If you drive a car in America, you need insurance. It’s the law in almost every state, and it’s the difference between a manageable inconvenience and financial disaster when something goes wrong on the road.

Auto insurance is essentially a contract between you and an insurance company. You pay a premium, and in return, they agree to cover certain losses—whether that’s damage you cause to someone else’s property, injuries from an accident, or theft of your vehicle. In 2026, most states require at least liability insurance to register and operate a vehicle legally. California, New York, Texas, and the vast majority of other states mandate some form of coverage, though New Hampshire and Virginia offer alternative proof-of-financial-responsibility rules.

This guide will answer the questions that actually matter: What coverage do I need? How much does it cost? And how do I buy it? Consider this scenario from 2024: A driver rear-ends another vehicle at a stoplight, causing $15,000 in vehicle damage and $30,000 in medical bills for the other driver. Without insurance, that’s $45,000 out of pocket—enough to devastate most household budgets. With proper liability coverage, the insurance company handles it.

Auto insurance is a contract: you pay a premium, and the insurer pays for covered losses up to your policy limits when you file a claim. That’s the fundamental exchange at the heart of every policy.

Here are the key concepts you need to understand:

Let’s make this concrete. Imagine a 2025 fender-bender in Illinois where you’re at fault. Your liability coverage pays for the other driver’s vehicle repairs ($8,000) and their medical bills ($12,000). You don’t pay those costs directly—your insurer handles them within your policy limits.

Different coverages pay for different things. Liability covers damage you cause to others. Collision covers damage to your own car from accidents. Comprehensive coverage handles non-collision events like theft or hail damage. Medical payments coverage addresses injury costs for you and your passengers.

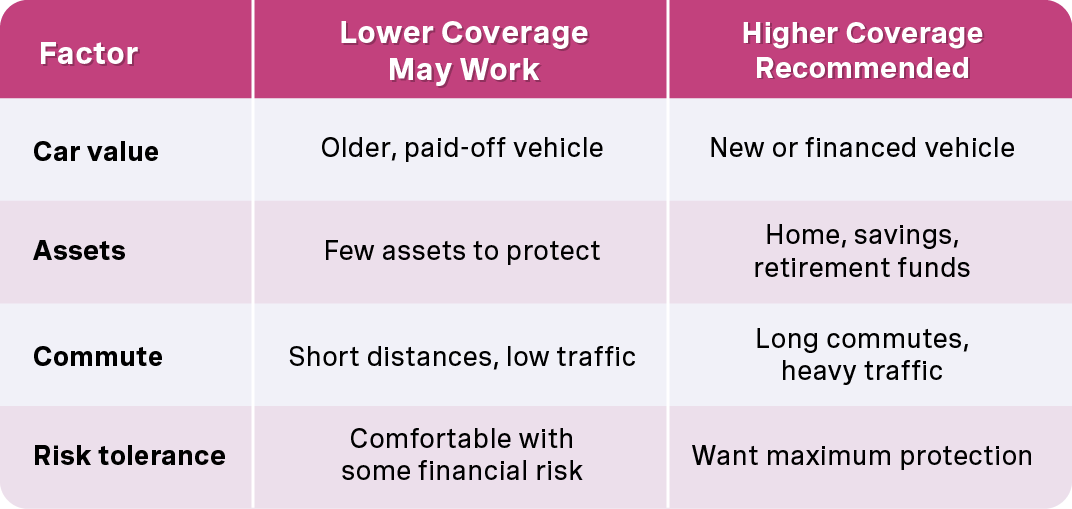

One important note: if you have a loan or lease on your vehicle, your lender will almost certainly require more coverage than the bare state minimum. They’re protecting their investment, which means you’ll typically need comprehensive and collision coverage until the car is paid off.

State minimums are legal baselines—not recommendations for adequate financial protection. Meeting the minimum keeps you legal, but it may not keep you financially secure after a serious accident.

