If you drive a car in America, you need insurance. It’s not optional—it’s the law in almost every state. Motor insurance protects you against financial loss from auto accidents, theft, vandalism, and weather damage. Think of it as your financial shield on the road.

By March 2026, 48 states plus Washington, D.C. require some form of auto liability insurance as proof of “financial responsibility.” New Hampshire and Virginia have unique rules, but they still demand proof you can pay for damages. The bottom line? You can’t legally drive without coverage in most states.

A typical motor insurance policy covers three broad areas:

This motor insurance guide walks you through everything: understanding coverages, choosing limits and deductibles, managing claims, and controlling costs. We’ll cover coverage types first, then legal requirements, buying and pricing, claims procedures, special situations, and FAQs.

Most personal auto policies in the U.S. share common building blocks, even though terminology and state rules differ. Understanding these coverages is essential before you purchase or renew a policy.

Here’s what we’ll break down:

Note that lenders typically require collision and comprehensive until your loan or lease is paid off. For a 60-month loan on a 2024 SUV, that means years of mandatory physical damage coverage.

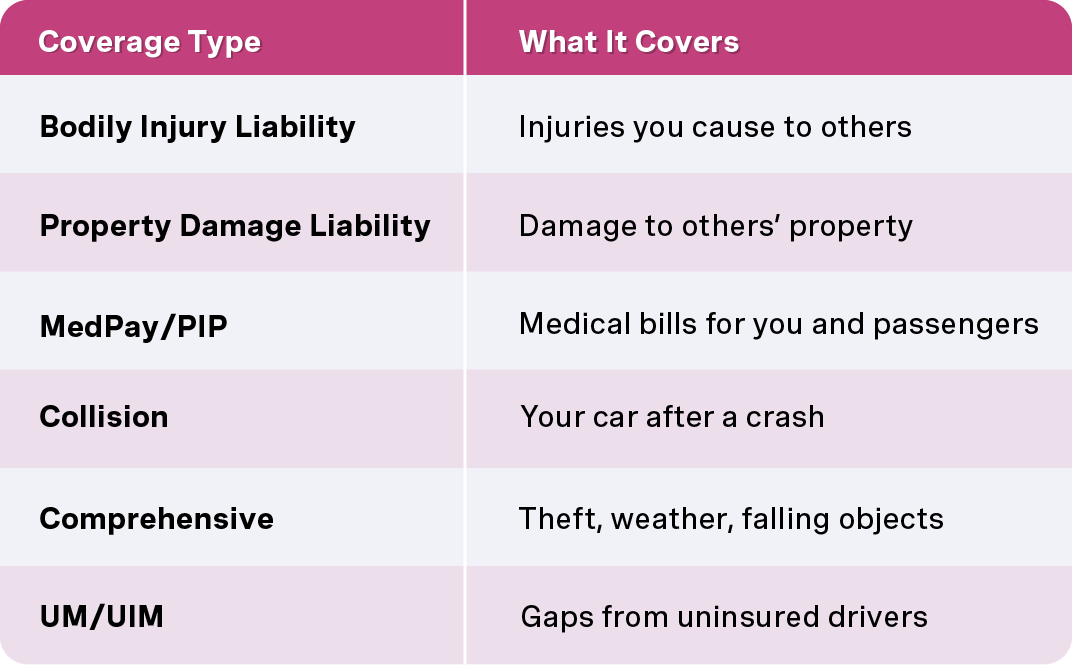

Bodily injury liability pays for injuries you cause to other people in an at fault driver scenario. This includes their medical bills, lost wages, and pain and suffering. Your liability coverage also covers legal defense costs if you’re sued after a multi-car crash.

Coverage usually follows you when you drive someone else’s car with permission, but not for excluded uses like commercial rideshare work unless properly endorsed.

