If you drive in Missouri, you need insurance. It's that simple. But what exactly does Missouri law demand, what happens if you skip it, and how much coverage do you actually need? This guide breaks down everything Missouri drivers need to know about car insurance requirements in 2026.

Every registered motor vehicle in Missouri must carry liability insurance and uninsured motorist coverage. Here's what matters most:

Missouri is a financial responsibility state, meaning every driver must prove they can pay for damages they cause on the road. Most Missouri drivers meet this obligation by purchasing car insurance in Missouri through a licensed insurance provider.

Missouri car insurance laws apply to any Missouri car registered with the Missouri Department of Revenue, regardless of how often it's driven. The minimum car insurance requirements are the lowest coverage limits you can legally carry-not necessarily what you should carry. Think of them as a legal floor, not a recommendation.

Drivers must keep proof of insurance in their vehicle at all times in Missouri. You'll need to carry proof and show it after traffic violations, during routine stops, or if you're involved in an accident. The sections below cover required coverages, penalties for driving uninsured, and the optional coverages that can actually keep you protected.

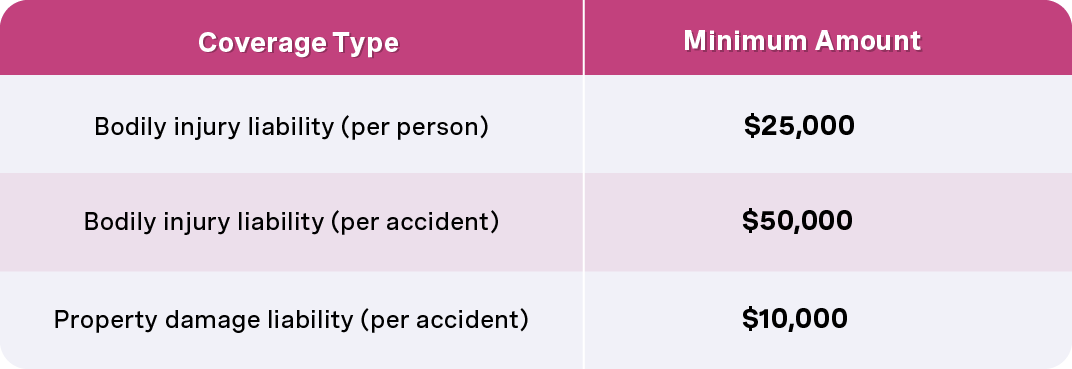

Missouri requires liability insurance and uninsured motorist coverage on every active auto insurance policy. Here are the mandatory minimum coverage amounts:

"Per person" means the maximum your insurance company will pay for one individual's injuries. "Per accident" is the total cap across all parties involved in a single crash. So if you cause a car accident injuring three people, each person's claim is capped at $25,000, and total bodily injury payouts won't exceed $50,000-even if combined medical bills run higher.

These minimum limits have been in place for years, but real-world medical costs and vehicle prices have skyrocketed. Property damage liability minimum is $10,000 per accident in Missouri, which might not even cover a fender on a newer SUV. Your liability coverage pays for the other driver's injuries and damage to that person's property when you are at fault. It does not cover your own vehicle repairs or your own medical bills.

Uninsured motorist coverage is mandatory in Missouri to protect you when the at-fault driver has no insurance. Missouri utilizes this requirement because roughly 1 in 8 drivers nationally carry no coverage at all.

The required uninsured motorist bodily injury limits match the liability structure: $25,000 per person and $50,000 per accident. This motorist coverage kicks in when the at-fault driver has no insurance or in many hit-and-run situations where the other driver can't be identified.

Uninsured motorist coverage helps pay your medical costs, lost wages, and related damages for you and your passengers. However, it typically does not repair your car-Missouri does not require uninsured motorist property damage coverage, so your vehicle damage in a hit-and-run scenario may not be covered unless you carry separate collision coverage. Many Missouri drivers choose higher uninsured motorist limits and also add underinsured motorist coverage to fill the gap when someone with enough insurance to be legal still doesn't have enough to cover your full losses.

Missouri offers optional coverages beyond minimum liability insurance that can seriously protect your finances. While the legal minimums focus on liability and uninsured motorist protection, these optional coverages cover your own car and expenses:

Optional coverages can reduce out-of-pocket expenses after an accident-sometimes dramatically. The best coverage for you depends on your vehicle, budget, and how much risk you're comfortable absorbing, so reviewing car insurance coverage FAQs can help you compare options before you buy.

Insurance coverage usually follows the car, but who's protected varies by insurance policy language. The named insured, spouse, and resident family members are typically covered while driving the insured motor vehicle.

"Permissive users"-friends or relatives who have your permission to drive your car-are generally covered under your liability insurance when driving someone else's car in Missouri. Coverage for a rental car often extends from your existing policy for liability (and sometimes collision or comprehensive), but confirm specifics with your insurer before renting.

