If you’re looking for affordable car insurance without a big upfront payment, you might have come across Hugo. Since launching in 2020, Hugo has quickly become popular. Hugo has over 31,400 Trustpilot reviews with an average rating of 4.8, and 89% of those are 5-star ratings. That’s impressive for any insurer, especially a new digital one. Hugo is known for its easy online process, instant coverage, and simple sign-up.

Hugo does not charge hidden fees, emphasizing a transparent pricing model. Hugo Insurance lets you use their turning coverage feature, allowing you to turn your coverage on only when you need it and off when you’re not driving.

However, most reviews don’t mention that Hugo’s model has changed a lot, so what worked in 2023 might not be the best choice now.

If you're researching Hugo Insurance, you're likely looking for affordable, flexible coverage options. However, before making a decision, it's important to understand both Hugo's limitations and how OCHO's comprehensive approach provides a more sustainable solution for most drivers. OCHO offers pay-as-you-go prices with no-deposit, and on full coverage insurance.

Hugo Insurance is a real option and can be a great help for some drivers. If you don’t drive much, have an older car that’s paid off, and only need the minimum required coverage, Hugo’s small payment system could help with saving money compared to regular monthly plans. It’s especially useful if you want to keep upfront costs low and only pay for the coverage you actually use.

But Hugo does have some real drawbacks. It’s only available in about 15 states and mostly offers liability-only coverage. There’s no roadside help or rideshare coverage, and the popular Flex plan ended in March 2025. The biggest issue is that if your balance runs out and auto reload doesn’t work, you could quickly lose coverage, which can lead to DMV problems and registration issues. Hugo works best for people who just need the minimum required insurance or needed insurance and want flexible, on-demand coverage.

If you want steady coverage without worrying about turning payments on and off, OCHO takes a different route. We offer $0 or very low down payments, let you split payments to match your paychecks, don’t charge late fees, give you instant proof of insurance, and even help you build credit with on-time payments. You get continuous coverage with flexible payments, no need to switch your insurance on and off.

Quick Comparison:

Compared to other car insurance companies, Hugo stands out for its flexible payment model, but may not always offer the lowest prices or the broadest coverage options.

Some customers feel that the 'pay as you go' benefit does not always align with their experience, sometimes leading to higher premiums, and dissatisfied customers have complained about higher rates compared to other carriers for liability coverage.

Hugo customers value the micropayment options and instant proof of insurance, which make it easy to get covered quickly and pay only for the days they need.

Hugo started in 2020, first serving drivers in Illinois and then expanding to about 15 states by 2026. Unlike most insurance companies, Hugo acts as a broker and managing general agent, so it doesn’t underwrite the policies itself.

Here’s how the Hugo website model works:

Hugo works with partner carriers that have their own ratings (Aspire B+ from A.M. Best, First Acceptance A+ from BBB), but Hugo itself doesn’t have an A.M. Best rating because it isn’t the actual insurer.

To really understand what Hugo offers, you have to look past the marketing. Hugo’s policies come with different coverage options and requirements to fit different drivers. There are three main options: Flex, Unlimited Basic, and Unlimited Full. Hugo is available in only 16 states, which limits its coverage options and availability.

Right now, most people can only get liability-focused coverage from Hugo in most states. If you’re hoping for full coverage with extras like comprehensive and collision, you’ll probably be disappointed unless you live in a specific area. Basic provides state-minimum liability coverage—meaning bodily injury and property damage protection (think limits like 25/50/25 depending on your state).

What’s included:

What Hugo does NOT provide coverage for:

This plan is good for drivers who use their car regularly and want affordable payments. It’s not a fit if you have a financed or leased car, since your lender will require more than just liability coverage.

Hugo has promoted an “Unlimited Full” plan that includes liability, comprehensive, collision, medical, and rental benefits. It sounds great in theory.

But as of 2026, this plan is very hard to find. In many states, you can’t buy it at all. Even where it’s available, it usually has fewer features than traditional full coverage from other insurers, with no rideshare coverage and limited extras.

If you have a financed car, check Hugo’s current availability for your ZIP code before assuming you can get coverage. Don’t rely on old ads.

The Flex plan was what first made Hugo popular. It was a real pay-as-you-go option where you could buy coverage for 3, 7, 14, or 30 days and turn it on or off whenever you wanted.

