Shopping for car insurance in 2026 can feel overwhelming, but comparing car insurance quotes from multiple providers is one of the most effective ways to save money while improving your coverage. This article will provide practical tips for comparing car insurance quotes, ultimately helping you purchase the right policy for your needs. According to NerdWallet’s analysis, drivers who take time to compare quotes can save over $1,300 annually—a significant amount that adds up over the life of a policy.

In this guide, you’ll learn exactly how to compare quotes step by step, what information you need to gather beforehand, and how to avoid common comparison mistakes that lead to inadequate protection. Keep in mind that quotes are estimates, not final rates. Your premium may adjust after underwriting reviews your credit, claims history, and other details. Shopping around every 6–12 months is essential because insurers regularly update their pricing models and discounts. Re-evaluating your car insurance regularly ensures you continue to get the best deal as rates and market conditions change.

Consider two 35-year-old drivers with identical 2022 Honda Civics. One receives a quote for $1,714 per year from Travelers while the other gets quoted $2,700 from Nationwide for the same coverage. The difference comes down to how each insurance company weighs factors like location, driving history, and even occupation. Insurance companies use proprietary algorithms to weigh risk, which is why rates for the same driver can vary significantly.

Auto insurance is essential protection for anyone who owns or drives a vehicle. It acts as a financial safety net, helping cover the costs that can arise from car accidents, theft, or damage to your car. When shopping for car insurance, it’s important to understand the different types of coverage available—such as liability, collision, and comprehensive—so you can choose the right coverage for your needs.

Car insurance rates are determined by several factors, including your driving record, where you live, the type of vehicle you drive, and even your claims history. Because these factors vary from person to person, car insurance quotes can differ widely between companies. Most insurance companies offer a variety of discounts, such as for safe driving, low annual mileage, or bundling your auto insurance with home or renters insurance.

To make sure you’re getting the best deal, it’s smart to compare auto insurance quotes from multiple companies. Don’t just look at the price—consider customer satisfaction ratings, the company’s claims history, and their financial stability. Shopping around and comparing different types of coverage and discounts can help you find the right policy at a competitive rate, ensuring you’re protected without overpaying.

Every car insurance quote starts with risk-based pricing. Insurers analyze hundreds of variables to predict how likely you are to file a claim and how expensive that claim might be. While many factors overlap between companies, each insurer weighs them differently, which explains why your quoted price can vary dramatically.

Here are the primary rating factors that affect your auto insurance quotes:

Driver age plays a significant role in car insurance rates. A 25-year-old typically pays more than a 45-year-old because younger drivers statistically have more accidents. Teen drivers can face premiums nearly double those of middle-aged drivers.

Location by ZIP code matters because urban areas with higher theft rates and traffic density cost more to insure than rural regions. A driver in Dallas will likely pay more than someone in rural Iowa, even with the same vehicle and driving record.

Vehicle type influences both repair costs and theft risk. A 2022 Honda Civic generally costs less to insure than a 2020 Ford F-150 because of differences in repair expenses, safety ratings, and replacement parts availability. Sports cars and luxury vehicles typically carry higher premiums.

Annual mileage directly correlates with accident risk. The more you drive, the more exposure you have. Someone commuting 25,000 miles per year will pay more than a remote worker driving 7,500 miles annually.

Driving record is one of the most heavily weighted factors. A clean record for five years typically lowers premiums significantly. A recent at-fault car accident or DUI can sharply raise rates—sometimes by 50% or more.

Credit-based insurance score is used in most states to predict claim likelihood. However, California, Hawaii, Massachusetts, and Washington restrict or ban credit score usage in auto insurance pricing, so availability varies and comparisons may work differently in those states.

Because each insurer applies different weights to these factors, the same person can see a $1,000 or more difference between two quotes. This is precisely why you need to compare multiple options.

You must decide what protection you want before requesting any quotes. Otherwise, you’ll be comparing apples to oranges, making it impossible to identify the best value. The cheapest option means nothing if it leaves you underinsured after an accident.

