Georgia drivers searching for affordable car insurance have probably come across the term "pay as you go." It sounds simple - pay only when you drive, skip the massive upfront deposit. But in Georgia, the reality is more nuanced. Let's break down what pay as you go car insurance actually means in this state, who it works for, and how OCHO helps Georgia drivers get covered without draining their bank account.

Georgia allows pay as you go car insurance, but most options still require some form of down payment and must comply with the state's continuous coverage rules. There's no magic loophole that lets you dodge Georgia's insurance requirements.

OCHO is a digital broker that helps Georgia drivers access pay-as-you-go style payment plans - including $0 down for qualifying drivers - rather than being a pay-per-mile insurer itself. We compare real-time quotes from partner insurance companies, then finance the down payment interest-free so qualifying drivers can start coverage with instant coverage once it’s bound, without a financial gut punch. OCHO offers insurance with little to no down payment, and no down payment options help manage insurance costs effectively.

In Georgia, "pay as you go" usually means flexible payment schedules - biweekly or monthly - and sometimes pay per mile coverage. It does not mean true daily on/off insurance. Pay-as-you-go insurance can include shorter, manageable payment periods that align with your budget. This article is written specifically for Georgia drivers in 2026, referencing the state minimum limits of 25/50/25 (that's $25,000 bodily injury per person, $50,000 per accident, and $25,000 property damage). Any pay as you go plan must still satisfy those minimums. Georgia requires minimum liability coverage for all drivers - no exceptions.

"Pay as you go car insurance" isn't a regulated product category in Georgia. It's a marketing umbrella covering usage based insurance, pay per mile, micropayment toggle plans, and paycheck-aligned payment plans. Pay-as-you-go policies offer standard coverage options like liability, collision, and comprehensive coverage - the difference is how you pay, not what you get.

Most Georgia drivers still get standard 6-month policies. "Pay as you go" refers to how you pay, not weaker coverage, though for frequent drivers, traditional insurance can still be the better fit. Keeping continuous coverage helps your rates go down over time, and OCHO helps you do that. Continuous coverage prevents gaps that raise future premiums and helps avoid high-risk categorization.

OCHO focuses on continuous coverage with flexible payments, while some Georgia competitors focus on on/off short-term liability-only coverage. Here's where OCHO stands apart: we offer both liability coverage and full coverage. The advantage is that we can make comprehensive and collision insurance affordable, so you get a great package - affordable insurance that you can easily keep. If you're unsure which option fits your driving habits, it helps to understand the difference between pay-as-you-go and pay-per-mile insurance, which many Georgia drivers compare.

Georgia's insurance laws require proof of continuous coverage. The state's electronic system (GEICS) tracks policy starts and cancellations in near real-time. Stopping and starting go insurance can trigger registration suspension, fines, and higher future premiums.

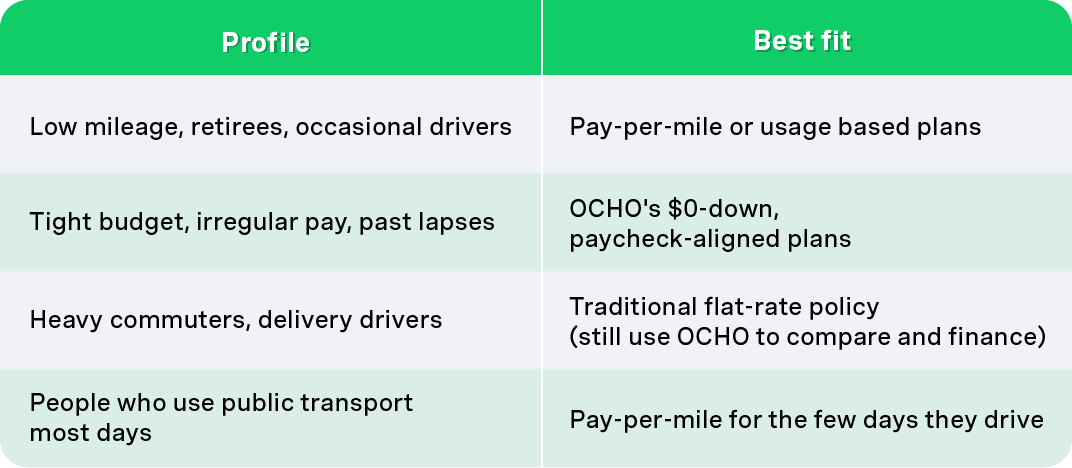

Georgia drivers will mostly encounter three models: telematics-based usage based insurance, pay-per-mile plans, and micropayment on/off toggle plans. Each has different pros, cons, and long term benefits depending on whether you're among the low mileage drivers or need continuous full coverage.

Major insurers in Georgia offer telematics programs that track your driving habits - speed, braking, time of day, and how many miles you cover. Telematics tracks driving habits to adjust insurance premiums, and insurers often monitor driving behavior including speeding and braking. Telematics devices track driving habits to calculate premiums, while some insurers track mileage using telematics devices or smartphone apps.

