So your car got pummeled by hail, a deer decided to play chicken with your bumper, or some vandal keyed your doors. You’re wondering: if I file this comprehensive claim, is my insurance company going to punish me with higher rates?

Let’s cut through the confusion and give you the real numbers—because nobody should have to decode insurance industry doublespeak just to figure out what a claim will cost them.

Yes, comprehensive claims can raise your insurance rates—but typically far less than at-fault collision or liability claims. A single comprehensive claim might bump your auto insurance premiums by around $30 to $70 per 6-month policy term, depending on your insurer, state, and claim size.

Here’s what you need to know right now:

Comprehensive coverage protects your vehicle from damage that doesn’t involve a collision with another car or stationary object. Think of it as your shield against the random chaos the world throws at your car—things completely outside your control.

When you file a comprehensive claim, you’re asking your insurer to cover repairs or replacement for non-collision damage. You’ll pay your deductible (commonly $250, $500, or $1,000), and your insurance provider covers the rest up to your vehicle’s actual cash value.

What comprehensive claims cover:

What comprehensive does NOT cover:

One critical distinction: comprehensive and collision coverage are separate. When lenders require “full coverage” on financed cars, they’re typically mandating both. Collision handles crashes with the other driver or objects; comprehensive handles everything else.

The rate increase from a comprehensive claim depends on many factors: your insurer’s underwriting rules, your state’s regulations, the claim amount, and your overall driving history.

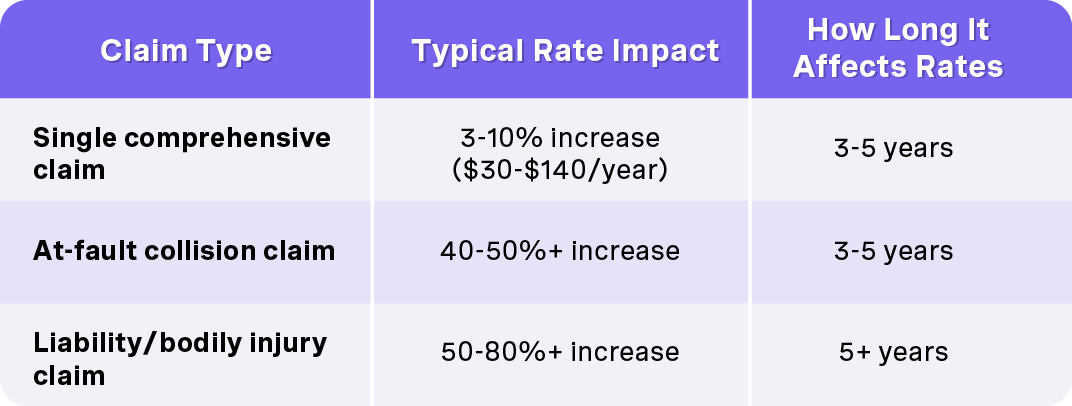

Let’s look at real numbers. In 2024, a single comprehensive claim typically adds about 3-10% to your car insurance premiums—that’s roughly $30 to $140 per year for most drivers. Compare that to an at fault claim from a collision, which can spike your premium by 40-50% or more.

Here’s a practical example: You hit a deer on a rural highway in January 2026. Repairs cost $2,500, and you have a $500 deductible. Your insurer pays $2,000. At your next renewal, you might see a premium increase of around $50-$80 per 6-month term.

Key numbers to remember:

Small vs. large claims matter:

The insurance costs difference between claim sizes is significant. Before filing a claim for minor damage, ask yourself if it’s worth the potential long-term cost.

Not all comprehensive claims are treated equally. Your insurer runs your claim through a complex algorithm that weighs multiple variables before deciding whether to adjust your rate.

Here’s what influences the outcome:

Here’s something many people don’t realize: even though comprehensive claims are technically “no-fault,” insurers can view multiple claims as evidence that you’re higher risk. Parking outside in storm-prone areas? That’s exposure. Repeated theft claims in the same neighborhood? That’s a pattern.

All insurance claims can affect your car insurance rates, but they’re definitely not created equal. Understanding the hierarchy helps you make smarter decisions about when filing a claim makes sense.

Comprehensive claims: The gentlest impact

Because comprehensive claims cover events outside your control—weather damage, theft, animal strikes—insurers typically apply smaller surcharges. You’re not being held accountable for causing the loss. A single comprehensive claim often results in 0-10% increase, and some insurers won’t raise rates at all for a first-time weather-related claim.

Collision claims: Moderate to severe impact

Collision coverage kicks in when you crash into another vehicle or object. If you’re at fault, expect significant pain. An at fault accident can raise full-coverage insurance premiums by 40-50% or more. Even not-at-fault collisions can sometimes affect rates, depending on your insurer and whether you live in a no fault state.

Liability and bodily injuries claims: The biggest hit

When your accident causes bodily injuries to others, you’re looking at the steepest and longest-lasting surcharges. A liability claim involving serious injuries can spike premiums by 50-80%, and the rate hike often lasts 5+ years.

