Most drivers overpay for car insurance by hundreds of dollars annually, missing out on discounts they’re already qualified for. Research shows that 85% of drivers qualify for at least one type of car insurance discount, yet many never claim these savings simply because they don’t know they exist.

Discount car insurance isn’t a separate type of coverage—it’s the same quality car insurance and comprehensive coverage you need, just at significantly reduced rates. The difference lies in understanding how insurance companies calculate premiums and which factors can trigger automatic savings on your auto policy.

Whether you’re shopping for affordable auto insurance for the first time or looking to reduce your current insurance costs, the right combination of discounts could save you anywhere from $200 to $800 annually. Many insurance companies offer more than 25 different discount types, and the savvy drivers who take advantage of multiple discounts often see the most dramatic reductions in their car insurance rates.

Finding affordable car insurance isn’t easy. Between high rates and large upfront payments, many drivers end up paying more, or delaying coverage altogether.

At OCHO, we’re changing that. Our goal has always been to make getting insured simple, affordable, and stress-free.

Why car insurance costs more than it should

Car insurance is supposed to protect you—not drain your bank account. But for a lot of people, especially those on low or fixed incomes, the system makes coverage far more expensive than it needs to be.

The problem starts before you even get on the road. Most insurers require huge down payments just to start a policy. That means the people who have the least money on hand are asked to pay the most upfront. On top of that, many carriers only offer the strongest pay-in-full discounts to customers who can afford to drop hundreds or even thousands of dollars in one go. If you can’t? You pay more—sometimes a lot more.

Then there’s the cycle no one talks about: cancelled insurance. When rates are inflated and the upfront cost is too high, people fall behind. Once a policy cancels, the next company often charges even bigger deposits because the customer is now considered “high risk.” It’s a trap, and it keeps people stuck paying more than drivers with higher incomes.

The result? Good drivers end up spending too much, losing coverage, and getting pushed into a financial corner—all because the system wasn’t built for people living paycheck to paycheck.

The solution: What OCHO does current and our new full-pay financing

OCHO now offers full-pay financing: a first-of-its-kind option that lets you get your pay-in-full discount, even if you don’t pay in full.

We pay the full cost of your insurance policy upfront, you get the carrier’s discount, and you pay us back over time, interest-free.

Our mission is to make the relationship with your money always humane, simple, safe and transparent so that you can manage it at your own pace.

This new program is currently available for select carriers in Arizona, Georgia, Texas and Washington, but we’re working to expand it soon.

Check your eligibility today and see how much you could save with OCHO.

Discount car insurance operates on a straightforward pricing formula that most drivers don’t fully understand: base rate plus surcharges minus discounts equals your final premium. Insurance companies start with a baseline car insurance rate for your demographic and vehicle type, then adjust this rate based on risk factors and qualifying discounts.

The average American driver pays approximately $1,500 annually for car insurance, but drivers who strategically apply for available discounts often reduce this amount by $200 to $800 per year. The key is understanding that discounts aren’t just marketing gimmicks—they’re risk assessment tools that insurance carriers use to reward behaviors and characteristics that statistically correlate with fewer claims.

Individual savings vary significantly based on your driving history, vehicle type, coverage needs, and geographic location. For example, a clean driving record discount might save you 15% with one insurer but 25% with another. Similarly, bundling your auto and home insurance policies could reduce your premiums by anywhere from 5% to 25%, depending on your insurance carrier.

The most successful discount strategies involve “stacking” multiple discounts together. While some insurance companies cap total discount amounts, others allow you to combine numerous qualifying discounts, creating compounding savings that can dramatically lower your annual insurance costs. Program availability and discount percentages may vary by state due to different regulatory requirements, so it’s essential to understand what’s available in your specific location.

Insurance companies organize their discount offerings into five primary categories, each targeting different aspects of your driver profile and risk assessment. Understanding these categories helps you identify which discounts you might already qualify for and which ones you could pursue with minimal effort.

The five main discount categories include safe driver and behavioral discounts, policy and coverage discounts, personal and professional affiliation discounts, vehicle-specific discounts, and loyalty-based discounts. Each category operates on different qualification criteria, and many drivers find they can access discounts from multiple categories simultaneously.

Average savings percentages vary considerably across insurers and states. Safe driver discounts typically offer the highest savings potential at 10-30% off base rates, while smaller discounts like paperless billing might only save 2-5%. However, these smaller discounts add up quickly when combined with larger savings opportunities.

