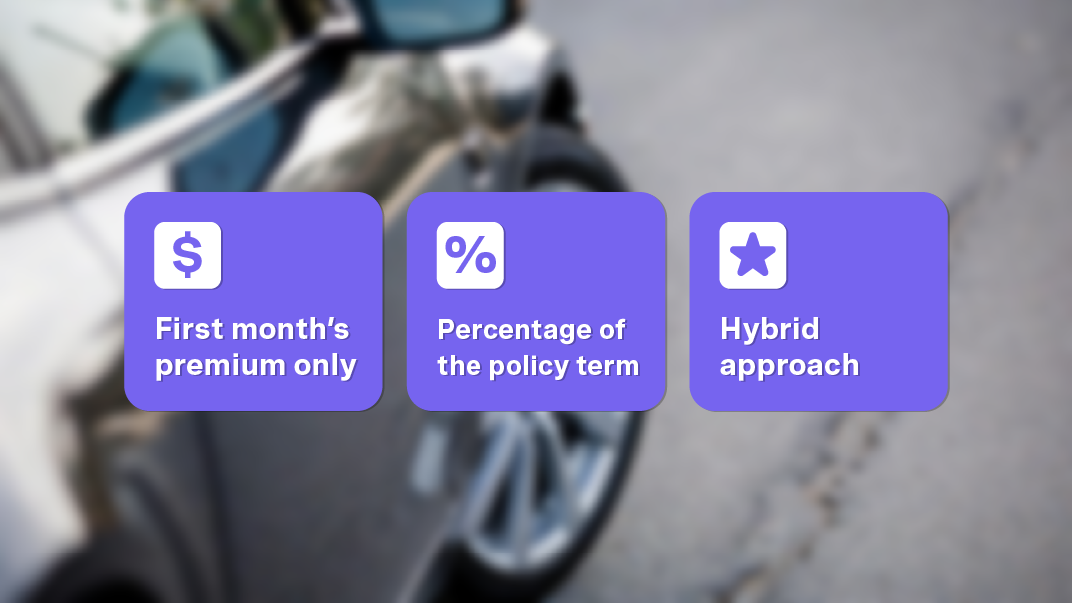

What you can find are realistic alternatives that minimize the financial burden:

Option 1: First month’s premium only. Many insurance companies let you start coverage by paying just your first month’s premium. For a driver in Ohio or Texas with minimum coverage and a good driving record, this could be as low as $20–$40 with certain online carriers.

Option 2: A percentage of the policy term. Some insurers structure it as a percentage—say, 15% of your six-month premium—rather than a specific dollar amount.

Option 3: Hybrid approach. A small down payment plus a slightly higher first installment, then regular monthly payments going forward.

Consider a six-month auto policy. Choosing a six-month policy instead of twelve months reduces the size of the initial payment, even if per-month costs are similar. Your payment upfront is calculated against a smaller total, which means a smaller dollar amount leaves your pocket on day one.

Explore pay-per-mile insurance. If you drive fewer than 7,500–8,000 miles per year, pay per mile programs from carriers like Metromile (where available), Allstate’s Milewise, or Progressive Snapshot can significantly reduce your total premium. Lower premiums mean lower down payments. These programs work especially well for urban commuters, retirees, or anyone who works from home.

Don’t be afraid to ask insurers directly about:

Many drivers don’t realize these options exist simply because they never ask.

Getting insured with a low monthly premium and minimal money upfront is just step one. Planning beyond month one is crucial to avoid cancellations, late fees, and the higher car insurance rates that follow.

Here’s an example budget breakdown:

The paid-in-full option saves money through a lump sum discount, but the low down payment approach keeps more cash available when you need it most.

Set up automatic payments or calendar reminders to prevent late fees or policy lapses. A single missed payment can raise your future premiums and restart any progress you’ve made building a continuous coverage history. Some insurers in 2025–2026 offer small discounts for automatic bank draft (ACH) compared with credit card payments—typically 1-3% off your premium.

An SR-22 filing is a form some states require after DUIs, serious violations, or driving without insurance. It proves you carry the state-mandated minimum coverage and represents what insurance companies call “financial responsibility.”