Here’s why it’s gone:

Hugo stopped selling new Flex plans in March 2025 and moved current users to Unlimited Basic. The takeaway is that overly flexible insurance can cause problems for most drivers.

Hugo’s current system isn’t really “pay per day” anymore. It’s more like short-term billing on a regular liability policy.

Here’s the typical flow:

Hugo’s micropayment model allows customers to start their policy by paying for only three or seven days of coverage, depending on their state.

It really is convenient. You don’t have to wait weeks for policy documents, pay a big down payment, or worry about hidden fees.

But there’s a catch. If your payment method fails and auto reload doesn’t work, your coverage can end in just a few days. That’s when trouble can begin.

Many Hugo customers prefer making small, frequent payments rather than a single monthly bill. But they sometimes don’t realize how quickly things can go wrong.

What happens with lapses:

At OCHO, we do things differently. We spread out your down payment and premium over the policy term, so you keep continuous coverage while making small, predictable payments. This way, you get affordable payments without the risk of turning your coverage on and off.

If you drive most days, the real question is not only about flexible payments, but whether you want those payments with or without coverage gaps.

Hugo is still a niche provider. They started in Illinois in 2020 and have grown to about 15 states by 2026, but availability can change and needs to be checked.

Common eligibility restrictions:

Always check Hugo’s website with your ZIP code to see if coverage is available for you. Blog posts from 2023 may not show the current situation.

OCHO works with multiple partner insurers throughout various U.S. states, helping drivers with imperfect credit find carriers willing to write policies—then financing the upfront cost so you’re not stuck waiting with no coverage.

Hugo works well for:

Hugo Insurance's focus on micropayments can be especially beneficial for drivers who do not drive frequently, as opposed to traditional insurers that typically require larger upfront payments.

Think twice if you:

Hugo’s Trustpilot reviews are impressive, with over 31,000 reviews and an average rating of about 4.8 out of 5. Around 89% of those are five-star ratings, which is rare for any insurance company.

Hugo's customer service has received mixed reviews, with some indicating difficulty in reaching support representatives.

What customers praise:

Common complaints:

Hugo replies to about 97% of negative reviews within 24 hours, showing they actively manage their reputation.

Across reviews, a few patterns emerge:

Reddit and forum users have warned that DMV problems can happen after even short lapses in coverage. Sometimes, just a few days without payment caused registration issues.

The bottom line is that Hugo is a real company and helps many people, but its unique setup means you need to fully understand how payments and coverage work together before you sign up.

Here’s something that confuses many Hugo customers: when you file a claim, you’re not dealing with Hugo at all.

Claims go directly to underwriting partners like First Acceptance or Aspire General. That means:

Be sure to save your Hugo account login and your carrier’s claims contact information as soon as you get coverage. You’ll need both. Hugo is not accredited by the BBB and is better suited for individuals seeking quick, basic coverage rather than high-end, full-service insurance.

Filing a claim with Hugo Insurance is designed to blow up everything you hate about the Old Timer insurance game—no more waiting in endless lines like cattle, no more drowning in ridiculous paperwork mountains, and definitely no more getting trapped in those soul-crushing phone trees that lead nowhere. Whether you're dealing with a fender bender or something that's turned your world upside down, Hugo's digital-first approach means you can beat the system and handle your car insurance claim quickly and efficiently, right from your phone or computer. We're here to set the record straight on how claims should work.

Here's how to make sure your claim goes smoothly, so you can get back on the road without the insurance industry bleeding you dry:

Thinking about dropping your Hugo insurance policy? Here's the deal - they've made it extremely user-friendly and you can knock it out directly through your online account or just hit up Hugo's support team. This digital-first approach means no more waiting on hold like some kind of medieval torture! No mailing paperwork either - just a few clicks and boom, your plan is history.

Before you make that move, you absolutely need to understand what's coming your way. Canceling your Hugo policy is going to leave you with a lapse in coverage unless you've got another policy ready to roll. Hugo's going to notify the state DMV about this lapse - that's just how the game works. And trust us, this can trigger some serious headaches like registration suspension or even sky-high premiums when you're shopping around with other insurance companies later. Some insurers? They might straight-up deny coverage if they spot a recent gap in your history!