The availability of specific discounts depends heavily on your state’s insurance regulations and the competitive landscape among local insurance companies. Some states mandate that insurers offer certain discounts, like defensive driving course reductions, while others leave discount offerings entirely to company discretion.

Clean driving record discounts represent one of the most valuable discount categories available to eligible drivers. Most insurance companies offer good driver discounts to customers who maintain accident-free and violation-free records for three to five years. These discounts can reduce your premium by 10-30%, making them among the most impactful savings opportunities available.

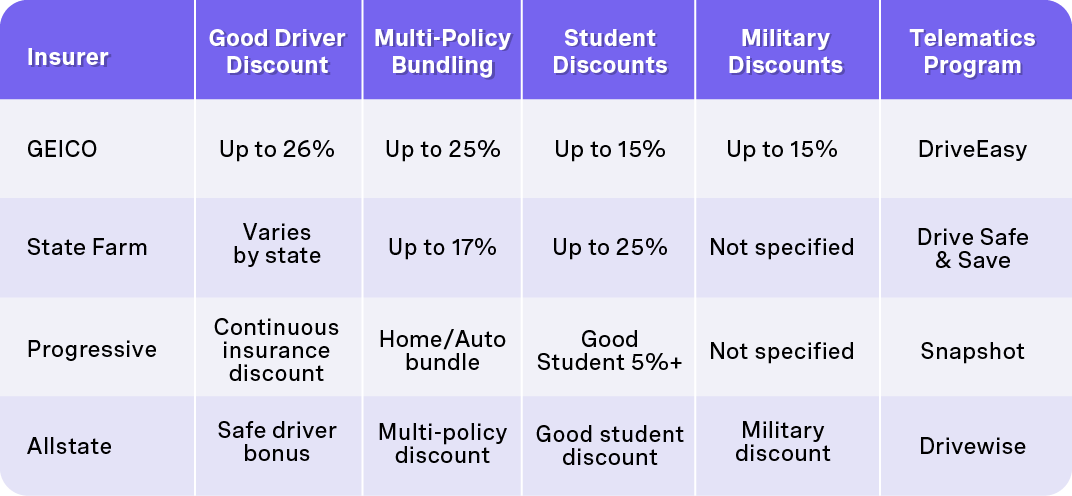

Telematics and usage-based insurance programs have revolutionized how insurance companies assess driving behavior. Programs like Progressive’s Snapshot monitor your actual driving habits through smartphone apps or plug-in devices, measuring factors like speed, braking patterns, time of day you drive, and total miles traveled. Participants in these programs save an average of $322 annually, with some careful drivers seeing much larger reductions.

Low mileage discounts specifically benefit drivers who travel fewer than 7,500 miles annually. Many insurance companies recognize that reduced road time correlates with lower accident risk, offering discounts ranging from 5-15% for qualifying low-mileage drivers. If you work from home, live in a walkable city, or simply don’t drive much, this discount could provide significant savings.

Defensive driving course discounts reward drivers who complete approved safety training programs. Some states actually require insurance companies to offer these discounts, recognizing the public safety benefits of additional driver education. Even if you have a clean driving record, completing a defensive driving course can often trigger additional savings while improving your road safety skills.

Several factors influence your eligibility for behavioral discounts beyond just avoiding accidents. Traffic violations like speeding tickets, running red lights, or reckless driving can disqualify you from good driver discounts for several years. However, the investment in safe driving pays off significantly—drivers with clean records often qualify for the deepest discount tiers offered by their insurance carrier.

Multi-policy bundling creates some of the most substantial savings opportunities for property owners who need both auto and home insurance coverage. When you purchase multiple policies from the same insurance company, you could save 5-25% on both your car insurance policy and homeowners coverage. This discount recognizes that managing multiple policies creates operational efficiencies for insurers and increases customer lifetime value.

The multi car discount applies to households that insure more than one car under a single policy. Families with multiple vehicles often see 10-25% savings compared to maintaining separate policies for each vehicle. This discount makes particular financial sense for families with teen drivers, where adding a young driver to an existing policy often costs less than purchasing separate coverage.

Payment method discounts reward customers who choose cost-effective billing and payment options. Paying your annual premium upfront instead of monthly installments can save you 5-10% by eliminating processing fees and administrative costs. Similarly, automatic payments and paperless billing each typically provide 2-5% discounts that add up over time.