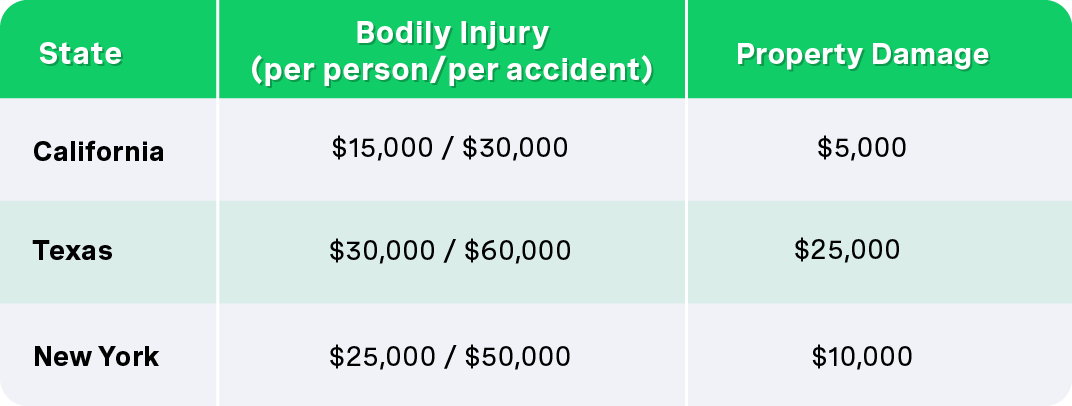

State laws set minimum liability limits using a format like “15/30/5.” Here’s what California’s minimum means in real dollars:

Those numbers might sound reasonable until you consider that a single hospital stay can easily exceed $100,000, and a new car costs over $48,000 on average in 2025. If you cause an accident with damages exceeding your limits, you’re personally responsible for the difference.

Drivers with assets—savings accounts, home equity, retirement funds—usually need much higher liability limits, such as 100/300/100 or more. The more you have to protect, the more coverage makes sense.

Some states have unique systems that affect your coverage decisions:

When deciding how much insurance you need, consider these factors:

One auto policy bundles several distinct coverages together—some required by law in most states, others optional. Think of it like a menu where the appetizers are mandatory and the entrees are your choice.

The following sections walk through each major coverage type with practical examples from 2023–2026. Keep in mind that exact availability and terminology vary by state and insurer, so check your own state’s insurance department website for specifics.

Liability coverage pays for bodily injury and property damage you cause to others when you’re the at fault driver in an accident. This is the coverage required in almost every state.

It has two components:

Here’s how minimum limits compare across three states:

These minimums are often dangerously low for serious accidents. A multi-vehicle crash with injuries can easily generate $200,000 or more in claims. If your coverage tops out at $30,000, you’re personally liable for the rest.

Liability does not pay for your own injuries or your own car repairs—that’s what other coverages handle. If you have a home, savings, or other assets, choosing higher limits (100/300/100 or more) provides much better protection against lawsuits and judgments.

Medical payments coverage is optional in many states and pays medical expenses for you and your passengers regardless of fault, up to your chosen limit. It’s straightforward: you get injured in a crash, MedPay helps cover doctor bills, hospital stays, and related costs.

Personal injury protection goes further. This broader no-fault coverage may include:

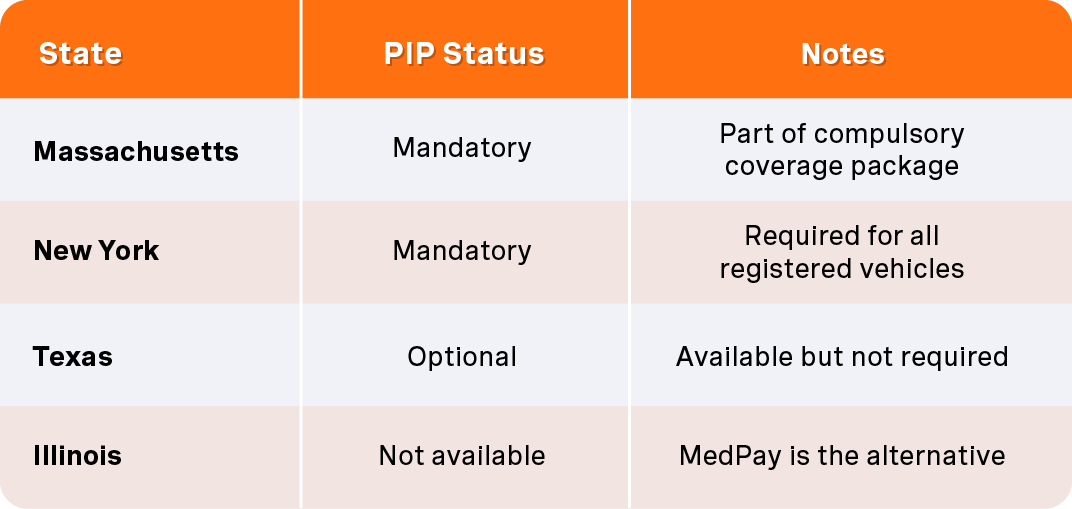

State requirements vary significantly:

In a no fault state, PIP claims are typically the first payment source for injuries from a crash, before liability claims against the other driver are pursued. If you have health insurance with high deductibles or limited coverage, MedPay or PIP can fill important gaps.

