Key Takeaways

Let’s be honest: if you’re searching for cheap sr22 insurance, you’ve probably had a rough go of it lately. Maybe a DUI conviction, maybe you got caught driving without coverage, or perhaps too many traffic offenses stacked up. Whatever landed you here, you’re now facing higher rates and a bureaucratic process that feels designed to confuse you.

Here’s the thing, the SR 22 filing requirement doesn’t have to drain your bank account. Yes, your insurance company will likely charge you more because of your driving history. But “more expensive” doesn’t have to mean “unaffordable.” With the right approach, you can satisfy your state’s requirements, get back on the road legally, and keep your monthly payments from spiraling out of control.

This guide breaks down everything you need to know about finding affordable SR 22 insurance, from understanding what the filing actually is to specific strategies that can save you hundreds of dollars per year.

Let’s clear up the biggest misconception right away: SR 22 insurance isn’t actually a type of insurance policy. It’s a certificate of financial responsibility that your insurer files with the state’s department of motor vehicles to prove you carry the minimum amount of liability coverage required by law.

Think of it this way, you must first buy a standard auto insurance policy that meets your state’s minimum requirements for liability insurance. The SR 22 form is simply an added filing that proves to the department of motor vehicles dmv that you have that coverage in place. Your insurance provider handles the paperwork and will notify the local dmv if your policy lapses or gets canceled.

You might hear different terms tossed around: “SR-22 filing,” “SR-22 bond,” or “certificate of financial responsibility.” They all mean the same thing. It’s a monitoring mechanism that keeps the state informed about your coverage status.

Here’s where it gets tricky: requirements vary significantly by state. Not every motorist in every state even uses the SR 22 system. And if you’re in Florida or Virginia and got convicted of a DUI, you’ll likely need an FR 44 instead. The FR 44 demands higher liability limits, often around 100/300/50 compared to standard minimums like 25/50/25, which means your car insurance policy will cost more to meet those thresholds.

Consider two drivers with similar violations:

Driver A in Ohio gets a DUI and needs to file an SR 22 with standard state minimum liability coverage. Their insurance agent files the form, and they’re set for three years.

Driver B in Florida faces the same situation but must obtain an FR 44 with significantly higher liability limits. Their auto insurance company charges more because the coverage itself costs more, not just because of the filing.

Same violation, different states, different rules. Before you start shopping, check what your state requires.

You only need an SR22 if you’re ordered by a court or your state’s DMV to file one, typically after serious or repeated driving violations. If nobody has told you that you need an SR22, you probably don’t.

The most common triggers for SR22 requirements include:

