In today's evolving auto insurance landscape, terms like "pay-as-you-go" and "pay-per-mile" are increasingly common. While both options sound similar and promise greater flexibility than traditional insurance, they actually represent distinctly different approaches to coverage. Understanding these differences is crucial for finding the insurance structure that best fits your driving habits and financial situation.

Before diving into details, here's the fundamental difference:

Now let's explore each option in depth.

Pay-as-you-go car insurance is a payment model that breaks down your premium into smaller, more manageable installments. Instead of paying large lump sums quarterly or semi-annually, you make smaller payments more frequently—typically bi-weekly or monthly.

Pay-as-you-go insurance is ideal for:

With OCHO's pay-as-you-go insurance, you might pay $50 every two weeks instead of $200-$300 monthly. The coverage remains identical to traditional insurance, but the payment structure aligns better with how most people manage their finances—particularly those paid bi-weekly.

Pay-per-mile (also called usage-based insurance) directly links your premium to the distance you drive. Your bill typically consists of a base rate plus a per-mile charge, measured through a plug-in device or smartphone app.

Pay-per-mile insurance works best for:

With a typical pay-per-mile plan, a driver might pay a $30 monthly base rate plus $0.06 per mile. Driving 500 miles in a month would result in a $60 bill ($30 base + $30 for mileage). The same coverage might cost $100-$150 under traditional or pay-as-you-go plans.