Coordinate your coverage amounts with your existing health insurance deductibles and out-of-pocket maximums. If your health plan has a $5,000 deductible, having at least that much in MedPay makes sense.

Uninsured motorist coverage protects you when a driver who hits you has no insurance at all—or disappears in a hit-and-run. Underinsured motorist coverage helps when the at fault driver’s liability limits are too low to cover your actual losses.

Here’s a scenario that happens more often than you’d think: In 2024, you’re injured in a collision that causes $75,000 in medical expenses and lost wages. The at-fault driver carries only a $25,000 bodily injury limit—the state minimum. Your underinsured coverage steps in to cover the $50,000 gap.

Some states require this coverage:

According to industry data, roughly 12-14% of drivers nationwide are uninsured. In some states like Mississippi and New Mexico, that number exceeds 20%. If you live in or drive through high-uninsured-rate areas, stronger UM/UIM limits are worth serious consideration.

Collision coverage pays to repair or replace your car after a crash with another vehicle or object—a guardrail, a telephone pole, another car—regardless of who’s at fault. You pay your deductible, and insurance covers the rest up to your vehicle’s actual cash value.

Common deductible options:

Lenders and leasing companies typically require collision coverage on financed vehicles—especially cars purchased new in 2022 or later. They want to ensure their collateral is protected.

But here’s the thing: collision coverage may not make financial sense for older, low-value vehicles. If your car is worth $4,000 and you’re paying $400 annually for collision coverage (10% of the car’s value), you might be better off self-insuring and saving that premium money.

Simple rule: When annual collision premiums approach 10% or more of your car’s market value, it’s time to reconsider whether the coverage is worth it.

Comprehensive coverage handles non-collision damage—all the things that can happen to your car when you’re not actually driving it into something.

This includes:

Real examples from recent years: In 2024, Colorado experienced several major hailstorms that destroyed windshields and dented thousands of vehicles. In 2023, catalytic converter thefts in California reached epidemic levels, with thieves targeting certain models. A deer collision in Pennsylvania can cause $4,000+ in damage before you know what happened.

Like collision coverage, comprehensive insurance uses a deductible and is typically required by lenders on financed vehicles. You should review your comprehensive coverage when your vehicle’s market value (check Kelley Blue Book or similar resources) has dropped significantly.

However, if you live in areas prone to hurricanes, wildfires, or severe storms, maintaining comprehensive coverage—even on older vehicles—provides meaningful protection against total loss scenarios.

Beyond the core coverages, insurers offer several optional add-ons worth knowing about:

Rental reimbursement: Pays for a rental car while yours is being repaired after a covered claim. Usually $30-50 per day with a total limit.

Roadside assistance coverage: Covers towing, lockout service, flat tire changes, and jump starts. Similar to AAA but through your insurance company.

Gap insurance: Essential for new cars. If you total a 2023 or 2024 vehicle and owe $28,000 on your loan but the car’s actual cash value is only $22,000, gap insurance covers the $6,000 difference. Without it, you’d owe money on a car you can no longer drive.

Custom equipment coverage: Protects aftermarket additions like upgraded stereo systems or custom wheels that aren’t covered by standard policies.

Non-owner liability policies: For people who regularly rent or borrow cars but don’t own one themselves.

Classic car insurance: Specialty coverage for collector vehicles with agreed values—like that 1969 Mustang that’s worth more restored than when it was new.

Before adding optional coverages, check for duplication. Your credit card might already include rental car coverage. Your auto club membership might cover roadside assistance. Your employer benefits might offer something similar. Avoid paying twice for the same coverage.

Your premium is what you pay for coverage—and costs vary wildly based on who you are, what you drive, and where you live.

Key rating factors that affect your car insurance rates:

Higher coverage limits and lower deductibles increase your premium. Safe driving records, multi-policy discounts, and telematics programs can reduce them.

