Finding car insurance in Texas when money is tight feels like being punished for not having enough of it. But legal coverage doesn't have to drain your bank account. Here's everything you need to know about getting insured without going broke.

When people search for "low income car insurance Texas," they're not looking for a government handout. They're looking for ways to meet the law without choosing between insurance and groceries. In 2026, many drivers across the state face this exact dilemma as inflation, rising medical costs, and higher vehicle prices push premiums upward. The average full coverage policy in Texas now runs around $2,200–$2,480 per year - a significant expense for any family, let alone one on a tight budget.

Affordable car insurance doesn't mean the absolute cheapest policy with zero protection. It means choosing coverage car insurance that keeps you legal with bare-minimum liability or gives you more protective options, while still letting you pay rent. Options exist whether you're in Houston, Dallas, San Antonio, or a small rural town, though prices vary dramatically by ZIP code and driver profile. Even with low income, prior tickets, or poor credit, you can find coverage - you just need to understand how texas insurers price policies.

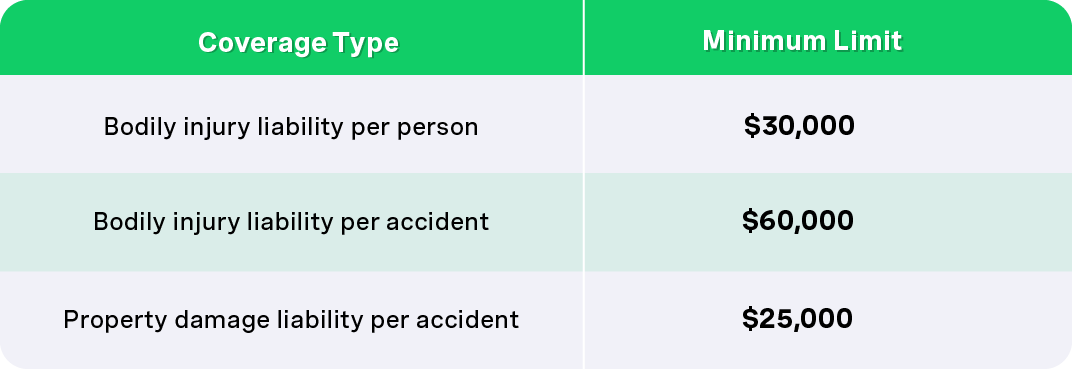

Every person who drives in Texas must carry liability insurance meeting these minimum limits:

Texas raised minimum coverage limits in 2008 from the previous 20/40/15 standard. These limits apply statewide - Houston, Austin, El Paso, smaller towns, everywhere. Police can verify your coverage electronically through the TexasSure database, so a lapsed policy can flag you even without a traffic stop.

Here's what minimum liability coverage does not do: it doesn't cover repairs to your own vehicle, your own medical costs, or damage from weather events. It only pays for injuries and property damage you cause to others. If your vehicle is financed or leased, your lender will almost certainly require full coverage (liability plus collision plus comprehensive), regardless of your income level.

Let's be direct: Texas does not have a state-sponsored low income car insurance program. Unlike California or New Jersey, which offer subsidized plans for qualifying drivers, Texas leaves it to the private market, so drivers must rely on affordable car insurance options for low-income drivers available through private companies and specialized programs.

That said, if you've been denied coverage by at least two car insurance companies, you can apply through TAIPA - the Texas Automobile Insurance Plan Association. TAIPA helps high-risk drivers by assigning them to a participating insurer. You'll get basic liability coverage, personal injury protection, and uninsured/underinsured motorist coverage, but no collision or comprehensive options. And TAIPA rates are often higher than what you'd find shopping around on your own.

Before turning to TAIPA, exhaust your options: get quotes from budget-friendly insurers, independent agents, and online comparison tools. TAIPA is a safety net, not a first choice.

Liability only coverage is almost always the cheapest path to staying legal. For many drivers, minimum coverage runs roughly $60–$100 per month, compared to $175–$241 per month for full coverage. Drivers can reduce costs significantly by purchasing state minimum liability coverage on older, paid-off vehicles.

Consider this comparison:

If your car is worth less than about $4,000–$5,000, dropping collision and comprehensive often makes financial sense. But if you depend on that car to get to work, losing it in a total loss with no coverage to replace it is a real risk you need to weigh.

The cheapest isn't always the best. If you use OCHO for easy, free car insurance quotes, you can get access to full coverage options that you normally wouldn't be able to afford upfront because we spread the cost for you - low down payments, easy installments, and the protection you actually need.

Texas insurers can't directly ask about your income, but they use factors that strongly correlate with it. The biggest one? Your credit history. Credit-based insurance scores are legal under Texas law, and drivers with poor credit can pay up to 70% more for insurance than those with good credit for the exact same coverage options. According to the Insurance Research Council, this pricing gap disproportionately affects low income drivers who are already stretched thin.

Key rating factors that affect your premium:

Many drivers in Houston and Dallas pay significantly more than the national average due to heavy traffic, higher claim frequency, and elevated theft risk. Meanwhile, mid-sized cities like San Antonio or Lubbock tend to show more affordable rates. ZIP-level variance can exceed 200% for identical risk profiles, meaning where you park at night matters as much as how you drive.