Typical potential savings for safe drivers range from 10–30% off base premiums after several months of monitored driving. Drivers with safe driving habits benefit most.

Key tradeoffs to know:

Pay per mile coverage uses a low base rate plus a per mile rate, charged based on actual miles driven. Policies often include a base rate plus a per-mile charge. This model is ideal for Georgia drivers under 8,000–10,000 miles per year - remote workers, retirees, occasional drivers, and second-car owners. Pay-as-you-go insurance is ideal for retirees or remote workers, and drivers who only pay for the miles they use are considered fair pricing, especially when paired with Georgia-specific car insurance options from OCHO.

Low-mileage drivers can save significantly with pay-as-you-go plans. Here's a concrete example:

Pay-per-mile insurance charges based on actual miles driven, and pay-as-you-go insurance charges based on actual mileage driven. But high-mileage drivers commuting daily on I-75 or I-20 may end up paying more than with traditional policies. Before switching, estimate how many miles you actually drive.

Some plans allow coverage to be turned on and off as needed - daily or short-burst liability coverage where drivers "toggle" insurance for a day or a few days at a time. These products typically offer only state-minimum liability, no full coverage.

The risk? If you forget to turn insurance back on, you're driving uninsured. Frequent lapses show up on Georgia insurance records, triggering registration issues and higher future premiums. Many drivers who rely on these models end up classified as high risk drivers.

OCHO's approach keeps coverage continuous while still letting customers pay in small, paycheck-friendly amounts - no toggling, no gaps, no surprises.

Georgia's electronic insurance database (GEICS) checks for active policies in near real-time, making continuous coverage critical for every registered vehicle.

Georgia minimum liability requirements (25/50/25):

Any pay as you go plan must meet these minimums.

What happens when coverage lapses:

Continuous coverage can lead to lower premiums over time. Frequent policy cancellations can damage your credit score and lock you into expensive high-risk brackets. Turning coverage off for even a weekend can cost more in fees and future premiums than the short-term savings.

Pay-as-you-go insurance can be cheaper for low-mileage drivers, but it's not automatically cheaper for everyone. Your driving history, vehicle value, coverage level, ZIP code (Atlanta vs. rural Georgia), and annual mileage all determine whether you save money or pay more, and understanding how much car insurance should cost for your situation can help you set realistic expectations.

Comparing quotes helps find the best car insurance deal. OCHO helps drivers compare multiple real-time quotes, placing total annual cost and first payment side by side so you can see the actual numbers, similar to the steps in our complete guide to smart auto insurance quotes.

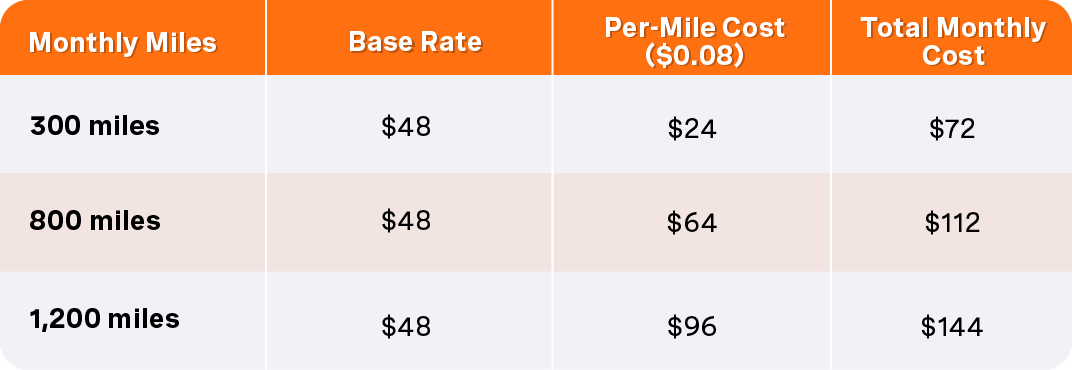

Simple formula: monthly cost = base rate + (per mile rate × miles driven).

Example: A Georgia driver near Macon switches to remote work and drops from 12,000 to 4,000 miles per year. Traditional policy: $1,200/year. Pay-per-mile plan: $600 base + (4,000 × $0.08) = $920/year - roughly 23% savings. That's real money back in your pocket.

Keep in mind: occasional long trips (Atlanta to Savannah for vacation) can temporarily spike pay-per-mile bills. Account for seasonal driving and holidays before committing. Drivers with newer cars or loans may still want full coverage, and OCHO can help finance that higher protection level without a huge deposit through its no deposit car insurance financing model.

After 12 months of coverage with no lapses, you can access lower premiums. Georgia insurers reward loyalty - clean, continuous history can move you from "high risk" to "preferred" status, where lower rates and discounts become available.

OCHO provides up to 15 extra days for payment without penalties, so even during tight months, your coverage stays active. OCHO provides up to 15 extra days for payment flexibility, and provides up to 15 extra days to make payments when needed. That built-in breathing room is the difference between maintaining coverage and starting over with expensive high-risk rates, and our How OCHO Works FAQ explains the details.