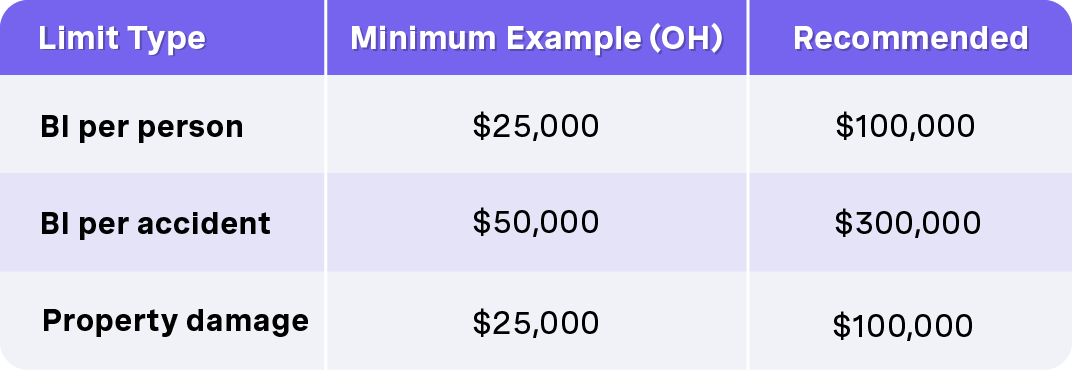

BI limits are written in split format—for example, $100,000 per person / $300,000 per accident. Ohio’s minimum is just 25/50, which is dangerously low when average bodily injury claims hit $26,000 in 2025.

Recommendation: Choose limits high enough to protect your assets. If you have significant net worth, consider an umbrella policy starting at $1 million for around $200-400 annually.

Property damage liability pays for damage caused to other people’s property: vehicles, buildings, fences, traffic signs, and utility poles.

Example: After a 2026 collision where you total someone’s 2021 pickup and damage a storefront, your property damage liability coverage pays repair or replacement costs up to your PD limit.

This coverage doesn’t repair your own vehicle—that requires collision coverage.

Ohio’s minimum is $25,000 PD, but modern vehicle prices mean damages easily exceed low limits. A single multi-car pileup can create property damage claims exceeding $50,000.

Many financial planners recommend $50,000-$100,000 PD, matching your per-accident BI limit.

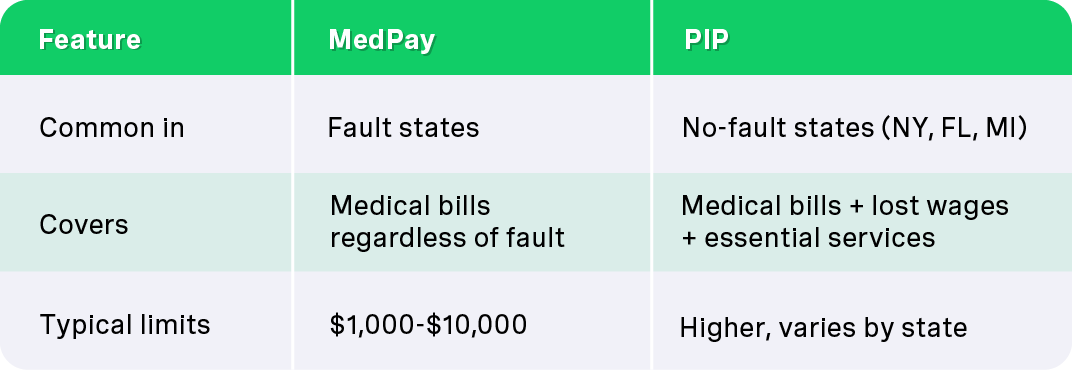

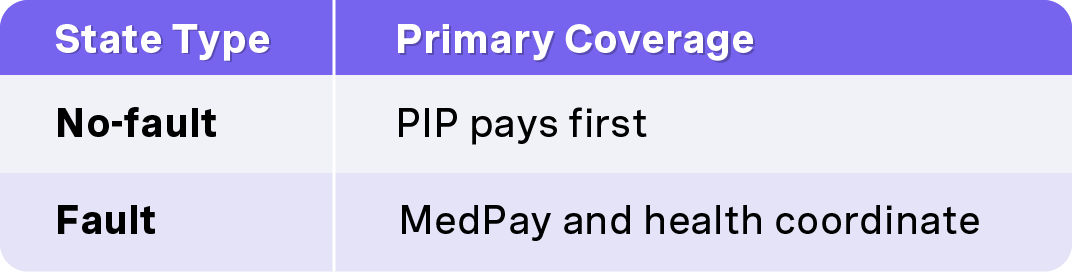

Medical payments coverage (MedPay) and PIP serve similar purposes but work differently:

Both can pay medical bills for you and passengers without waiting to determine fault. PIP in no-fault states may also cover 80% of lost wages and essential services if you can’t work after a crash.