One important note: commercial use like rideshare or delivery driving may require special endorsements or a separate commercial policy. Standard personal auto policies often exclude commercial use, and gaps here can leave you completely exposed. Check with your insurance company if you drive for work.

Missouri law requires drivers to show they can pay for damages they cause-usually through an active insurance policy. You must show proof of insurance when registering a vehicle, during traffic stops, and after any reportable car accident.

Missouri accepts both paper ID cards and electronic proof of insurance on a smartphone. Some drivers may qualify to prove financial responsibility through alternatives like surety bonds or self-insurance certificates, but these are rare and typically reserved for businesses or fleets-not everyday drivers.

Failure to provide acceptable proof when requested can lead to citations, fines, or driver's license actions by the Missouri Department of Revenue.

Driving an uninsured motor vehicle is a misdemeanor under Missouri law, and the consequences escalate fast. If you're caught driving without the required coverage:

Failure to maintain insurance in Missouri can result in fines and license suspension even if you weren't involved in an accident, and the broader penalties and risks of driving without insurance can follow you for years. Missouri's "No Pay, No Play" provision can also limit an uninsured driver's ability to recover non-economic damages like pain and suffering-even when the crash wasn't their fault. If a driver at fault in an accident causes damages exceeding the minimums, they are personally responsible for the remaining costs, including legal fees, medical bills, and property damage.

Missouri uses a point system to track every traffic violation on your driving record, and insurers use this history to price your policy. Your driving history significantly impacts your insurance rates.

Maintaining a clean record, avoiding new violations, and completing approved driver improvement programs can help reduce points and lower your missouri car insurance rates over time.

State minimum limits rarely match the real costs of a serious car accident in 2026. A multi-vehicle crash can produce medical bills, lost wages, and legal defense costs that blow through 25/50/10 limits before you blink.

Many Missouri drivers choose higher coverage limits-like 50/100/50 or 100/300/100-to provide greater financial protection for their savings, wages, and home equity, and may look for fast, affordable Missouri car insurance with $0 down to meet these higher limits without stretching their budget. For example, if a crash causes $100,000 in medical expenses and your policy only covers $50,000 per accident, you're personally on the hook for the remaining $50,000. That's not a hypothetical-it's a real scenario people face.

Higher underinsured motorist coverage and uninsured motorist limits help cover medical costs and long-term treatment if you're injured by someone without enough insurance. Balance your premium cost with your actual risk: review your limits annually or after major life changes like buying a home, adding a teen driver, or paying off a car loan. A free consultation with a licensed agent can help you find the right balance without overpaying on insurance costs.

Yes. As long as your motor vehicle is registered and operated on Missouri roads-even occasionally-it must meet state car insurance requirements. If the car is truly off the road and not being used, you may explore suspending coverage and registration simultaneously, but you must follow Missouri Department of Revenue rules to avoid penalties. Simply letting your insurance policy lapse while keeping active registration is a recipe for fines and license suspension.

Many Missouri policies extend liability coverage automatically to a temporary rental car. However, collision and comprehensive coverage on the rental may depend on your specific insurance policy terms. Review your policy or call your insurance company before renting to decide whether you need the rental company's additional options. Don't assume you're covered-check first.

Absolutely. Missouri can suspend a driver's license for failing to show proof of insurance during a traffic stop, being cited for driving uninsured, or not maintaining required SR-22 filings. Reinstatement usually requires proof of current insurance, paying reinstatement fees, and possibly maintaining SR-22 certification for two years or more.

SR-22 is not a separate insurance policy-it's a certificate of financial responsibility that some high risk drivers must file to prove they carry at least Missouri's minimum insurance requirements. Your insurer files it directly with the state. Any lapse in your policy during the SR-22 period triggers automatic license suspension and resets the clock on your filing requirement. It's a headache you want to avoid.

A few practical moves: raise your deductibles on collision and comprehensive to lower your premium, maintain a clean driving record, bundle your auto insurance with home or renters insurance, and ask about discounts for safe driving or telematics programs. Shopping around and comparing quotes from multiple providers helps too-missouri car insurance rates vary widely between companies. Just don't drop essential coverages or go below recommended coverage limits to save a few dollars. The money you save now could cost you tens of thousands after a serious accident. State laws set the floor, but smart drivers build above it.

Compara y obtén cobertura rápido

Encuentra y compara seguros de auto en minutos y obtén su puntaje de crédito gratis.

Elige cuando pagar

Selecciona fechas de pago que coincidan con tu día de pago de sueldo.

Gestiona todo en un solo lugar

Realiza un seguimiento de tu póliza, administra los pagos y solicita una extensión de pago directamente desde tu perfil.

.svg)