Here’s the hard truth: high risk drivers and those needing SR-22 policies typically face larger down payments. Insurance companies view them as more likely to cancel or miss payments, so they want more money upfront to protect themselves.

However, some specialty carriers let drivers trade a slightly higher premium for a smaller initial payment. It’s a negotiation worth having.

Concrete scenario: A driver needing SR-22 in 2026 negotiates a modest upfront payment by choosing state-minimum coverage and opting for higher deductibles on any optional coverage. Instead of a $500 down payment, they secure coverage with $150 down and higher monthly payments.

Fair warning: missing payments when you have an SR-22 filing is especially dangerous. In certain states, a policy cancellation can restart your SR-22 filing period entirely. You could find yourself back at square one, owing additional fees and facing even higher auto insurance rates.

The same moves that cut your total premium also reduce the required down payment. Think about it—your down payment is a percentage of your total. Lower the total, lower the percentage.

Strategies that work in 2026:

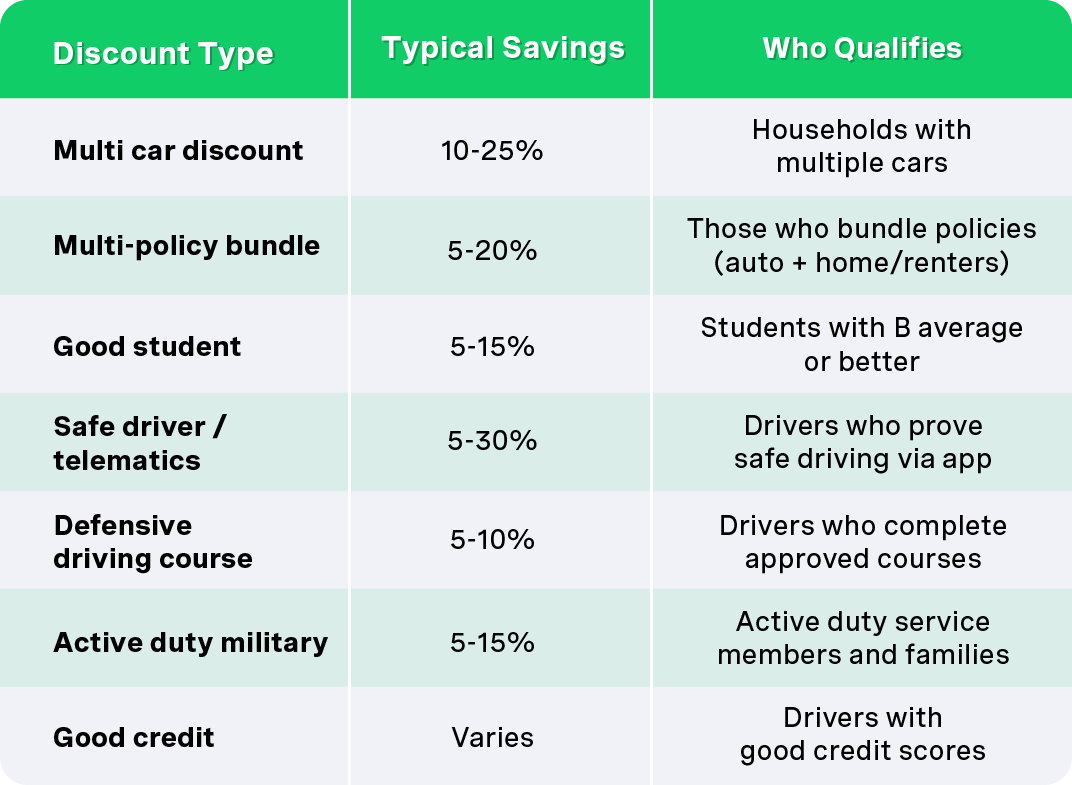

Key car insurance discounts for 2026:

Stacking discounts example: A college student drives a 2019 Toyota Corolla shared with her brother. She maintains a 3.5 GPA and uses a telematics app showing safe driving habits.

Her lowest down payment at 10%: $110 instead of $180. Her monthly cost drops proportionally too.