Health insurance can overlap with MedPay/PIP, but these auto coverages often pay faster and cover deductibles your health insurance might exclude. A common MedPay limit is $5,000 per person.

Collision coverage pays to repair or replace your own vehicle after a crash—regardless of who is at fault. This includes hitting another car, backing into a pole, striking a guardrail, or damage from a pothole.

How deductibles work:

If the other driver is 100% at fault and insured, your insurance company may pursue subrogation and potentially refund your deductible.

Collision is essential for newer vehicles (0-8 years old) or cars with outstanding loans. Older vehicles worth less than $4,000 might not justify the cost.

Comprehensive insurance covers damage not caused by a collision: theft, fire, vandalism, hail, flooding, falling objects, and deer strikes. With 1.2 million vehicle theft incidents in 2025 and hail claims doubling in states like Texas and Colorado, this coverage matters.

Like collision, comprehensive has a deductible—typically $100-$500. Many drivers choose lower comp deductibles since claims are often less severe.

Comprehensive also covers glass damage and windshield replacement. Some states offer zero-deductible glass endorsements.

No state requires comprehensive by law, but lenders almost always mandate it for vehicles with a lien. It’s cost-effective even on older vehicles worth more than a few thousand dollars, especially in areas prone to storms or theft.

Uninsured motorist coverage pays when you’re hit by a driver with no insurance or in hit-and-run situations. About 13% of drivers are uninsured nationally—25% in Florida and Mississippi.

UIM kicks in when the at fault driver’s limits can’t fully compensate your injuries.

Example: In a 2026 crash, the at-fault driver carries only $25,000 BI, but your medical bills reach $80,000. Your UIM covers the remaining $55,000 if you carry higher limits.

UM/UIM also protects you when struck as a pedestrian or cyclist. Match your UM/UIM limits to your bodily injury liability limits—30% of claims involve uninsured motorists.

“Financial responsibility” laws ensure every driver can pay for injuries and damage they cause. Most states require drivers to carry minimum liability insurance as proof.

You satisfy this requirement by buying an auto policy meeting your state’s minimum limits—like Ohio’s 25/50/25 requirement. Some states allow alternatives like posting a cash bond, but these require large upfront sums.

Proof of insurance coverage (paper or digital ID card) is required when:

Driving without valid insurance can mean fines ($100-$1,000), license suspension, vehicle impoundment, and personal liability for all damages in a crash.

“Limits” are the maximum amounts your insurer pays for each coverage type. They’re often expressed as split limits for liability (e.g., 50/100/50 or 100/300/100).

The problem: If you cause $100,000 in injuries with only 25/50 limits, you’re personally liable for $75,000. That money comes from your savings, home equity, or future wages.

Consider your assets, income, and risk tolerance when choosing limits. Umbrella liability coverage adds protection above your auto policy limits for around $150/year.

Some insurers offer combined single limits (CSL)—for example, $300,000 total for any combination of BI and PD claims from one accident.

Your insurance ID card contains:

Most states accept digital proof on smartphones in 2026, but keep a paper copy as backup. Present your card at traffic stops, after an accident, or when asked by DMV.

Lost your card? Download a replacement instantly via your insurer’s app or website. Households with multiple drivers should keep copies for each vehicle.

Your premium is what you pay to keep coverage active—monthly, quarterly, or annually. The average full coverage cost nationally is $2,543 in 2026, though this varies dramatically by driver.

