We’ve all been there—bills piling up, paychecks stretched thin, and tough choices about what gets paid this month. When money’s tight, car insurance might seem like an expense you can temporarily put on hold. After all, what’s the worst that could happen if you miss a payment or two? 🚗💨

This situation is known as a car insurance lapse, and there are some common reasons why these lapses occur. Most often, drivers experience a lapse due to missed payments, forgetting to renew their policy, or switching insurers without making sure there’s no gap between policies.

Unfortunately, a lapse in insurance coverage—even for just a few days—can trigger a cascade of unexpected consequences that affect your finances for years to come. From premium hikes to license suspensions and even wage garnishment, the costs of an insurance gap extend far beyond what most drivers realize.

In this article, we’ll explore what happens when you experience a lapse in insurance coverage, the surprising ways it affects your future rates, and most importantly, how you can avoid these gaps even when money is tight.

An insurance coverage lapse occurs any time you own a registered vehicle that isn’t continuously protected by an active insurance policy. A lapse can occur for various reasons, including but not limited to:

Even a single day without coverage counts as a lapse—and insurance companies have sophisticated tracking systems that detect these gaps, no matter how brief.

🦉Ocho says, “Many drivers don’t realize that reinstating a canceled policy doesn’t erase the gap period from your record. That ‘fixed’ gap still counts against you!”

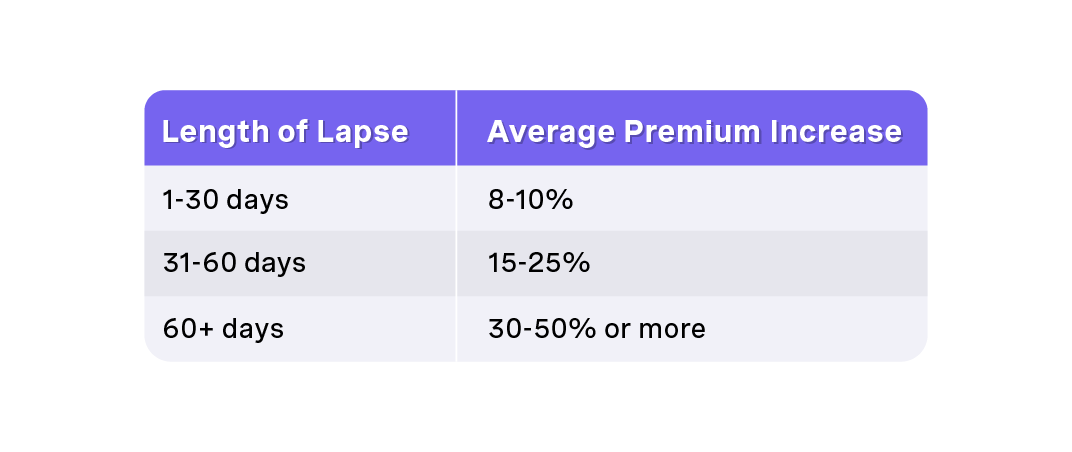

Here’s something most insurance companies don’t advertise: if you’ve had a lapse in insurance coverage within the past 200 days, you’re automatically flagged as “high-risk” and pushed into what’s called the “non-standard” insurance market.

If your lapsed policy extends beyond 200 days, you may be forced into the non-standard insurance market, where premiums can be 30–100% higher than standard rates.

This industry secret is one of the primary reasons why people get trapped in a cycle of expensive insurance. Once you’re categorized as non-standard, you face:

What’s particularly frustrating is that this penalty applies regardless of why your coverage lapsed. Whether you were a perfect driver who simply missed a payment because your paycheck was delayed, or you intentionally canceled your policy—the 200-day rule treats everyone the same. If you need to purchase a new policy after a lapsed policy, you’ll likely face higher premiums and stricter terms, making it even harder to get affordable coverage.

Wondering how insurance companies know about your coverage history? It’s not magic—it’s data sharing.

Most insurers use services like LexisNexis’ Current Carrier Report (C.L.U.E.) to view your complete insurance history. This report shows:

When you apply for insurance, this report is automatically pulled, instantly revealing any lapses in your history. And because this data is shared industry-wide, you can’t hide a lapse by simply switching to a new insurance company.

It’s important to submit all claims and required documentation accurately and on time, as any delays or errors in submission can be tracked in your C.L.U.E. report and may impact your insurance record.

The traditional insurance payment system seems almost designed to create lapses for people living paycheck to paycheck. Here’s why:

Paying premiums on time is essential to avoid lapses in coverage, and low-cost, no-deposit pay-as-you-go car insurance options can make it easier to stay insured. The process for reinstating coverage during the grace period typically allows policyholders to pay the missed premium without losing coverage, with most insurers offering a 10 to 20-day grace period, usually 30 days for most insurance policies, and 15 to 30 days for health insurance. Additionally, some states require insurers to provide written notice before canceling a policy after a missed payment.

This rigid system doesn’t account for the financial reality of many working Americans. When the Federal Reserve reports that 37% of Americans would struggle to cover an unexpected $400 expense, it’s clear that the traditional insurance payment model needs rethinking, as does the decision of when to file a claim versus pay out of pocket—an issue explored in depth in guidance on when to pay out of pocket instead of filing an insurance claim.

