If you've been staring at your car insurance bill wondering "Why is my car insurance so high?", you're not alone. Car insurance rates have increased dramatically across the United States, with the average full coverage policy in 2025 now costing over $2,300 annually—a 15% increase from just one year ago.

More than half of Americans have noticed their car insurance rates going up in the past year, leaving many drivers frustrated and searching for answers. The truth is, your high car insurance rates likely result from a combination of factors—some you can control, and others you can't.

This comprehensive guide will reveal the hidden reasons your rates might be so high and, more importantly, show you practical strategies to lower them. Whether it's fixing a factor you didn't know was affecting your rates or finding an insurer that works with your situation rather than against it, there are solutions available.

OCHO says, "High rates don't have to be permanent—once you understand what's driving them up, you can take action to bring them down!" 🦉

This is one of the biggest factors pushing drivers into expensive "non-standard" insurance, yet most people have never heard of it. If you've had any gap in car insurance coverage within the past 200 days—even just a few days—insurance companies automatically flag you as "high-risk" and charge significantly higher rates.

The impact is severe. Drivers with recent coverage gaps can pay 30-100% more than those with continuous coverage, regardless of their driving record quality. The gap doesn't have to be your fault—payment processing errors count against you. Even if you reinstated a canceled policy, the gap still counts, and the 200-day clock resets with each new gap.

Real-World Example: Maria had a flawless 10-year driving record but missed an insurance payment when her hours were cut at work. Her policy canceled for just 3 days before she reinstated it. At renewal, her rates jumped from $1,200 to $1,920 annually—a $720 increase for a 3-day gap.

OCHO's solution addresses this problem head-on. Our extended grace periods and flexible payment schedules help prevent these costly gaps from occurring in the first place. Learn more about no deposit car insurance options that can help maintain continuous coverage.

In most states where OCHO operates, your credit score can impact your insurance rates more than your driving record. Insurance companies use credit-based insurance scores, which are different from regular credit scores, to predict claim likelihood. Poor credit can increase your rates by 50-100% or more.

Consider this shocking example: In OCHO markets like Arizona, Georgia, Illinois, Missouri, New Mexico, Texas, Washington, and Wisconsin, credit scoring is heavily used. A driver with poor credit might pay $2,400 annually while an identical driver with good credit pays $1,200.

Several hidden factors affect your insurance credit score beyond what you might expect:

This system seems unfair to many drivers. People with poor credit due to medical bills, job loss, or other circumstances are often very safe drivers, but they're penalized with higher insurance rates anyway.

OCHO's approach differs significantly from traditional insurers. We report your on-time insurance payments to credit bureaus, helping improve your score over time. Our flexible payment schedules help ensure on-time payments, and we don't penalize you excessively for past credit issues while you're working to improve.

Where you live can impact your rates more than how you drive, and the differences can be extreme even within the same city. Several factors make your area "high-risk" from an insurance perspective, including crime rates (particularly vehicle theft and vandalism), traffic density, weather patterns, litigation trends, uninsured driver rates, and expensive healthcare costs.

The examples are shocking when you look at specific regions:

What you might not know is that moving just a few miles can dramatically change your rates. Even "good" neighborhoods can be expensive due to high vehicle values, and your specific address matters—different sides of the street can have different rates based on historical claim data.

OCHO's advantage lies in understanding regional challenges and working to provide competitive rates regardless of your location within our service areas.

External economic factors are driving up insurance costs industry-wide, affecting everyone's rates regardless of personal circumstances.

Vehicle costs have increased dramatically, with new car prices averaging over $45,000. Used car values remain elevated from pandemic impacts, and more expensive cars mean higher replacement costs, which translates to higher premiums for everyone.

Repair costs have similarly skyrocketed. Advanced technology in modern vehicles costs significantly more to repair than older, simpler systems. Parts shortages drive up replacement part costs, labor costs have increased significantly across the automotive repair industry, and materials cost more due to general inflation.

Medical costs continue to outpace general inflation. Healthcare inflation exceeds general inflation rates, more expensive treatments are available (driving up potential claim costs), and longer life expectancies mean longer-term care costs for serious injuries.

The legal environment has also changed dramatically. Larger jury awards in injury cases have become common, more sophisticated personal injury litigation increases costs, and social inflation—society's tendency toward larger settlements—impacts all insurance lines.

What this means for you is that even if nothing about your personal situation has changed, external factors are pushing everyone's rates higher.