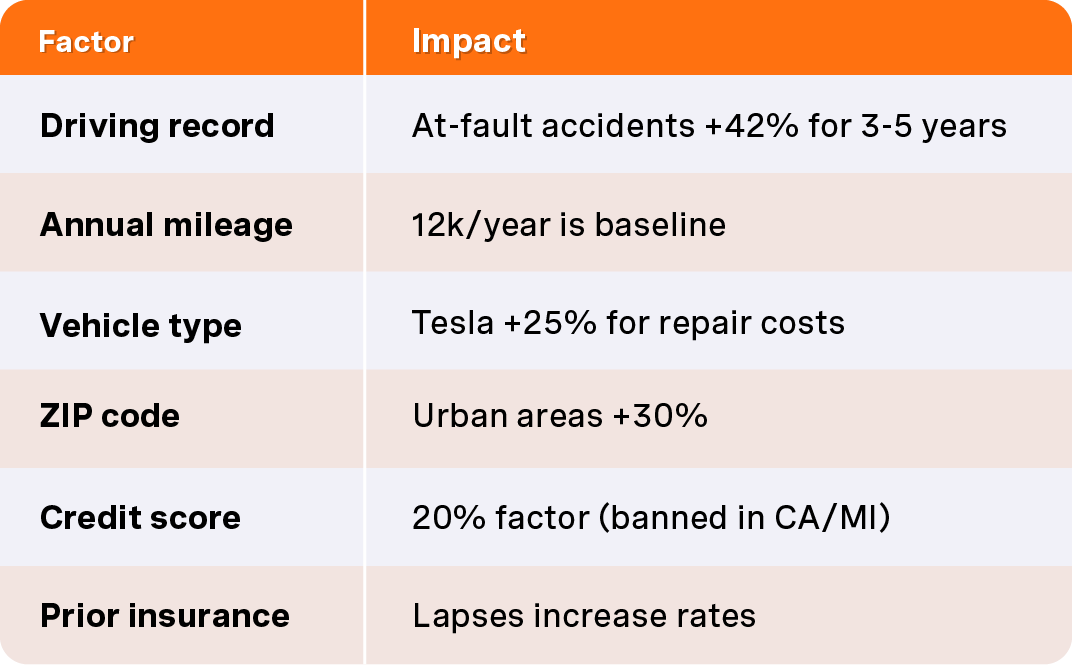

Insurance companies use actuarial data and state-approved rating formulas to estimate risk and translate it into price. You can’t control every factor (age, location), but you can influence others: driving record, vehicle choice, and coverage selections.

Premiums change at renewal based on:

At-fault accidents and moving violations typically impact rates for 3-5 years. A clean-record driver of a 2024 sedan pays significantly less than someone with two speeding tickets.

Ask your insurer or insurance agent which factors matter most in your state and what you can do over 12-36 months to improve your risk profile.

High-risk drivers include those with:

High-risk status means higher premiums, fewer options, and potential non-renewal. State-run “assigned risk” plans (like Ohio Auto Plan) ensure even high-risk drivers can obtain minimum coverage, though at higher rates.

To move back to preferred rates: complete driver improvement courses, use telematics programs, and maintain a loss-free record.

State insurance departments regulate auto insurance rates to ensure they’re not excessive or discriminatory. Insurers must file proposed rate changes with regulators before they take effect.

Consumers can access public filings and complaint statistics through state insurance departments. Regulations vary—some states require prior approval, others allow “file and use” with later review.

Contact your state insurance department if you suspect unfair pricing.