Want to avoid these nightmare scenarios? Here's what the smart people do: always, always secure a new insurance policy before you cancel your current one. This keeps your continuous coverage intact and shields you from unexpected costs or legal disasters. If you're mainly worried about the cost of your current plan, why not try adjusting your coverage levels or evaluating different payment options within your Hugo account first? Sometimes, switching to a different plan or tweaking your liability coverage can help you save serious money without risking that dangerous lapse.

Bottom line? While canceling Hugo insurance is simple enough, the real secret sauce is planning ahead and protecting yourself from the ripple effects that a coverage gap can unleash on your life. Don't let a simple cancellation turn into your worst financial nightmare!

When you're picking car insurance, here's what the Old Timers will tell you: check the financial strength of whoever's covering you. But let's get real about Hugo for a second—they're not like these crusty traditional insurers. Hugo operates as a broker and managing general agent, which means they're not stuck in the old-school underwriting game. Instead, they've teamed up with companies like First Acceptance and Aspire General Insurance Company to shake things up.

These partner carriers? They've got a B+ (Good) rating from A.M. Best, which is the industry watchdog everyone talks about. Look, this rating tells you these companies can actually pay out when you need them to, which is pretty essential if you ask us. Sure, Hugo doesn't have its own A.M. Best rating, but here's the thing—they're not playing by the same broken rules as everyone else. Their ability to get you covered and pay claims depends on these solid partners they've chosen.

You want some real advice that nobody else is giving you? Do your homework on any insurance company's financial ratings and reputation—we're talking serious security verification here. Whether you're after liability coverage or going full coverage, knowing your insurer won't leave you hanging when disaster strikes is absolutely crucial. Don't let anyone tell you otherwise.

Hugo's got an innovative approach to car insurance with flexible coverage and instant proof of insurance, pretty appealing if you're tired of the same old insurance runaround. But here's what we're telling you: weigh that convenience and affordability against financial stability because that's what really matters when the chips are down. Do your due diligence, make sure your insurance company's got the security to back you up, and then you can confidently pick a policy that'll actually be there when everything goes sideways.

Both Hugo and OCHO solve the same core problem: insurance is too expensive upfront for many drivers.

Hugo’s solution was micropayments and, historically, on/off coverage. It worked for some, but created DMV headaches for others.

OCHO tackles affordability differently. As a digital auto insurance agency and broker, we help you compare real-time quotes from multiple carriers, then finance the down payment so you can split costs across your policy term—without toggling coverage off.

OCHO benefits:

If Hugo represents “pay only when you drive,” OCHO represents “pay affordably while always being covered.”

Consider OCHO if you:

Simple decision rule: if you drive most days and don’t want to think about turning insurance on and off, OCHO’s model fits much better than Hugo’s.

One of the biggest differences between OCHO and companies like Hugo is that we make real coverage affordable from day one. Instead of asking drivers for a big, impossible down payment, OCHO breaks your insurance into smaller, predictable payments that fit your budget. So you can have quality insurance at pay-as-you-go prices.

This is real customer feedback: “I was so stressed out. Every insurance company wanted so much without comprehensive and collision. You all made it so much easier I am overjoyed and my stress has been lifted. Thank you very very much. I now have full coverage 3 times less than all the other insurance companies I applied for. Again thank you!!!!!!!!!”

With OCHO, you don’t have to choose between paying rent, buying groceries, or keeping your car insured. Our payment plans vary by state, but the goal is always the same: make starting and keeping coverage easy.