When most people think about a lapse in insurance coverage, they worry about higher premiums or legal trouble. But there’s another risk that’s often overlooked—medical expenses. If your insurance policy lapses, your insurance company is no longer obligated to pay for any medical expenses incurred during that period. That means if you or someone else is injured in an accident while your coverage is inactive, you could be on the hook for every dollar of those medical bills, and without protections like gap insurance for a totaled vehicle you may also still owe money on a car that’s been written off.

This isn’t just a minor inconvenience. Medical expenses can quickly add up to thousands—or even tens of thousands—of dollars, especially if emergency care or hospitalization is needed. Without active insurance coverage, you lose the financial protection that helps cover these costs, and healthcare providers may not receive payment for services rendered during the lapse. In some cases, unpaid medical bills can lead to collections, damaging your credit and financial stability even further.

Policy lapses don’t just impact you—they can also create headaches for healthcare providers, who may struggle to collect payment for care provided during an uninsured period. That’s why it’s so important for policyholders to maintain continuous coverage and make premium payments on time. If you’re approaching the end of your grace period or realize you’ve missed a payment, take immediate action to reinstate your policy. Acting quickly can help you avoid the serious consequences that come with a lapse, including the risk of being left to pay out-of-pocket for major medical expenses.

By staying proactive and keeping your insurance coverage active, you protect yourself from unexpected financial burdens and ensure you have the support you need if the worst happens. Don’t let a brief lapse lead to long-term medical debt—make continuous coverage a top priority.

At OCHO, we understand the challenges of maintaining continuous insurance coverage when you're living paycheck to paycheck. Our mission as a company is to redesign car insurance so hardworking drivers can stay protected, including through offerings like seguro de automóvil económico de OCHO for Spanish-speaking drivers. That's why we've designed a system specifically to help prevent lapses:

Traditional insurers might require $500+ upfront to start a policy—an impossible amount for many. OCHO offers no deposit car insurance with our interest-free financing program, allowing you to get covered with as little as $0 down in many cases.

Our most popular feature allows you to schedule your insurance payments to arrive just after your paycheck does. This simple adjustment aligns your insurance with your cash flow, dramatically reducing the chances of missed payments.

While traditional insurers give you only 10 days to make a late payment, OCHO extends this window to help you avoid the dreaded lapse. Sometimes those extra few days make all the difference between maintaining coverage and facing years of higher rates.

For drivers already stuck in the "penalty box" due to past lapses, OCHO offers special programs designed to help you rebuild your insurance history and escape the high-premium non-standard market faster. You can review how OCHO works and common FAQs to see how these programs fit into our overall system.

Many insurers add late fees, reinstatement fees, and other charges that make it even harder to catch up after falling behind. OCHO eliminates these barriers to help you maintain continuous coverage.

Maria, a retail worker in Texas, had a flawless driving record but missed an insurance payment when her hours were cut. Her policy was canceled after the 10-day grace period, and even though she reinstated coverage just three days later, the damage was done. Drivers in nearby states like California can face similar challenges, which is why understanding California car insurance with $0 down and flexible coverage is so valuable.

When it came time to renew six months later, her premium had jumped from $1,200 to $1,920—an extra $720 she couldn't afford. This led to another lapse, creating a vicious cycle that took years to escape, even though she could have explored instant car insurance options to get covered the same day.

Had Maria been with OCHO, our extended grace period and flexible payment options would have prevented her initial lapse entirely, just as our Missouri car insurance with fast, affordable $0 down coverage is designed to help drivers there avoid gaps.

Carlos had been stuck in the high-premium market for two years following a brief lapse in coverage. Every six months, he faced the same challenge: come up with a $600 down payment or lose his insurance again, a situation that many drivers in places like Washington seeking fast, affordable car insurance quotes online also want to escape.

After switching to OCHO, Carlos qualified for our zero down car insurance program, similar to our broader zero down car insurance coverage, and aligned his payments with his biweekly paychecks, an approach that also underpins our Wisconsin car insurance with affordable $0 down options. Within eight months (over 200 days) of continuous coverage, he was able to transition back to standard insurance rates, saving over $800 per year.

Curious whether past lapses are affecting your current rates or whether OCHO is available where you live? Here’s how to find out, starting with reviewing car insurance by state FAQs from OCHO:

After a lapse, you may also need to check if you are eligible for coverage with certain insurers, as eligibility criteria can change based on your coverage history. If the lapse involved health insurance, be aware that it can impact a patient's eligibility for coverage or claims.

We believe that a brief financial hiccup shouldn't lead to years of insurance penalties. That's why everything about OCHO is designed to help you maintain continuous coverage:

Now that you understand the serious consequences of a lapse in insurance coverage, here are your next steps:

Remember, the best time to address a potential insurance lapse is before it happens. If you’re concerned about making your next payment, reach out to us today to explore your options.

Ready to escape the lapse penalty box? Visit OCHO.co now to get a quote and see how our flexible payment options can help you maintain continuous coverage—even when money is tight.

Ocho’s wisdom: “The path to affordable insurance starts with never letting your coverage slip away!” 🦉

This blog post is for informational purposes only and does not constitute professional insurance advice. Coverage options, terms, and conditions may vary by state and individual situation.

Compare & get covered fast

Find and compare auto insurance in minutes, and get your free credit score.

Choose when you pay

Select payment dates that line up with your payday.

Manage everything in one place

Track your policy, manage payments, and request a payment extension right from your dashboard.

.svg)