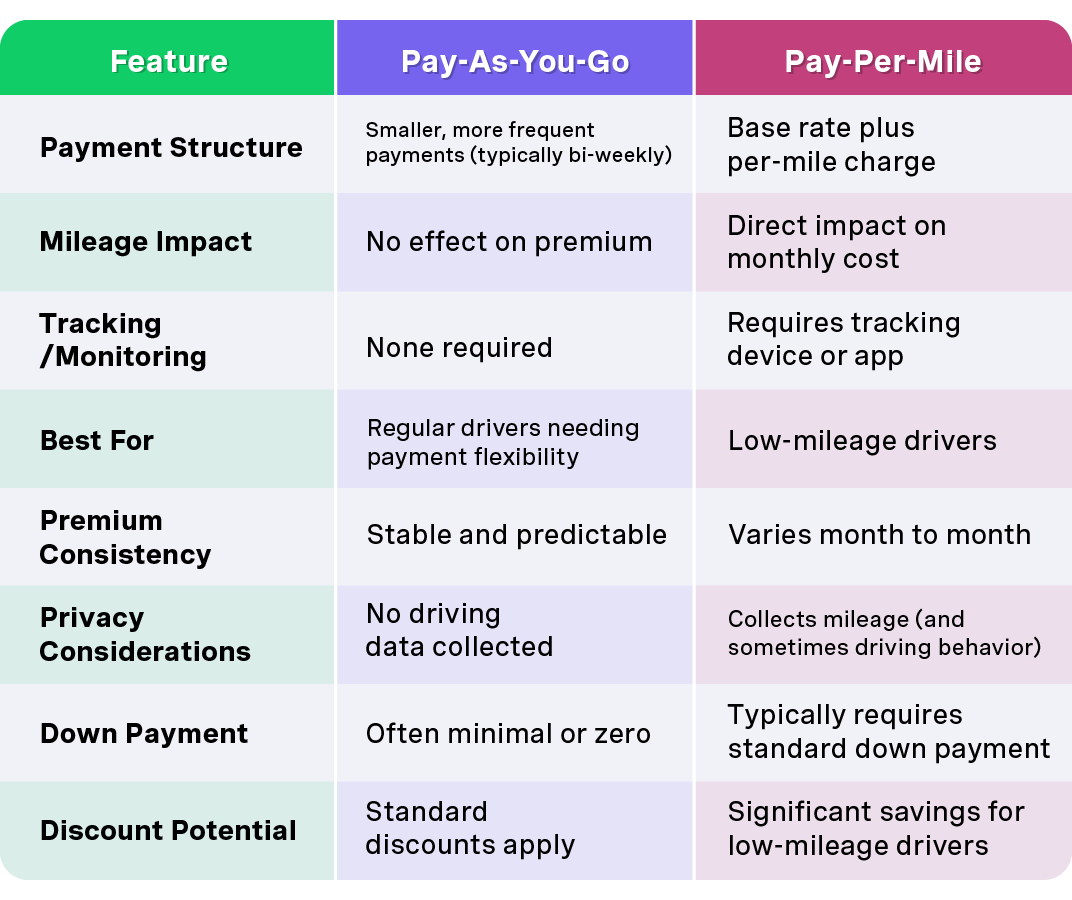

Let's break down the specific differences between these insurance models across several key factors:

Many drivers confuse pay-as-you-go with pay-per-mile because both offer alternatives to traditional payment structures. However, as we've seen, they address completely different needs.

Some drivers mistakenly believe pay-as-you-go insurance provides temporary or intermittent coverage. In reality, it offers continuous coverage just like traditional insurance—only the payment schedule changes.

While pay-per-mile can save money for low-mileage drivers, it's often more expensive for those who drive regularly. Someone driving 15,000+ miles annually would likely pay more with pay-per-mile than with traditional or pay-as-you-go insurance.

The payment structure doesn't affect coverage limits or types. You can get the same comprehensive protection with pay-as-you-go as with traditional insurance.

The best option depends entirely on your personal circumstances:

At OCHO, we've pioneered a pay-as-you-go model designed specifically for drivers who need payment flexibility without sacrificing coverage quality. Our approach offers:

Unlike traditional insurers that require large upfront payments or pay-per-mile providers that penalize regular drivers, OCHO's pay-as-you-go model ensures affordable, accessible coverage for everyone—especially those living paycheck to paycheck.

Pay-as-you-go insurance availability varies by state due to different insurance regulations. OCHO currently offers pay-as-you-go options in Arizona, Georgia, Illinois, Missouri, New Mexico, Texas, Washington, and Wisconsin, with plans to expand to additional states soon. Check your state's availability for the most current information.

With pay-per-mile insurance, your premium increases directly with your mileage. Most providers cap the daily charge (typically at 250 miles per day) to prevent excessive charges for occasional long trips. However, consistently driving more than anticipated will result in higher bills, potentially exceeding what you'd pay with traditional or pay-as-you-go insurance.

Yes, you can typically switch between insurance models when your policy renews, though mid-term changes may be more difficult. Consider your anticipated driving patterns for the upcoming term before deciding which model makes more sense financially.

No. Both payment models offer the same coverage types and limits as traditional insurance. You can still select liability, comprehensive, collision, and other standard coverages with either option. The difference lies solely in how you pay, not what's covered.

Some pay-as-you-go providers, including OCHO, report on-time payments to credit bureaus, which can help build your credit history. This added benefit makes pay-as-you-go insurance particularly valuable for drivers working to establish or improve their credit scores.

Both pay-as-you-go and pay-per-mile insurance offer valuable alternatives to traditional payment models, but they serve distinctly different needs. Understanding these differences helps you choose the option that aligns with your driving habits, financial situation, and personal preferences.

For most regular drivers, especially those seeking payment flexibility without usage tracking, pay-as-you-go insurance provides the ideal balance of convenience and consistency. For infrequent drivers looking to minimize costs based on limited usage, pay-per-mile offers potential savings.

At OCHO, we believe insurance should work with your life, not against it. Our pay-as-you-go model represents the smarter way to stay covered without the financial stress of large premium payments or the limitations of mileage-based pricing.

Ready to explore how pay-as-you-go insurance can make coverage more manageable? Get a free quote today and experience the OCHO difference.

OCHO does not guarantee an increase to your credit score, and individual results may vary. It's important to make on-time payments, but other factors can affect your credit score, including performance on other credit accounts.

.svg)