Some Georgia insurers offer loyalty and safe-driver discounts after 3–5 years of clean, continuous insurance history. The future payoff of staying covered today is significant.

OCHO is a digital broker - not a carrier - focused on Georgia drivers who struggle with large upfront car insurance costs. We work with partner insurers that can offer both minimum liability and full coverage options, plus add ons like roadside assistance, rental reimbursement, or uninsured motorist protection, all rooted in our broader mission to make car insurance fair and accessible.

OCHO's plans require little to no down payment for coverage, and we emphasize continuous coverage (no daily on/off) with payments that sync with your pay cycle - biweekly or monthly, just like our core service for easy, free car insurance quotes with flexible payments.

Most Georgia insurers require a substantial down payment - often 20–40% of the policy. OCHO finances that amount interest-free, reducing the first payment to as little as $0 for qualifying drivers, effectively turning traditional deposits into no down payment car insurance with $0 upfront.

Here's how it works:

Your next payment is always predictable, always manageable.

Unlike micropayment products that let Georgia drivers toggle coverage and risk driving uninsured, OCHO keeps you covered continuously. No telematics device tracking your every move. No surprise per-mile surcharges.

Keeping a steady policy with OCHO's partners helps you qualify for better tiers and lower premiums at renewal. Frequent cancellations do the opposite.

Happy customers in Georgia tell us stories like this: A driver in Gwinnett County had been juggling on/off liability-only coverage for two years, racking up lapse fees and paying sky-high premiums every time they restarted. After switching to OCHO, they locked in continuous coverage with $0 down, and after 12 months, their renewal quote dropped significantly. Another driver near Columbus - previously uninsured because they couldn't afford the deposit - got covered the same day through OCHO and hasn't missed a payment since, echoing many of the experiences shared in our real customer reviews of OCHO.

The right plan depends on your mileage, vehicle value, income stability, and risk tolerance.

Many drivers don't realize they can benefit from OCHO's financing even on traditional coverage, accessing no deposit, $0 down instant car insurance options while still choosing a standard policy structure.

Georgia minimum liability (25/50/25) is the cheapest way to stay legal, but it doesn't cover your own vehicle. If you rear-end someone and your car is totaled, minimum liability pays for their damages - not yours.

Full coverage adds collision and comprehensive, covering your car too. Some pay-as-you-go and micropayment products only offer liability, while OCHO's partner carriers provide full coverage options financed with small payments. OCHO can help drivers compare the cost to upgrade from minimum to full coverage while keeping first payments low. You typically pay more for full coverage, but the protection is worth it - especially if you have a loan or lease.

Getting started takes under 10 minutes. Enter your ZIP code, vehicle info, driving history, and preferred coverage. OCHO returns side-by-side quotes from multiple insurers so you can compare on your own terms.

Georgia drivers can sort options by first payment, biweekly cost, or total 6-month price to match their budget. We don't pressure customers into one carrier - we explain tradeoffs and help you manage your coverage and payments.

Have these ready to speed up your quotes:

Drivers without recent coverage can still qualify. Expect slightly higher premiums initially, but after 6–12 months of clean, continuous coverage, those rates can drop. Knowing your mileage upfront helps determine whether a pay-per-mile option or a flat-rate OCHO-financed plan is the right fit.

Is pay as you go car insurance legal in Georgia? Yes. Payment-flexible, usage-based, and pay-per-mile plans are all legal. But you cannot let liability coverage lapse while your vehicle is registered.

Can I get $0 down car insurance in Georgia? Yes. OCHO offers $0 down for qualifying drivers by financing the premium upfront interest-free with split payments.

Will pay-per-mile work if I sometimes drive to Florida or Alabama? Yes - charges are based on total miles driven, not which state you're in. But longer trips will increase that month's bill.

Can pay as you go provide full coverage? It depends on the insurer. OCHO can arrange financed full coverage - including collision and comprehensive - with small, predictable payments. Many on/off products only offer minimum liability.

What happens if a payment is late? OCHO provides up to 15 extra days to make payments when needed, helping you avoid cancellation and the costly cycle of lapses and reinstatement fees. Check your policy documents for specific details and fine print.

Georgia drivers don't have to choose between risky on/off go insurance and unaffordable big deposits. Enter your Georgia ZIP code on OCHO's website to compare real-time quotes and see both your first payment and ongoing payment options. Review your current mileage and account for your budget today, then use OCHO to access smarter, more flexible car insurance - with potential savings, continuous coverage, and no coverage gaps.

Compara y obtén cobertura rápido

Encuentra y compara seguros de auto en minutos y obtén su puntaje de crédito gratis.

Elige cuando pagar

Selecciona fechas de pago que coincidan con tu día de pago de sueldo.

Gestiona todo en un solo lugar

Realiza un seguimiento de tu póliza, administra los pagos y solicita una extensión de pago directamente desde tu perfil.

.svg)