Choosing the absolute minimum payment upfront can help in a tight month, but it may cost more over the life of your car insurance policy. Understanding the trade-offs helps you make a smart decision.

Advantages of minimal down payment:

Trade-offs to consider:

Before choosing the lowest possible down payment, ask your insurer to show you the total cost comparison. Sometimes paying $50-100 more upfront saves $100+ over the policy term.

Some ads use aggressive wording designed to confuse shoppers about when they actually have coverage. Let’s decode the marketing speak.

“Buy now, pay later” typically still requires some payment before the insurance policy activates. You’re not getting free coverage for any period.

“First month free” often means your first payment is due within 30–45 days, not that coverage is truly free. You’ll still pay for that month eventually.

“Instant coverage” normally refers to fast underwriting and immediate policy activation, not zero cost. You’re still paying something.

Major red flag: Any offer claiming “no payment until after your accident” or similar language is not real insurance. This is likely a scam designed to take your money without providing actual coverage.

Protect yourself:

Legitimate low down payment car insurance in 2026 will always spell out an exact dollar amount due before a specific start date. If an offer seems too good to be true, it probably is.

While this article focuses on low down payments, sometimes paying more upfront is the better long-term deal. It feels counterintuitive, but the math often favors those who can pay upfront.

Benefits of paying six or twelve months in full:

Numeric example:

The driver paying in full saves $207 over the year compared to the lowest down payment option.

A larger initial payment makes especially good sense if:

Always ask insurers to quote both options: the lowest possible down payment AND a higher down payment or paid-in-full option. Compare the total cost over the term before deciding.

You can get low down payment or zero down payment with OCHO. That's because we finance your downpayment, and you pay us back, interest-free.

Same-day coverage is often possible if you can pay at least the first month’s premium by card, e-check, or another accepted method. “Almost no money” usually still means a modest amount—for example, under $100 for bare-bones liability in states like Ohio, Texas, or Indiana, depending on your driving record and vehicle.

Very cheap car insurance with minimal money upfront exists, but you’ll need a clean driving record and willingness to accept minimum coverage. Call or chat with insurers directly to ask for their minimum initial payment for a new policy in 2026. Some may surprise you with flexible payment options you won’t find advertised online.

In most states, insurers use credit-based insurance scores that influence the total premium and, by extension, the dollar amount due upfront. Drivers with bad credit often face higher premiums across the board.

However, some states restrict or ban the use of credit in auto insurance pricing. California, Hawaii, and Massachusetts limit how insurers can use credit information. If you live in these states, your financial strength matters less to your insurance rate.

Improving your credit over time can unlock lower premiums and more flexible payment options at renewal. It’s a long game, but it pays off.

Unused premium is generally refundable, but insurers typically deduct:

If you cancel after only a few weeks, you may get back only a portion of what you initially paid. The refund calculation method matters too. Ask about “short-rate” versus “pro-rata” cancellation methods when starting a policy so you know exactly how refunds will be calculated.

Many insurers let policyholders adjust payment schedules and initial amounts at each 6- or 12-month renewal. If you had no late payments during the previous term, you may qualify for more flexible options or slightly smaller required down payments.

Review your quote carefully at renewal. Ask specifically how much is required upfront and how that changes if you pay a bit more or less initially. Your payment history with that insurer gives you negotiating leverage.

New and teen drivers are considered higher risk, so their premiums and minimum down payments are often higher than experienced drivers’ in 2026. Insurance companies don’t have driving history to evaluate, which translates to more expensive coverage.

Strategies to reduce costs as a new driver:

The key is shopping around. Auto insurance rates for new drivers vary dramatically between carriers, sometimes by hundreds of dollars for identical coverage.

Compara y obtén cobertura rápido

Encuentra y compara seguros de auto en minutos y obtén su puntaje de crédito gratis.

Elige cuando pagar

Selecciona fechas de pago que coincidan con tu día de pago de sueldo.

Gestiona todo en un solo lugar

Realiza un seguimiento de tu póliza, administra los pagos y solicita una extensión de pago directamente desde tu perfil.

.svg)