Focus on what you can control: maintain a clean driving record, keep continuous coverage, drive fewer miles when possible, and work on gradually improving credit while applying proven ways to get cheap car insurance.

This isn't generic advice - it's a money-saving playbook. Here's how to actually lower your bill, especially if you're looking for affordable Texas car insurance quotes in minutes:

And here's what most people won't tell you: use OCHO. We get you a low down payment, easy installments, more time to pay when you need it, and you can even build your credit score. We take a bet on you when other companies won't, and you can see how OCHO works and answers common questions.

Discounts are one of the fastest ways to reduce premiums without gutting your coverage. Low-income drivers can find affordable coverage by utilizing company-specific discounts that many people never even ask about, especially when paired with no deposit, $0 down car insurance options.

Common savings opportunities:

Take a defensive driving course for a 5% to 10% discount - a Texas-approved six-hour online defensive driving course costs about $25 and the savings can last up to three years. Discounts for defensive driving and paperless billing combined can make a meaningful dent.

Stacking 2–4 discounts together can cut a low-income driver's premium by 20%–40%. That could be the difference between affording coverage and going uninsured, and many of these savings opportunities are explained in OCHO's frequently asked questions about coverage and pricing.

Car insurance in Texas varies sharply by city, so understanding your local cost patterns matters. Large metro areas like Houston, Dallas, and Fort Worth typically carry the highest rates due to congestion, elevated claim rates, and theft risk. Some ZIP codes in Dallas can push liability-only rates to double what a suburban driver pays.

Cities like San Antonio, El Paso, and Corpus Christi tend to show moderate average premiums, though specific neighborhoods vary. Rural counties and smaller towns may offer lower base rates, but fewer local agents mean online or phone-based shopping becomes more important, particularly with flexible pay as you go car insurance coverage.

Compare quotes not just by city but by your specific ZIP code. Texas insurers price risk at a very local level, and a move across town can sometimes save you hundreds per year compared to other states.

Skipping insurance to save money almost always backfires, especially for low-income households. Here's what you're looking at:

Driving without insurance in Texas can lead to fines up to $1,000 - and a single no-insurance ticket plus SR-22 costs can easily exceed a full year of minimum liability coverage. The math doesn't lie: staying insured is cheaper than getting caught uninsured, and you can review the wider penalties and risks of driving without insurance to see how quickly costs add up.

Follow this checklist over the next 30–60 days:

Comparing quotes from different insurers is vital due to varying rates - the savings from 30 minutes of shopping can protect your finances for an entire year.

No. Texas does not have a state-supported low income car insurance program. All standard policies come from private car insurance companies. TAIPA exists as a last-resort assigned-risk plan, but its rates are often higher than regular market policies and coverage options are limited. Treat TAIPA as a backup only after at least two companies have formally refused to insure you.

The lowest-cost legal option is usually a minimum liability-only policy meeting the 30/60/25 requirement. Texas Farm Bureau offers some of the lowest rates at around $30 monthly for qualifying drivers. While this is often the cheapest car insurance available, it may not be enough to protect your own car if you depend on it for work. Even a few extra dollars per month toward slightly higher liability limits can help you avoid large out-of-pocket costs after an accident.

Yes. Drivers with no credit history or poor credit can still get insured, but premiums are often higher. GEICO, for instance, provides relatively low rates for drivers with poor credit. Look for non-standard carriers and pay-per-mile options that weigh miles driven more heavily than credit. Basic credit-building steps - on-time bill payments, lower card balances - can slowly reduce your premiums over the next 12–24 months.

Major insurers generally do not offer car insurance discounts tied directly to SNAP, EBT, Medicaid, or similar benefit programs. However, low-income status may indirectly qualify you for low-mileage, pay-per-mile, or basic-coverage policies that cost less overall. Always ask agents about hardship plans, flexible billing, or alternative rating programs for budget-conscious drivers.

Contact your current insurer immediately to ask about changing coverage, raising deductibles, or switching to liability-only. Compare quotes from budget-oriented insurers and explore pay-per-mile or telematics programs. If you encounter a security solution or security service block on a comparison website - sometimes triggered when a certain word, sql command, or malformed data is submitted, or if online attacks cause the site owner to enable protections showing a cloudflare ray ID - try clearing your browser or using a different device. You may see a cloudflare ray id found at the bottom of those pages, which the site owner can use to troubleshoot. The action you performed triggered the security block, but it's usually temporary. Driving uninsured is risky and expensive. If absolutely necessary, consider carpooling, public transit, or rideshare while working to afford at least minimum coverage, and review real customer reviews of OCHO's affordable plans to see how other budget-conscious drivers stay insured.

Compara y obtén cobertura rápido

Encuentra y compara seguros de auto en minutos y obtén su puntaje de crédito gratis.

Elige cuando pagar

Selecciona fechas de pago que coincidan con tu día de pago de sueldo.

Gestiona todo en un solo lugar

Realiza un seguimiento de tu póliza, administra los pagos y solicita una extensión de pago directamente desde tu perfil.

.svg)