Comprehensive and collision coverage decisions also impact your discount eligibility. Higher deductibles generally reduce your premium costs, though this strategy only makes sense if you have sufficient savings to cover the deductible amount in case of an accident. Some insurers offer “deductible rewards” programs that reduce your collision or comprehensive coverage deductibles by $50 annually for each claim-free year.

Long-term customer loyalty discounts recognize the value of policy continuity. Customers who maintain coverage with the same insurer for multiple years often qualify for increasing discount percentages. However, it’s important to balance loyalty discounts against potentially better rates available from competitors—sometimes switching insurers provides greater savings than staying for loyalty benefits.

Military personnel and veterans often have access to specialized discount programs that recognize their service while acknowledging the disciplinary and safety training associated with military experience. Companies like USAA exclusively serve military families, while mainstream insurers like GEICO offer substantial military discounts. Federal employees may also qualify for group discount programs through their government employment.

Professional organization memberships frequently unlock insurance discounts that many members don’t know exist. AAA membership often provides car insurance discounts with multiple insurers, while AARP members over 50 can access senior-specific rates and discount programs. Alumni associations, professional societies, and trade organizations sometimes negotiate group rates with insurance companies that provide meaningful savings to their members.

Student discounts come in several varieties, each designed for different educational situations. The good student discount applies to full-time high school and college students who maintain at least a 3.0 GPA or B average, often providing 5-15% savings. Away student discounts can dramatically reduce costs for college students who attend school more than 100 miles from home and don’t regularly drive the family vehicle.

Occupation-based discounts recognize that certain professions correlate with lower insurance claims. Teachers, healthcare workers, first responders, and engineers often qualify for profession-specific discounts based on actuarial data showing these groups have fewer claims. Some companies also offer discounts for customers with higher education degrees, regardless of their specific occupation.

Teen driver discounts help offset the significant cost increase that comes with adding young drivers to a family policy. While teen drivers typically increase premiums substantially due to their limited driving experience and higher accident rates, some insurers offer discounts after young drivers complete their first year of coverage without serious accidents or violations. Taking advantage of good student discounts and defensive driving courses can further reduce these costs.

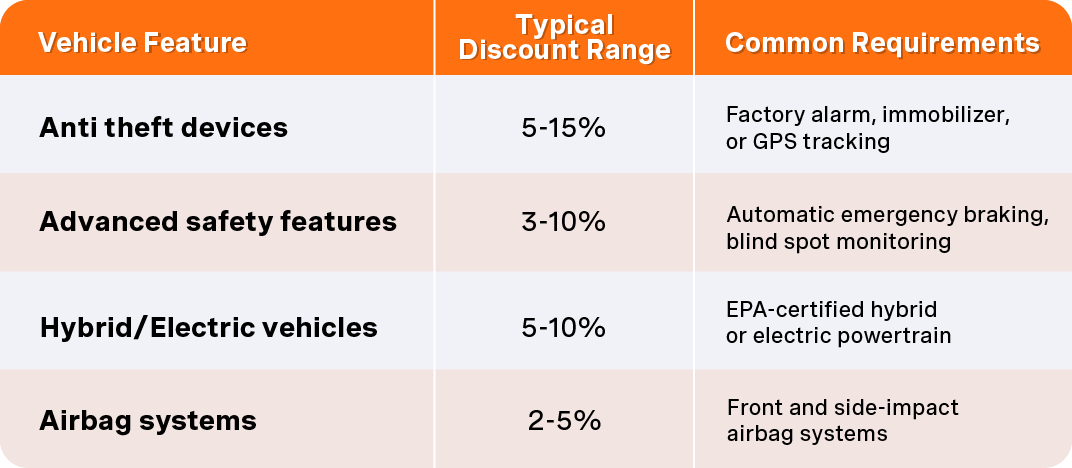

Your vehicle choice significantly impacts both your baseline insurance rates and discount eligibility. Safety features, security systems, and environmental considerations all factor into discount calculations, making vehicle selection an important component of long-term insurance cost management.

Insurance companies calculate vehicle-related discounts based on statistical data showing how specific features correlate with reduced claim frequencies and severities. Vehicles with comprehensive safety features simply cost less to insure because they’re involved in fewer accidents and sustain less damage when accidents do occur.

Anti theft devices provide some of the most straightforward vehicle-based discounts available. Factory-installed alarm systems, engine immobilizers, and GPS tracking systems all qualify for anti theft device discounts with most insurance companies. These features reduce theft risk, which translates directly into lower comprehensive coverage costs.