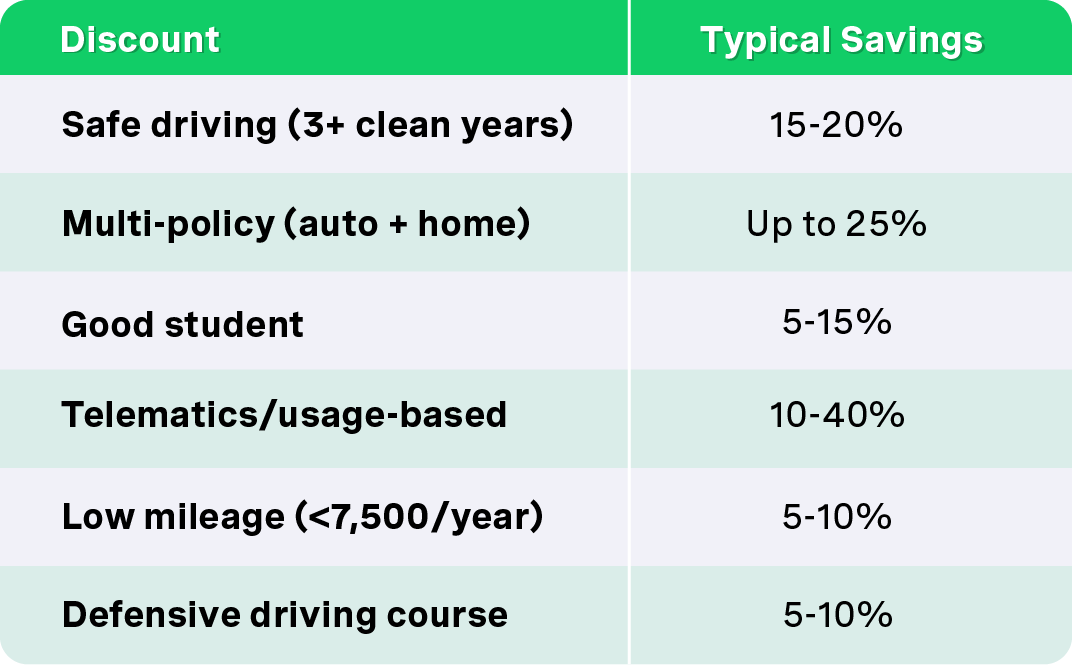

Common discounts that help you afford coverage:

Discounts are often additive but limited by company rules. Ask agents for a written list of all available discounts and verify each is applied to your policy.

The largest long-term savings come from maintaining a clean record and avoiding at-fault accidents.

Choosing the right policy means more than picking the cheapest quote. Match coverage to your car, finances, and risk tolerance.

Step-by-step approach:

Revisit coverage when buying a new car, paying off a loan, moving, adding a teen driver, or changing commute distance.

Get quotes from at least 3-5 insurers or comparison sites with identical coverage limits and deductibles for an apples-to-apples comparison. Shopping every 1-2 years yields 20-30% savings.

Options for buying:

Check independent ratings (financial strength, claim satisfaction, complaint ratios) beyond price. Review entire proposals: confirm liability limits, UM/UIM, deductibles, and exclusions for rideshare or business use.

Ask about accident forgiveness and claims service guarantees to get the best deal.

Agents help explain coverage options, interpret state requirements, and tailor policies for your household. They assist with mid-term changes like address moves, adding vehicles, and updating mileage.

Good customer service matters more than saving a few dollars. Look for:

Ask how claims are handled and whether local adjusters are available. You can change agents at renewal if service falls below expectations—just maintain continuous coverage.

Adding a teen (ages 16-24) significantly increases premiums due to higher accident rates—sometimes doubling costs to $3,000+ annually.

Strategies to manage costs:

Review coverage once teens move to college. “Student away” discounts apply when the car stays home.

Your personal auto policy often extends liability and physical damage coverage to rental cars for personal use within the U.S. and Canada.

Before buying rental company coverage:

Rental company CDWs simplify claims but cost $15-25 daily. Your personal policy may leave you responsible for loss-of-use charges from rental companies.

Verify details before renting in 2026, especially for international travel where U.S. policies typically don’t apply.

Knowing what to do after an accident occurs speeds up payment and reduces stress. Policyholders have rights (fair handling, timely decisions) and responsibilities (honest information, prompt notice).

Most insurers follow similar steps: report, investigate, evaluate, settle or deny. Timelines vary by state, but understanding the process helps you navigate it effectively.

Follow this sequence when an accident occurs:

Information to gather:

Avoid admitting fault at the scene. Report to your insurer within 24 hours, even for minor damage. Keep a claims checklist in your glove box.

Adjusters review police reports, interview drivers, inspect vehicles, and confirm coverage to determine what the company pays.

In many states, fault may be shared (comparative negligence). A 20-80 split affects how much each insurer pays.

For vehicle damage, adjusters estimate repair costs or determine total loss based on actual cash value (replacement cost minus 15-20% annual depreciation). Your deductible is then subtracted.

Keep records: claim numbers, conversation dates, estimates, receipts, and emails. These prove vital if disagreements arise.

If you disagree with a claim decision:

The appraisal process involves each side selecting an appraiser, with a neutral umpire if needed. The final value is usually binding.

Stay factual and organized when escalating disputes.

Insurance fraud—staged accidents, inflated bills, lying about drivers—is a crime in every state. It raises premiums for everyone through an estimated $40 billion annual cost.

Your duty of honesty matters when buying coverage too. Accurately list all regular drivers, garaging locations, and vehicle use. Misrepresentation can void your policy when you need it most.

Report suspected fraud to your insurer’s hotline or state agencies. Work with reputable repair shops and verify all estimates.