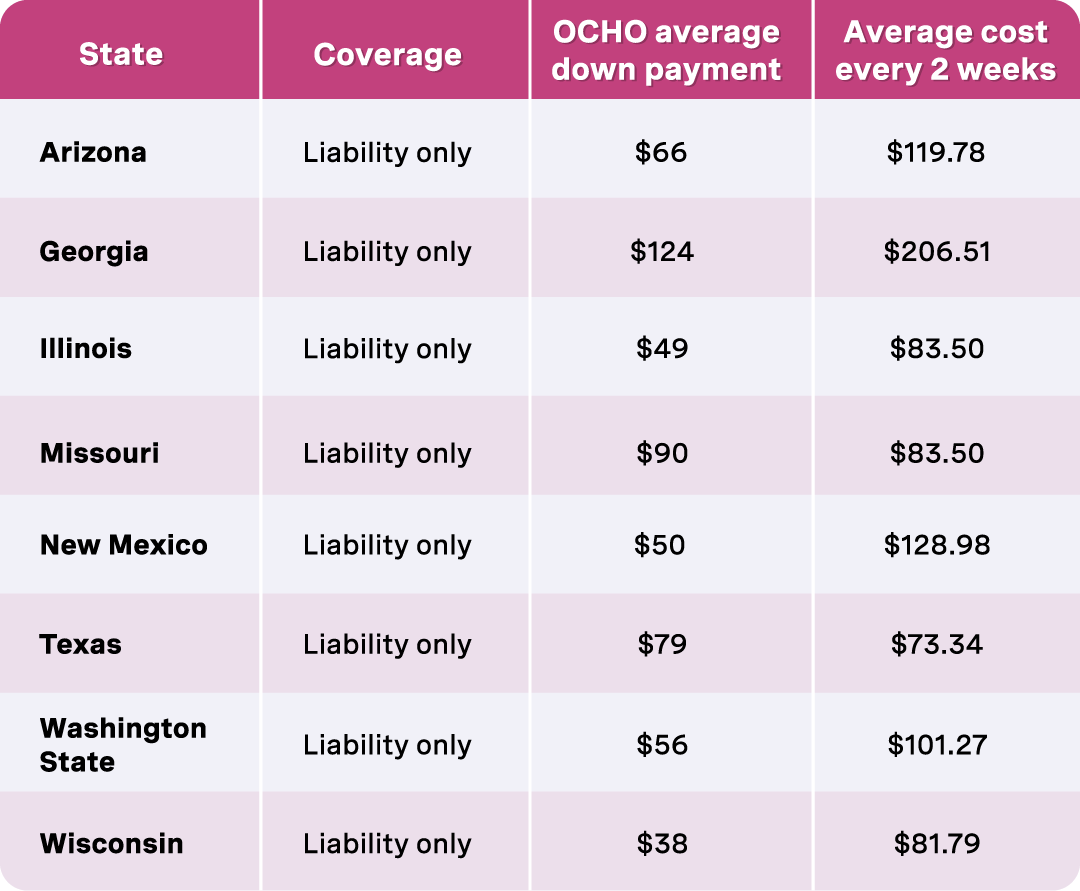

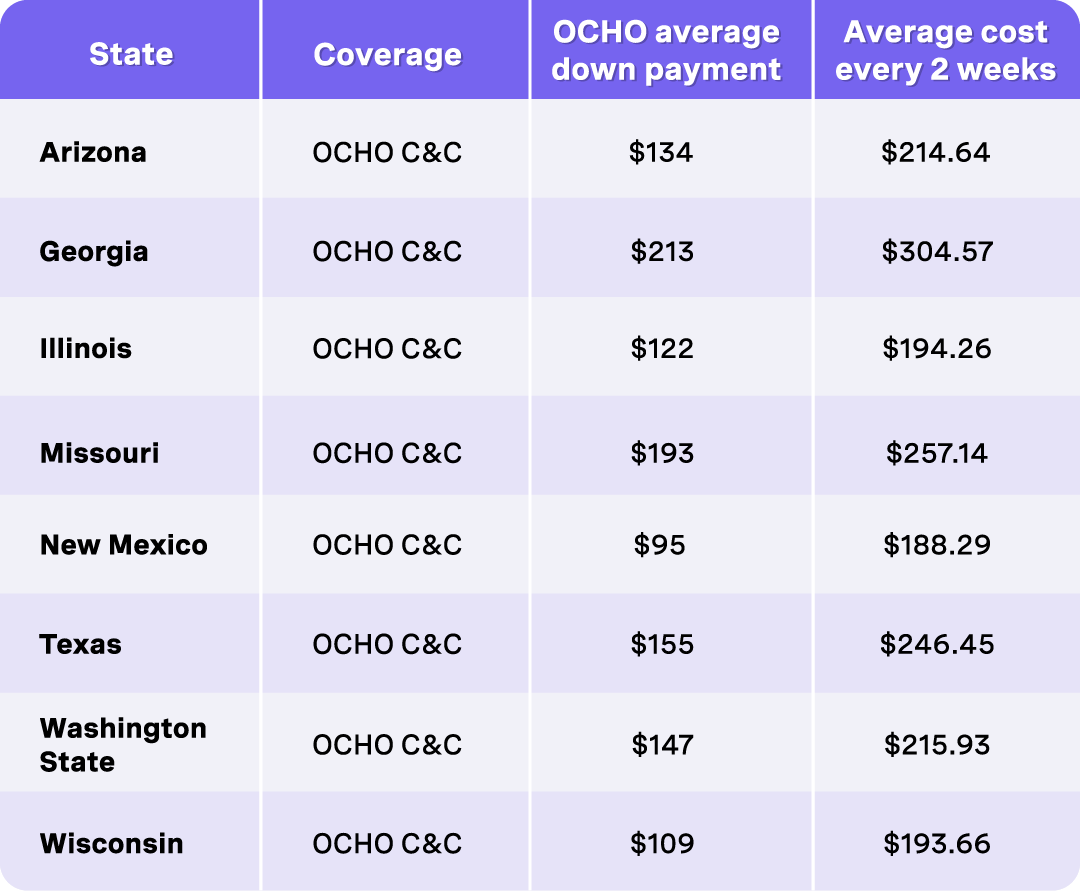

Below is a simple breakdown of how OCHO’s payment structure works in each state we serve. This table shows:

Hugo's focus on state-minimum liability coverage may seem cost-effective initially, but it exposes drivers to significant financial risks:

If you cause an accident resulting in $50,000 in damages but only have Hugo's minimum $30,000 liability coverage, you're personally responsible for the remaining $20,000 – plus any damage to your own vehicle, which isn't covered at all.

We help you understand your actual coverage needs and provide options that protect both your vehicle and your financial future. Our flexible payment plans make comprehensive coverage accessible without the financial strain of large upfront payments.

Hugo's customer reviews consistently mention difficulty contacting customer service representatives, creating frustration when drivers need assistance with claims or policy changes.

At OCHO, we understand that most drivers need more than temporary fixes. Our approach addresses the real challenges working families face:

Financial Accessibility

Unlike traditional insurers that require large down payments, OCHO offers $0 down options and flexible payment plans that align with your paycheck schedule. We don't believe financial barriers should prevent you from getting proper auto insurance.

Coverage That Actually Protects

While Hugo leaves you vulnerable with minimum coverage, OCHO provides comprehensive car insurance options that protect both your vehicle and your financial future. Our full coverage plans include comprehensive and collision protection, so you're covered for theft, vandalism, weather damage, and accidents.

Building Better Financial Futures

OCHO's payment reporting helps build your credit score over time, while our consistent coverage approach helps you qualify for lower rates. Instead of keeping you trapped in high-risk categories, we help you build toward better financial stability.

Preventing Coverage Gaps