Mandatory coverages vary by state. Your state sets minimum liability requirements for bodily injury and property damage liability coverage. For example, Illinois requires minimums of 25/50/20 (meaning $25,000 per person for injuries, $50,000 per accident for injuries, and $20,000 for property damage). Florida has different requirements, including mandatory personal injury protection. Most states require some form of liability coverage, but about half also mandate uninsured motorist coverage or PIP.

Collision coverage pays to repair your vehicle after an accident, regardless of who was at fault. If you have a car loan or lease, your lender will likely require this coverage.

Comprehensive coverage protects against non-collision events like theft, vandalism, weather damage, or hitting a deer. This is also typically required if you’re financing your vehicle.

Uninsured/underinsured motorist coverage protects you when other drivers cause an accident but lack adequate insurance. Given that roughly 13% of drivers nationally are uninsured, this coverage provides essential protection.

Personal injury protection (PIP) and medical payments (MedPay) cover medical expenses for you and your passengers after an accident, regardless of fault. PIP is required in no-fault states.

When choosing liability limits, consider going beyond state minimums. Many drivers choose 100/300/50 instead of minimum requirements because medical bills and repair costs have risen substantially since 2020. A serious accident can easily exceed minimum policy limits, leaving you personally liable for the difference.

For your deductible—the amount you pay out of pocket before coverage kicks in—consider your emergency savings. A $1,000 deductible lowers your premium compared to a $500 deductible, but you need to be comfortable paying that amount within a few days if you file a claim.

Before requesting quotes, list your non-negotiables. Do you need rental reimbursement if your car is in the shop? Glass coverage for windshield chips? Roadside assistance? Gap insurance if you owe more than your car is worth? Knowing these details upfront ensures you’re comparing the same coverage options across all quotes.

Complete, accurate information prevents frustrating differences between your initial quote and final policy rate. Taking 15 minutes to gather everything beforehand saves time and ensures your comparison is meaningful.

Driver information needed:

Vehicle information needed:

If you already have car insurance, keep your current declarations page handy. This document shows your existing coverage limits, deductibles, and current premium—making it easy to match details when requesting new quotes. An insurance representative can provide this if you don’t have a copy.

Enter the same details every time you request a quote. Same drivers listed, same annual mileage estimate, same coverages and deductibles. If you tell one insurer you drive 10,000 miles per year and another 15,000 miles, your comparison becomes meaningless.

If you recently moved—for example, from New York City to a New Jersey suburb in 2024—updating your address can significantly change your rate, potentially saving hundreds of dollars or costing more depending on the new location’s risk profile.

Aim for at least 3–5 quotes from different companies to see a realistic price range. This gives you enough data points to identify outliers and understand what competitive pricing looks like for your specific situation.

Direct quotes from insurer websites let you get information straight from the source. Visit the websites of major carriers like GEICO, Progressive, State Farm, or Travelers and complete their quote forms. This approach works well for most insurance companies that have streamlined online quote processes.

Independent agents represent multiple insurers and can provide several quotes through one conversation. Unlike captive agents who work for a single company (like a State Farm agent who only sells State Farm), independent agents access many carriers and can help you compare quotes without visiting multiple websites.

Online comparison marketplaces like Insurify or Policygenius let you enter your information once and receive quotes from multiple insurers. These tools are useful for a quick overview, though final binding quotes often require additional verification on the insurer’s actual website.

A practical workflow: Start with one online comparison tool to get a quick price range, then request 2–3 direct quotes from top-rated carriers or local regional insurers for more detailed comparison. Regional insurers sometimes offer competitive rates that national comparison sites miss.

Get your quotes within a tight time window—ideally within the same week. Car insurance rates and discounts change frequently, so quotes obtained weeks apart may reflect different promotional pricing or rate adjustments.

Some insurers offer telematics or usage-based programs that track your driving behavior through a mobile app or device. These can discount safe drivers by 30–50%, but require sharing data about your braking, speed, and driving times. Decide in advance whether you’re comfortable with this trade-off before pursuing these options.

Price alone tells an incomplete story. You must compare coverage details, deductibles, and company quality to make a confident decision. A policy that costs $200 less per year but leaves you underinsured after an accident isn’t actually a bargain.