The specific vehicle you drive affects your rates in ways you might not expect, beyond just its value. While everyone knows sports cars cost more to insure and luxury vehicles have higher premiums, several hidden factors might surprise you.

Theft popularity plays a major role in determining rates. Honda Civics and Toyota Camrys are frequently stolen, not because they're valuable, but because they're easily resold. Luxury cars aren't always the most stolen—thieves often prefer easily resold common models.

Repair complexity has increased dramatically with modern vehicles. Cars with advanced driver assistance systems cost significantly more to repair than traditional vehicles. Even minor accidents can result in expensive sensor recalibration that didn't exist in older cars.

A safety ratings paradox exists in modern insurance. Very safe cars protect occupants well but may cause more damage to other vehicles in accidents. Some safety features are expensive to repair or replace, and advanced airbag systems are costly to replace after deployment.

Age and value interactions create complex pricing scenarios. Cars 7-12 years old often hit a "sweet spot" of lower theft rates but reasonable repair costs. Very old cars may have expensive-to-find parts, while classic or vintage vehicles need specialized coverage.

OCHO's vehicle-friendly approach means we don't penalize you excessively for your vehicle choice and can help you understand the insurance implications before you buy.

How you pay for insurance and structure your policy can significantly impact your total costs in ways that aren't immediately obvious.

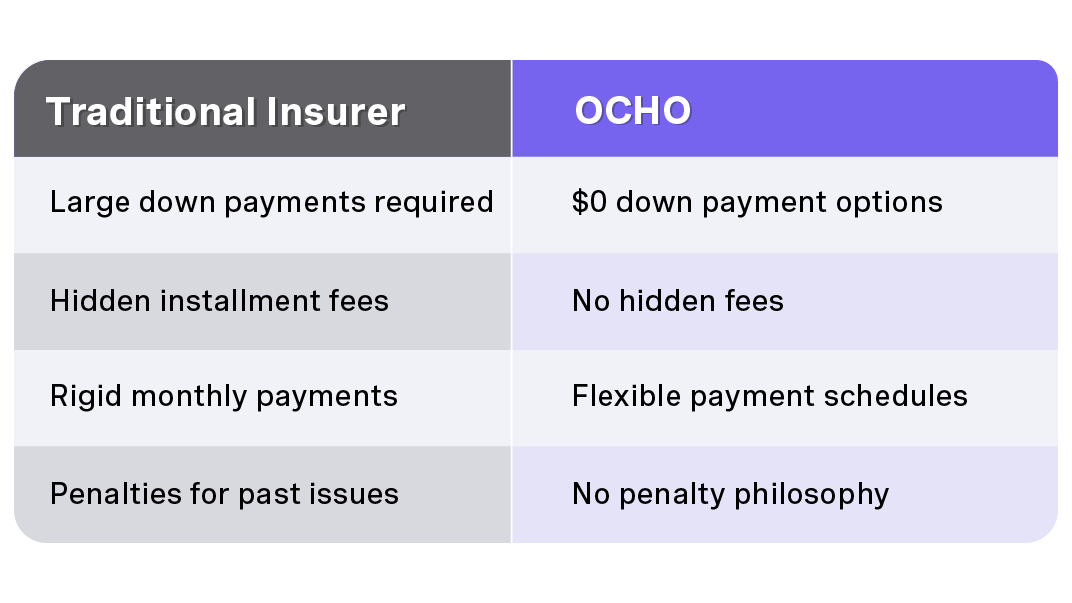

Down payment penalties hit many drivers hard. Many insurers require large down payments for "high-risk" drivers—sometimes 25-50% of your six-month premium. This creates a double penalty: you pay more for coverage and need more cash upfront to get it.

Payment frequency charges add up over time. Monthly payments often include "installment fees" of $3-8 per month, and these can add $50-100+ to your total annual cost. Some insurers charge different rates based on payment frequency, meaning the same coverage costs more if you pay monthly instead of annually.

Hidden fees accumulate throughout the policy period, including policy fees ($25-75 annually), cancellation fees if you switch insurers, reinstatement fees if your policy lapses, and processing fees for payment method changes.

OCHO's transparent approach eliminates these problems entirely.

Insurance companies use sophisticated algorithms that may work against certain groups of drivers, creating systematic disadvantages.

Loyalty penalty practices affect long-term customers disproportionately. Some insurers raise rates on customers who are less likely to shop around, new customer discounts expire leaving existing customers paying more, and rate increases may be applied gradually to avoid triggering departures.

Credit and income profiling creates systematic advantages for some groups. Affluent ZIP codes often get better rates regardless of actual risk, and high credit scores can outweigh poor driving records in pricing decisions.