Advanced safety features represent a growing discount category as vehicle technology continues improving. Automatic emergency braking, blind spot monitoring, lane departure warning systems, and adaptive cruise control all contribute to accident prevention. Insurance companies increasingly recognize these technologies’ safety benefits and offer discounts accordingly.

Airbag and anti-lock brake system discounts acknowledge that these safety features reduce injury severity in accidents, leading to lower medical expenses and property damage claims. Most modern vehicles include these features as standard equipment, making these discounts widely available to drivers with newer cars.

Backup cameras and parking assist technology help prevent low-speed accidents in parking lots and residential areas. While these accidents might seem minor, they represent a significant portion of insurance claims. Vehicles equipped with these systems often qualify for modest discounts that reflect their reduced accident involvement.

Hybrid and electric vehicles often qualify for specialized discount programs that combine environmental incentives with actuarial risk assessment. Insurance companies have found that hybrid and electric vehicle owners tend to be more cautious drivers who maintain their vehicles better and drive fewer miles annually.

Electric vehicles present unique insurance considerations beyond just environmental benefits. Many electric vehicle owners install home charging stations, tend to have higher incomes, and often maintain other environmentally conscious behaviors that correlate with lower insurance claims. Some insurers offer EV-specific policies that provide additional coverages for charging equipment and battery replacement.

Alternative fuel vehicles running on compressed natural gas, ethanol, or biodiesel may also qualify for green vehicle discounts. However, these discounts vary significantly by geographic region and fuel availability, as alternative fuel infrastructure affects vehicle practicality and usage patterns.

The top vehicles qualifying for eco-friendly discounts in 2024 include popular hybrid models like the Toyota Prius, Honda Accord Hybrid, and Ford Fusion Hybrid, along with electric vehicles like the Tesla Model 3, Nissan Leaf, and Chevrolet Bolt. Many insurance companies update their qualifying vehicle lists annually as new models enter the market.

Discovering all available discounts requires systematic research and honest assessment of your current situation. Most drivers qualify for multiple discounts they’re not currently receiving, simply because they haven’t asked about them or updated their insurance agent about qualifying changes in their circumstances.

Start by requesting a comprehensive discount review from your current insurance carrier. Insurance agents have access to complete discount listings and can identify opportunities you might not discover through online research alone. Many companies offer unadvertised discounts or regional promotions that only become available when you specifically inquire about them.

Document your qualifying factors systematically: your driving record, vehicle features, professional affiliations, educational background, and household composition. This information helps you present a complete picture to potential insurers and ensures you don’t miss applicable discounts during the quote comparison process.

Schedule annual insurance reviews to maintain optimal discount positioning. Life changes like marriage, home purchases, job changes, or vehicle upgrades often create new discount opportunities. Similarly, maintaining clean driving records for additional years can unlock higher discount tiers with many insurance companies.

Different insurance companies excel in different discount categories, making comparison shopping essential for maximizing your savings potential. Some insurers offer deeper discounts for specific demographics, while others provide more generous bundling opportunities or superior telematics programs.

Regional availability affects discount programs significantly. Insurance companies operating in multiple states often adjust their discount offerings based on local competition, regulatory requirements, and regional risk factors. What’s available in California might differ substantially from discount programs in Texas or New York.

Discount stacking policies vary considerably among insurers. Some companies cap total discounts at specific percentages, while others allow unlimited discount combinations. Understanding these policies helps you choose insurers where your particular discount combination provides maximum value.

Customer service quality becomes particularly important when managing multiple discounts. Companies with better customer service make it easier to maintain discount eligibility, update qualifying information, and add new discounts as your situation changes over time.

Many drivers focus exclusively on finding the cheapest base car insurance rate without considering how discounts affect their total annual costs. A company with higher base rates but generous discount programs often provides better value than insurers with low advertised rates but limited discount opportunities.

Failing to notify your insurance company about discount-qualifying life changes represents a costly oversight that many drivers make. Getting married, moving to a safer neighborhood, installing security systems, or completing defensive driving courses all create new discount opportunities that only apply if you inform your insurer.

Coverage quality should never be sacrificed solely to achieve lower premiums through discounts. Cheap auto insurance that doesn’t provide adequate protection can cost thousands more than quality coverage if you’re involved in serious accidents. Always ensure your policy meets your state’s minimum requirements and provides sufficient protection for your financial situation.

Discount percentages can be misleading if they apply only to specific coverage components rather than your total premium. A 20% discount on comprehensive coverage provides much less savings than a 20% discount on your entire policy. Always compare total costs rather than focusing solely on discount percentages.