Our extended grace periods and flexible payment options help you maintain continuous coverage even during temporary financial challenges. This prevents the coverage gaps that can damage your credit and push you into higher-risk premium categories.

Making the Right Choice for Your Future

While Hugo Insurance offers an innovative approach to ultra-short-term coverage, their limitations make them unsuitable for most drivers' needs. Hugo's small size, sparse coverage options, and limited coverage areas mean many drivers won't be able to access policies through Hugo.

OCHO provides a comprehensive solution that addresses both immediate affordability concerns and long-term financial stability. Our innovative payment options, comprehensive coverage choices, and commitment to customer success make us the smarter choice for drivers who want both affordability and proper protection.

Don't let limited coverage options leave you financially vulnerable. While Hugo Insurance's minimum liability coverage might meet legal requirements, it won't protect you from the real financial risks of driving.

With OCHO, you get:

Stop settling for minimum coverage that leaves you exposed. At OCHO, we believe everyone deserves access to comprehensive, affordable auto insurance that builds toward a better financial future.

Unlike Hugo's limited liability-only approach, OCHO offers real protection with payment plans that make quality coverage accessible. Our innovative financing options, extended grace periods, and commitment to helping you build better credit make us the smart choice for drivers who want both affordability and comprehensive protection.

Get your free quote today and discover how OCHO's comprehensive approach provides the protection you need at a price you can afford.

Finally, car insurance you can afford.

Start your OCHO journey today.

Compare & get covered fast

Find and compare auto insurance in minutes, and get your free credit score.

Choose when you pay

Select payment dates that line up with your payday.

Manage everything in one place

Track your policy, manage payments, and request a payment extension right from your dashboard.

.svg)