Step 1: Align coverage types and limits

Review each quote to ensure they include the same coverages: liability (bodily injury and property damage), collision, comprehensive, uninsured/underinsured motorist, and PIP if applicable. The coverage must match for a fair comparison.

Step 2: Check liability numbers

Liability limits appear as three numbers, such as 100/300/50. This means $100,000 per person for bodily injury, $300,000 per accident for bodily injury, and $50,000 for property damage. Ensure the same limits appear on each quote. A quote showing 25/50/25 will be cheaper than 100/300/50, but offers far less protection.

Step 3: Verify deductibles match

A higher deductible lowers your premium but increases out-of-pocket costs after a claim. Make sure you’re comparing identical deductibles across quotes.

Step 4: Review extras and add-ons

Check whether each quote includes rental reimbursement, roadside assistance, or accident forgiveness. These features add value but aren’t always included automatically.

Step 5: Read the fine print

Look for exclusions and special conditions. Does the policy cover aftermarket parts or only OEM? Are glass-only claims handled without affecting your deductible? Are there restrictions if you drive for a rideshare company? These details matter.

Step 6: Evaluate insurer strength and customer satisfaction

Look at third-party ratings. J.D. Power publishes customer satisfaction scores for claims handling. AM Best rates financial strength—important because you want your insurer solvent when you need to file a claim. Check your state insurance department’s complaint ratio to see how often customers report problems.

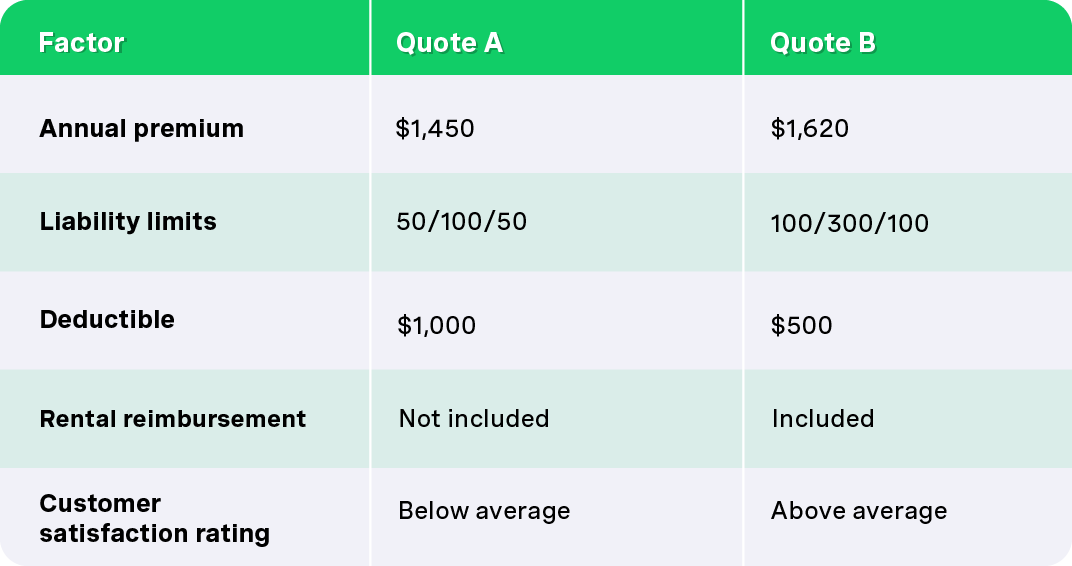

Example comparison:

Quote A looks cheaper, but Quote B offers significantly better liability protection, a lower deductible, rental reimbursement, and better customer satisfaction. If you cause an accident with serious injuries, Quote A’s lower limits could leave you personally liable for tens of thousands of dollars. Quote B provides better value despite the higher premium.

If your quotes come back higher than expected, several factors can lower your costs while keeping essential coverages intact.

Safe driver discounts reward those with clean driving records. Most insurance companies offer 10–20% off for drivers without accidents or violations for 3–5 years.

Multi-car discounts apply when you insure multiple vehicles on one policy, typically saving 10–25%.

Good student discounts benefit drivers under 25 who maintain a B average or better, often reducing premiums by 10–15%.