Quick comparison:

The takeaway? While comprehensive claims aren’t “free,” they’re far less damaging than fault accident claims. However, stacking multiple comprehensive claims on top of a collision or liability loss can seriously change your risk profile and lead to higher rate increases across the board.

Safety and legal requirements always come first—but for minor losses, you have choices. The smart move is running the numbers before you pick up the phone.

The deductible comparison rule:

Generally, it’s not worth filing if the repair cost is at or only slightly above your deductible. If you have a $500 deductible and the damage costs $550 to fix, you’re filing a claim to receive $50—while potentially triggering a premium increase that costs you far more over 3-5 years.

When you should file:

When you might pay out of pocket:

Important considerations:

Pro tip: Before filing, contact your insurance agent and ask directly: “How will this claim affect my rate at renewal?” Many agents will give you a straight answer, helping you decide if it’s worth filing for your specific situation.

If you’ve decided that filing makes financial sense, here’s how to navigate the claims process efficiently and avoid delays.

Step 1: Document everything immediately

Take dated photos of all damage from multiple angles. Write down when and where the incident occurred. For theft or vandalism, file a police report right away—many insurers require this for coverage. Example: “Vandalism discovered March 3, 2026, at 7:15 a.m. in apartment complex parking lot.”

Step 2: Contact your insurer quickly

Call your insurance company’s claims line or use their app as soon as reasonably possible. Most carriers offer 24/7 claim reporting. Delays can complicate coverage, especially for theft claims where timing matters.

Step 3: Provide specific details

Be ready to share:

Step 4: Schedule an inspection

Your insurer will either send an adjuster or ask you to upload photos through their digital claims platform. Some auto insurance claims can now be processed entirely through an app with no in-person visit required.

Step 5: Get repair estimates

Obtain estimates from your insurer’s network repair shop or an independent shop, depending on your policy. Many carriers allow you to choose your repair facility, but using a network shop sometimes speeds up approval.

Step 6: Pay your deductible and receive payment

You’ll pay your comprehensive deductible to the repair shop. The insurer pays the remaining covered amount—either directly to the shop or to you if you prefer to handle repairs yourself.

You can’t undo a past claim, but you can take steps to reduce its long-term cost and prevent future increases.

Ask the right questions immediately:

Adjust your coverage strategically:

Reduce your risk profile:

Leverage technology and discounts:

Shop around aggressively:

Maintain a clean driving record:

Keep your record clear of traffic violations, speeding tickets, and at-fault crashes for several years after the claim. A clean driving record helps the surcharge disappear faster and signals to insurers that you’re a safer driver overall.

Drivers commonly ask similar questions about auto insurance claims and premiums. Here are straight answers to the most frequent concerns.

Does a single comprehensive claim always raise my rates?

Not necessarily. It depends on your insurance provider, claim size, and state regulations. Some carriers don’t surcharge for a first small comprehensive claim, especially for unavoidable events like weather damage. Always ask your insurer directly.

How long will a comprehensive claim stay on my record?

Typically 3-5 years, though this varies by state and insurer. Some companies stop rating the claim after 3 years; others track it for 5 or more. This claim affects your premiums for the entire time it’s on record.

Will a not-at-fault comprehensive claim affect my “accident-free” or “claim-free” discounts?

Unfortunately, yes—in many cases. Some insurers remove claim-free discounts after any claim, even if you weren’t at fault. This is one of the hidden costs of filing that many drivers don’t anticipate.

Are glass-only claims treated differently?

Often, yes. Many insurers treat windshield repairs as low-impact or non-surcharged, especially in states like Florida and Arizona that mandate zero-deductible glass coverage. However, full windshield replacements might be rated differently. Check with your insurance agent.

Can my insurance policy be non-renewed for too many comprehensive claims?

While less common than for at-fault accidents, it can happen. Multiple weather or theft claims (3+ in 3 years) might lead some carriers to non-renew your policy. They may view the pattern as higher risk regardless of fault.

Does comprehensive coverage make sense for my 10-year-old car?

Run the math. If your vehicle is worth under $3,000-$5,000, compare the annual cost of comprehensive (premium plus deductible risk) against the maximum payout you’d receive. Sometimes it’s more cost effective to self-insure and save money by dropping comprehensive on older vehicles.

Should I talk to experienced attorneys about my claim?

For straightforward comprehensive claims like hail or theft, you typically don’t need legal help. However, if your claim is denied unfairly or involves disputes, a free consultation with an attorney who handles insurance matters might be worthwhile.

The bottom line? A comprehensive claim can raise your insurance rates, but it’s usually a fraction of what you’d face after a fault accident or liability claim. Being strategic—knowing when to file, understanding your coverage limits, and shopping around if needed—puts you back in control.

Don’t let fear of a rate hike stop you from getting what you’re owed on a legitimate claim. Just run the numbers first, ask your agent the hard questions, and make the decision that actually protects your wallet long-term.

Compare & get covered fast

Find and compare auto insurance in minutes, and get your free credit score.

Choose when you pay

Select payment dates that line up with your payday.

Manage everything in one place

Track your policy, manage payments, and request a payment extension right from your dashboard.

.svg)