Market segmentation strategies create tiers of service. Premium brands target affluent customers with better service and rates, while non-standard brands often provide expensive options for excluded customers.

OCHO's fair approach stands apart from these practices. We focus on your future potential, not past problems. Our pricing is transparent and doesn't rely on hidden penalties, and we serve customers others might consider "non-standard" with respect and fair rates.

OCHO was designed specifically to address the problems that make insurance expensive and difficult to maintain for real people in real situations.

Addressing payment barriers is central to our approach. Our zero down payment coverage allows you to get full coverage without large upfront costs through our no down payment car insurance program. Interest-free financing means no hidden charges, removing the biggest barrier to adequate coverage.

Flexible payment schedules align with your actual financial reality. You can align payments with your paycheck schedule through our pay-as-you-go car insurance options—weekly, biweekly, or twice-monthly—reducing financial stress and payment timing issues.

Use our car insurance calculator to estimate how much you could save with the right coverage levels.

Extended grace periods provide breathing room when life happens. We provide more time to make payments without policy cancellation, understanding that life happens and timing varies. This prevents the costly 200-day gap rule from affecting you.

Credit and history building features help improve your long-term situation. On-time insurance payments are reported to credit bureaus, helping improve your credit score over time. Better credit leads to lower insurance rates, creating positive momentum for overall financial health.

If your rates are too high, here's your comprehensive action plan broken down into manageable phases.

Days 1-2: Research and Compare Start by getting quotes from at least 3-5 different insurers, including OCHO. Ensure you're comparing identical coverage levels and factor in down payment requirements and payment flexibility. Research customer service ratings and claim handling reputation for each company.

Days 3-4: Optimize Your Application Gather documentation for all possible discounts you might qualify for. Consider different deductible levels and their impact on premiums. Review your coverage needs based on your current financial situation and calculate total first-year costs including any down payments or fees.

Days 5-7: Make Your Decision Choose the best overall value, not just the lowest price. Ensure the insurer can accommodate your payment schedule needs, verify all discounts are properly applied, and set up your new policy before canceling your old one to avoid coverage gaps.

Focus on credit score enhancement by paying all bills on time consistently, reducing credit card balances below 30% of limits, checking credit reports for errors, and avoiding new credit applications unless absolutely necessary.

For driving record protection, focus on defensive driving habits, use traffic apps to avoid high-risk times and areas, consider taking a defensive driving course for immediate discounts, and maintain your vehicle properly.

Policy optimization involves taking advantage of new discount opportunities, adjusting coverage as your vehicle depreciates, building an emergency fund to handle higher deductibles, and reviewing coverage needs if circumstances change.

Build positive insurance history by maintaining continuous coverage for at least 200 days to escape high-risk classification. Make all payments on time, work with OCHO's flexible payment options to maintain consistency, and avoid any coverage gaps.

Address root causes by continuing to improve your credit score, maintaining a clean driving record, considering how life changes might affect rates, and building financial stability to afford better coverage options.

Don't let high insurance rates continue draining your budget. If your rates are unaffordably high right now:

You can also explore our car insurance comparison tool to see how different options stack up.

If your car insurance feels unaffordably expensive, you're not powerless. While some factors driving high rates are beyond your control—like economic inflation and industry trends—many others can be addressed with the right knowledge and strategy.

The key is understanding that high insurance rates often result from a combination of factors: coverage gaps, credit issues, location factors, vehicle choices, and industry practices that may work against certain groups of drivers. Once you identify which factors are affecting your rates, you can take targeted action to address them.

OCHO was specifically designed to help drivers who've been struggling with high rates from traditional insurers. Our zero down payment options remove upfront barriers, flexible payment schedules help prevent coverage gaps, and our focus on building positive payment history helps customers transition to better rates over time.

Remember: your current insurance situation doesn't have to define your future. With the right approach—maintaining continuous coverage, improving your credit, optimizing your coverage levels, and working with an insurer that understands your challenges—you can achieve affordable rates that provide real protection.

Ready to escape the high-rate trap? Get your instant OCHO quote now → and discover how our innovative approach to insurance can help you get quality coverage at a price that fits your budget. Don't let another month pass paying more than you should for car insurance.

Compare & get covered fast

Find and compare auto insurance in minutes, and get your free credit score.

Choose when you pay

Select payment dates that line up with your payday.

Manage everything in one place

Track your policy, manage payments, and request a payment extension right from your dashboard.

.svg)