Warning: Driving uninsured carries serious consequences beyond accident liability. In Massachusetts, you face fines up to $500 and license suspension for operating without insurance. In Texas, penalties include fines up to $1,000, license and registration suspension, and potential impoundment of your vehicle. The money you “save” by skipping insurance rarely covers these penalties—let alone an accident.

Insurers group drivers into risk tiers or classes based on demographic and behavioral factors, then adjust for individual circumstances like your specific accident history and claims.

Here’s what significantly increases premiums:

State regulations affect what factors insurers can use. Some states limit age or gender as rating factors. All insurer rate filings must be approved by state insurance regulators, providing some consumer protection against arbitrary pricing.

When you receive your renewal documents, review the declarations page to see exactly how much you’re paying for each coverage type. This breakdown helps you identify where you might adjust to save money without sacrificing essential protection.

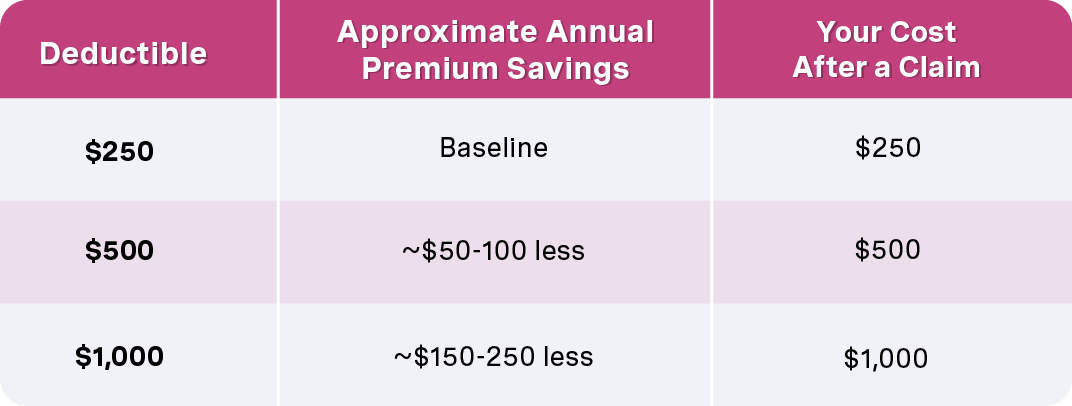

Your deductible is the amount you pay out of pocket before collision or comprehensive coverage kicks in after a covered claim. It’s money that comes directly from your pocket before insurance pays anything.

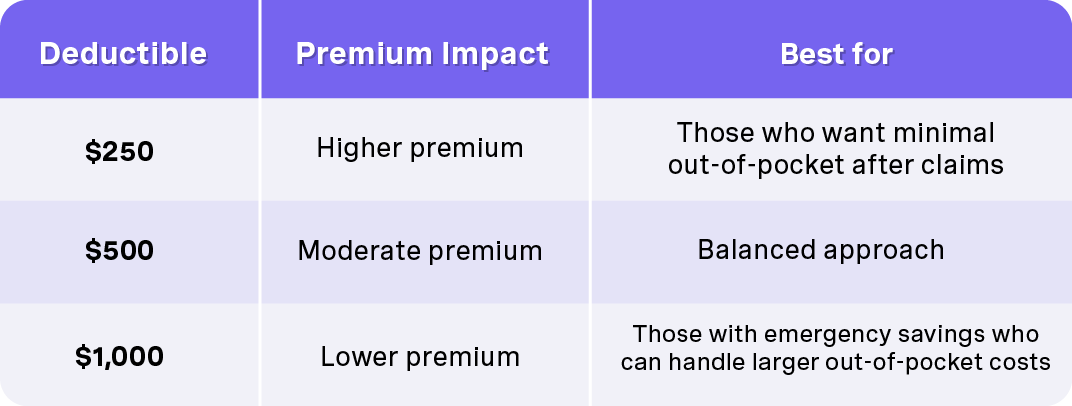

Here’s how common deductibles affect both your premium and your out-of-pocket cost after a claim:

Rule of thumb: Choose the highest deductible you can comfortably pay in cash after an unexpected accident. If you have $2,000 in emergency savings, a $1,000 deductible is reasonable. If you’re living paycheck to paycheck, a lower deductible provides more protection—even if it costs more monthly.

The premium savings from a very high deductible can backfire badly if you can’t afford repairs when something happens. Review your deductible choice annually, especially after changes in your emergency fund or your vehicle’s value.