Missing renewal deadlines can reset discount accumulation periods and eliminate hard-earned loyalty benefits. Many discount programs require continuous coverage to maintain eligibility, making timely renewals essential for preserving your savings. Set calendar reminders well before your policy expiration date.

Some drivers assume that discount car insurance automatically means lower-quality coverage or reduced customer service. This misconception prevents them from pursuing legitimate savings opportunities. Discounts are risk assessment tools, not indicators of coverage quality—the same comprehensive and collision coverage costs less when you qualify for applicable discounts.

Can you combine multiple discounts with most insurance companies?

Most insurance companies allow discount stacking, where multiple qualifying discounts apply simultaneously to reduce your premium. However, some insurers cap total discounts at specific percentages, while others limit certain discount combinations. When shopping for affordable car insurance, ask specifically about discount stacking policies to understand maximum savings potential.

Do discount car insurance policies provide the same coverage as regular policies?

Yes, discount car insurance provides identical coverage to standard policies. Discounts reduce your premium cost but don’t change your coverage levels, deductibles, or policy terms. Whether you pay full price or receive substantial discounts, your comprehensive coverage, collision coverage, liability protection, and other coverages remain exactly the same.

How often should you shop for new discounts and compare rates?

Insurance experts recommend comparing car insurance quotes annually, even if you’re satisfied with your current coverage. Insurance rates and discount offerings change frequently, and new companies entering your market might provide better discount combinations for your specific situation. Additionally, your discount eligibility often improves over time as you accumulate claims-free years and experience life changes.

What happens to your discounts if you file a claim?

Most discounts remain unaffected by single claims, though this depends on your specific insurance policy and discount types. Good driver discounts typically require claims-free periods of 3-5 years, so filing a claim might reset this timeline. However, discounts based on vehicle features, policy bundling, or professional affiliations generally continue regardless of claims activity.

Are there income-based discount programs for low-income drivers?

Some states and insurance companies offer income-based discount programs for qualifying low-income drivers. These programs recognize that affordable auto insurance access is essential for employment and economic stability. Additionally, some insurers provide payment plan options that make insurance costs more manageable without compromising coverage quality. Check with your state insurance department about available assistance programs in your area.

Many drivers overlook the fact that maintaining continuous insurance coverage is often more important than finding the absolute lowest rates. A brief coverage lapse can eliminate years of discount accumulation and place you in high-risk categories that significantly increase future premiums. The goal should be finding sustainable, affordable coverage that you can maintain consistently over time.

The key to maximizing your discount car insurance savings lies in understanding that insurance shopping is an ongoing process, not a one-time activity. As your life circumstances change and you accumulate more years of safe driving, new discount opportunities become available. Taking advantage of these opportunities while maintaining appropriate coverage levels ensures you get the best value from your auto insurance investment.

Start reviewing your current policy today to identify missed discount opportunities, compare quotes from multiple insurers, and take steps to qualify for additional savings programs. With the right combination of discounts and strategic planning, you could save hundreds of dollars annually while maintaining the quality coverage you need to protect yourself and your vehicle.

Where is OCHO available?

OCHO is currently available in Arizona, Illinois, Texas, New Mexico, Missouri, Georgia, Washington, Wisconsin. We’re expanding quickly, so if we’re not in your area yet, we’re likely on the way. You can always check availability by starting an application—if we’re active in your state, you’ll be able to continue your quote instantly.

How is this different from traditional premium financing?

Traditional premium financing usually means interest, fees, and a long approval process. OCHO is different. We give you a simple, flexible way to cover your insurance down payment with no interest, no hidden fees, and no credit check. You get the coverage you need today and pay us back over time in smaller, manageable installments.

Is it really interest-free?

Yes—100% interest-free. What you borrow to cover your down payment is exactly what you pay back. No surprises, no rate hikes, no compounding interest sneaking up on you later. We do have a broker fee, but that’s shown transparently as part of the payment process.

Will my insurance company know I’m paying with OCHO?

Yes, but only in the way that matters. Your insurance company receives the payment from OCHO just like they would from you directly. It doesn’t change your coverage, your premium, or your relationship with the carrier. To them, it’s simply a payment—just one that makes your life easier.

Compare & get covered fast

Find and compare auto insurance in minutes, and get your free credit score.

Choose when you pay

Select payment dates that line up with your payday.

Manage everything in one place

Track your policy, manage payments, and request a payment extension right from your dashboard.

.svg)