Not all driving situations are straightforward. Special circumstances affect coverage and claims in ways that surprise many policyholders.

Key situations to understand:

Check your specific policy wording before a loss occurs.

Standard personal auto policies often exclude coverage when your vehicle is used for rideshare (Uber, Lyft) or app-based delivery in 2026.

Many insurers now offer rideshare endorsements ($15/month) that fill gaps between personal policies and app company coverage during different periods (app on, en route, passenger on board).

If you use your car for work, sales, or contractor activities, explicitly tell your insurer. Failing to disclose regular business use leads to claim denials.

Compare rideshare company policies with your personal insurer’s offerings to avoid unexpected gaps.

A “total loss” occurs when repair costs plus salvage approach the car’s actual cash value. The insurer pays that value instead of repairs.

Actual cash value = replacement cost minus depreciation. A 2024 vehicle may be worth significantly less by 2026, even if well maintained.

Gap insurance pays the difference between actual cash value and your remaining loan balance. If your totaled car is worth $18,000 but you owe $22,000, you’d be stuck paying $4,000 without gap coverage (around $300/year).

Gap is essential for heavily financed or leased vehicles with small down payments or long loan terms.

Most policies cover occasional “permissive users” who drive your vehicle with consent. Coverage follows the car first.

If both guest driver and owner carry insurance, one policy is primary and the other secondary—depending on state law.

Be careful lending your car to people with poor records or unknown backgrounds. Your policy responds first to losses.

List frequent drivers on your policy rather than treating regular use as “occasional” to avoid coverage disputes.

After an accident, health insurance, MedPay, PIP, and liability coverages interact in complex ways:

Auto policies may have subrogation rights, allowing insurers to recover medical payments from at-fault driver settlements.

Review both health and auto policies to understand which pays first. Family members without robust health insurance may want higher MedPay or PIP limits to insure against out-of-pocket expenses.

These questions address common concerns not fully covered above, focusing on practical issues U.S. drivers face in 2024-2026.

Coverage usually begins at 12:01 a.m. on your policy effective date and continues until 12:01 a.m. on the expiration date. Mid-term changes (adding a car on March 18, 2026) typically start when processed and documented. Always obtain written proof—email, updated ID card, or endorsement—of new coverage. There’s usually no automatic grace period after expiration; if payment is late, coverage may stop immediately until reinstated.

Many policies include temporary automatic coverage (7-30 days) for newly acquired vehicles, but details vary. Check your policy in advance to understand how long new cars are covered and whether it applies only to liability or also collision and comprehensive. Call your insurer’s 24/7 line or use their app immediately after purchase to add the vehicle. Failing to notify within the specified window can leave your new car without physical damage coverage.

Increases vary by insurer, state, and severity, but at-fault crashes commonly trigger surcharges at renewal lasting 3-5 years. Minor claims might have little impact, while major injury accidents can cause 30-50% increases or non-renewal. Some insurers offer accident forgiveness programs waiving the first surcharge after several clean years. Ask your agent how a specific claim affects future premiums before filing small claims you could afford to pay out of pocket.

Insurers can cancel mid-term only for specific state-allowed reasons: non-payment, material misrepresentation, license suspension, or discovery of high risk. Most states require written notice (10 days for non-payment, 20-30 days otherwise). After an initial 60-90 day underwriting period, cancellation rules tighten—insurers often must wait until renewal to non-renew. Contact your insurer immediately if you receive a cancellation notice to explore resolution options.

Auto insurance follows the car first. Your policy is primary for liability and physical damage when a permissive driver causes an accident. The guest driver’s insurance may act as secondary if damages exceed your limits. If the driver lacked permission or exclusions apply, coverage may be limited or denied. Clearly communicate rules to anyone borrowing your vehicle, and ensure regular drivers are properly listed on your policy to protect against negligence claims.

Compara y obtén cobertura rápido

Encuentra y compara seguros de auto en minutos y obtén su puntaje de crédito gratis.

Elige cuando pagar

Selecciona fechas de pago que coincidan con tu día de pago de sueldo.

Gestiona todo en un solo lugar

Realiza un seguimiento de tu póliza, administra los pagos y solicita una extensión de pago directamente desde tu perfil.

.svg)