Anti-theft device discounts reward security features like alarms, GPS tracking, or steering wheel locks. A 2021 vehicle with factory anti-theft systems may automatically qualify.

Bundling discounts combine auto with home insurance or renters insurance, potentially saving up to 30%. This also simplifies billing and may improve your relationship with the insurer.

Adjusting your deductible is one of the most direct ways to lower your premium. Raising your collision deductible from $500 to $1,000 often reduces the premium noticeably. However, never choose a deductible higher than what you could pay within a few days—otherwise you risk being unable to repair your car after an accident.

Usage-based or pay-per-mile programs work well for low-mileage drivers. If you drive under 7,500 miles per year or work from home, these programs can reward consistent safe driving with discounts of 30% or more.

Dropping certain coverages on older vehicles may make financial sense. If your car’s current market value is under $3,000, the cost of collision coverage may exceed what you’d receive in a total loss claim. Check your vehicle’s value before making this decision, and ensure you can afford to replace it out of pocket.

The cheapest insurance policy can become extremely expensive after an accident if customer satisfaction is poor or claims handling is slow. Think of your policy as a long-term financial tool, not just a short-term expense.

Claims handling reputation matters. Research average claim resolution times and whether the insurer uses local adjusters or remote processes. Read recent customer reviews from 2022–2025, not outdated feedback from years ago. A company that lowballs claims or delays payments costs you money and stress when you need help most.

Digital tools and convenience affect your daily experience. Check the quality of the insurer’s mobile app—can you file and track claims online? Access digital ID cards? Reach 24/7 support via chat or phone? These features may seem minor until you’re stranded roadside at midnight.

Stable pricing and flexibility over several years often outweigh saving $50 in year one. Some insurers offer loyalty benefits or accident forgiveness after a set period, which can protect you from rate hikes after your first claim.

Conduct an annual policy review 30–60 days before renewal. Update your mileage if your commute changed, report life changes like a new job, marriage, or teen driver, and re-quote if your circumstances shifted significantly. What was the right coverage two years ago may no longer fit your auto insurance needs today.

A car insurance policy is a formal agreement between you and your insurance company that spells out exactly what is covered, how much coverage you have, and under what conditions your insurer will pay out. Each policy includes important details such as the vehicle identification number (VIN), information about all covered drivers, your chosen coverage options, policy limits, and deductibles.

Before you commit to a policy, take the time to review these details carefully to make sure the coverage matches your auto insurance needs. If you have questions, an insurance representative can walk you through the different types of coverage and help you identify discounts you may qualify for.

When comparing insurance quotes, always use the same coverage options, policy limits, and deductibles across all companies. This ensures you’re making an apples-to-apples comparison and can accurately judge which policy offers the best value. Look for insurance companies that provide personalized service, 24/7 claims support, and a variety of discounts to help you save on your premium. By understanding your policy and comparing your options, you can confidently choose the coverage that best protects you and your vehicle.

Comparing car insurance quotes effectively requires a systematic approach. First, define your coverage needs so you know exactly what protection you require. Second, gather accurate information including driver details, vehicle identification numbers, and your current insurance policy documentation. Third, obtain multiple quotes—at least three to five—from a mix of direct insurers, independent agents, and comparison websites.

Fourth, compare quotes line by line, ensuring identical coverage limits and deductibles. Don’t stop at price; evaluate customer satisfaction, claims handling reputation, and financial strength. Fifth, explore discounts and savings opportunities without sacrificing the right coverage for your situation.

An effective comparison focuses on both cost and protection. The goal isn’t finding the absolute cheapest option—it’s finding the best value for your specific needs. Set aside 30–60 minutes this week to collect at least three quotes using the checklist above. Request quotes with the same coverage options, review them carefully, and choose the policy that protects your finances without overpaying for coverage you don’t need. Your next renewal date is the perfect deadline to complete this process.

If you want quality coverage at pay-as-you-go prices, be sure to get a quote with OCHO!

Compare & get covered fast

Find and compare auto insurance in minutes, and get your free credit score.

Choose when you pay

Select payment dates that line up with your payday.

Manage everything in one place

Track your policy, manage payments, and request a payment extension right from your dashboard.

.svg)