Buying auto insurance follows a logical progression whether you’re a first-time buyer or switching insurers at renewal time:

The market is competitive, so getting multiple quotes can lead to substantial savings without reducing coverage. Before you start, gather what you’ll need:

You can buy through several channels:

The critical point: compare quotes on the same coverage limits, deductibles, and options. A $100/month quote with $50,000 liability limits isn’t comparable to a $150/month quote with $300,000 limits. Match the coverages, then compare prices.

Here’s the practical process:

Don’t let the lowest price be your only decision factor. An insurer with terrible claims service or shaky financials isn’t a bargain—it’s a risk.

Many drivers overpay simply because they never update coverages or shop around after that first policy purchase. Money left on the table adds up over years.

Savings opportunities come from two directions:

Smart cost-cutting tips:

Important: Don’t sacrifice essential protections just to cut costs. Dropping liability to state minimums might save money monthly but expose you to devastating personal liability. Focus on smarter adjustments, not dangerous ones.

Common discounts to ask about:

Check eligibility for group or affinity program discounts through:

Telematics programs can reward consistently careful driving with premium reductions of 10-30%. If you don’t drive aggressively, this can translate to real money.

Review optional coverages like roadside assistance or rental reimbursement. If your credit card, automaker warranty, or auto club already provides similar benefits, you’re paying twice.

And in states where credit-based insurance scoring is permitted, improving your credit profile over time can reduce premiums at renewal.

Accidents happen. Knowing the claims process beforehand reduces stress when you’re already dealing with vehicle damage or injuries.

The general sequence:

Reporting deadlines and documentation requirements vary by insurance company, so read the claims section of your policy before you need it. When describing the incident, accuracy and honesty are critical—misrepresentations can lead to denied claims or policy cancellation.

At the scene:

After the scene:

The adjuster process:

You can usually choose your repair shop, though some insurers have preferred networks with guaranteed work. Understanding this process beforehand means fewer surprises when you’re already stressed.

Many drivers assume “everything” is covered when, in fact, exclusions and limits are the norm. Your coverage always depends on the specific policy language and the options you selected.

Personal auto policies are intended for private passenger use—not every possible vehicle-related activity. Review your policy’s exclusions page and ask your agent about any unclear scenarios.

Typically covered:

Typically NOT covered:

Business use exclusions: Personal auto policies typically exclude coverage when you’re using your vehicle for business. This includes rideshare driving (Uber, Lyft) or delivery work (DoorDash, Amazon Flex) unless you purchase special endorsements. Many drivers don’t realize their regular policy won’t cover them during these activities.

Intentional acts: If you deliberately damage your vehicle or someone else’s property, that’s not covered. Insurance is for accidents, not crimes.

Racing and competition: Driving on a track or competing in any kind of speed event voids coverage.

Mechanical breakdown: Your transmission failing or your brakes wearing out isn’t a claim—it’s maintenance. Some insurers offer mechanical breakdown coverage as a separate product.

International driving: Coverage typically ends at the U.S. and Canadian borders. Driving into Mexico usually requires a separate Mexican auto insurance policy.

If you have unusual risks—using a truck for commercial hauling, for example—discuss appropriate specialized coverage with a licensed agent. The cost of proper coverage is far less than the cost of being uninsured when something goes wrong.

The best policy for you combines state requirements, your personal risk factors, your budget, and your vehicle’s value into coverage that actually protects you.

Your checklist:

Review and update your policy annually—especially after moving, changing vehicles, getting married, or adding a teen driver to your policy. What worked last year may not be optimal this year.

The “best” auto insurance isn’t necessarily the cheapest. It’s coverage that fits your specific situation, offers reliable claims service from a financially stable insurance company, and remains affordable over time.

Your action items for this week:

You now have everything you need to make informed decisions about your auto insurance. The question is: are you currently getting the coverage you actually need at the best car insurance rates available? There’s only one way to find out—start comparing.

Compara y obtén cobertura rápido

Encuentra y compara seguros de auto en minutos y obtén su puntaje de crédito gratis.

Elige cuando pagar

Selecciona fechas de pago que coincidan con tu día de pago de sueldo.

Gestiona todo en un solo lugar

Realiza un seguimiento de tu póliza, administra los pagos y solicita una extensión de pago directamente desde tu perfil.

.svg)