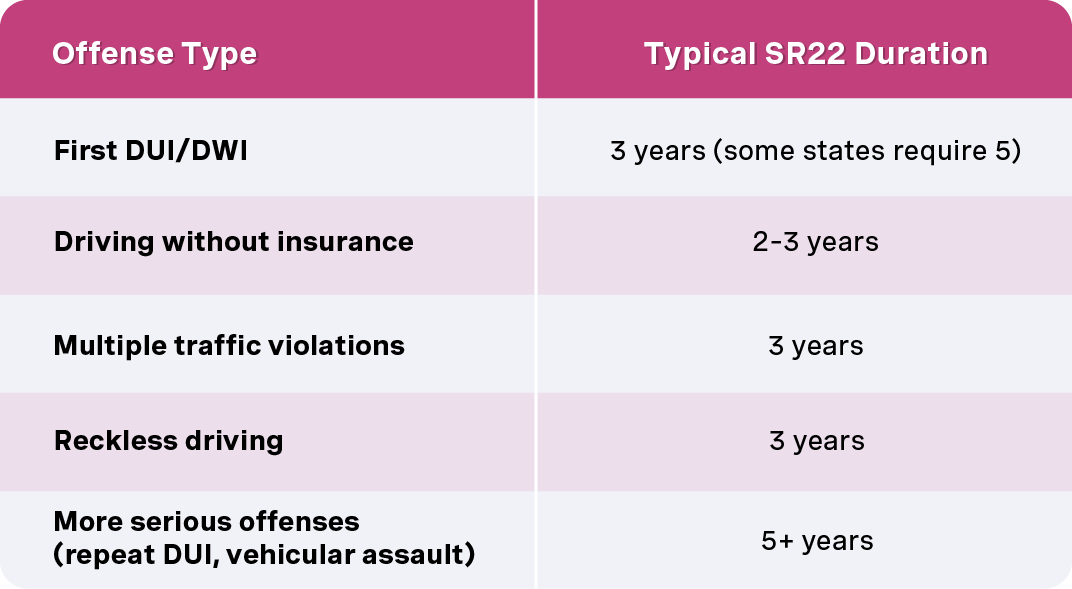

The duration depends on your state law and the severity of the driving offense. Here’s what typical timelines look like:

A first-offense DUI in California, for example, triggers a 3-year SR 22 filing requirement. In Texas, a no-insurance conviction typically means 2 years of mandatory SR22 insurance. The exact timeframe should be spelled out in your court paperwork or the notice from your state’s department of motor vehicles.

Here’s the critical part: the SR 22 must stay active the entire mandated period. If your car insurance policy lapses, even for a single day, your insurer must notify the state immediately by filing an SR-26 cancellation notice. That can trigger automatic license suspension and potentially restart your filing period from scratch.

One more thing to understand: the underlying violation usually stays on your driving record longer than the SR22 requirement itself. A DUI might require SR 22 for 3 years, but that DUI conviction could remain visible on your record for 7–10 years. This means your rates won’t instantly drop to “normal” when the filing period ends.

The SR 22 filing fee itself is usually minor, often a one time fee of $15 to $50 that your insurance company charges to process the paperwork. That’s not what makes sr 22 insurance expensive.

What actually drives up your costs is your classification as a high-risk driver. Insurance premiums are based on risk, and if you’ve been convicted of a DUI, caught driving without coverage, or racked up multiple traffic offenses, insurers see you as significantly more likely to file a claim than the average driver.

The numbers can be jarring. A driver paying $120 per month before a DUI might see rates jump to $250–$400 per month afterward. That’s a 100%–300% increase, and it’s entirely because of the violation—not the SR 22 paperwork itself.

Several factors influence exactly how much more you’ll pay:

The good news? These factors aren’t set in stone. Shopping strategically and making smart choices can significantly reduce what you pay.

Even after a serious violation, you can reduce your SR22 insurance costs. It takes some effort, but the savings are real. Here’s how to approach it methodically.

Step 1: Confirm your state requirements

Before you do anything else, check your DMV notice or court paperwork carefully. You need to know the exact filing period (e.g., 3 years from your reinstatement date) and the minimum liability coverage limits required. Some drivers assume they need more coverage than the state actually requires, or less, which creates legal problems. Get the facts straight first.

Step 2: Decide between owner and non-owner coverage

If you don’t own a car and don’t have regular daily access to one, a non-owner SR 22 policy can often fulfill your requirement at a lower cost than insuring a specific vehicle. We’ll cover this more in the next section, but it’s worth considering before you start getting quotes.

Step 3: Shop multiple high-risk carriers

This is where most people leave money on the table. Get quotes from at least 4–5 insurers that explicitly handle SR 22 filings. Include national companies like Progressive, GEICO, and State Farm, but also look at regional specialists and companies like The General that focus on high risk drivers.

Compare both 6-month and 12-month policy options. Sometimes one term is significantly cheaper than the other with a particular car insurance company.

Step 4: Tailor your coverage appropriately

Choose liability limits that meet or moderately exceed your state minimum, but don’t over-insure if your budget is tight. If you’re driving an older, paid-off vehicle, consider dropping collision and comprehensive coverage. The math often doesn’t make sense to carry full coverage on a car worth less than a few thousand dollars.

Avoid unnecessary add-ons like roadside assistance or rental car coverage if you’re trying to minimize costs.

Step 5: Adjust your deductibles

If you do keep collision and comprehensive coverage, raising your deductible from $500 to $1,000 can meaningfully lower your monthly premium. Just understand the tradeoff: you’ll pay more out of pocket if you’re in an accident.

Step 6: Ask specifically about discounts

Many insurers offer discounts that apply even to high-risk policies, but they don’t always advertise them. Ask your insurance agent about:

A free auto insurance quote doesn’t obligate you to anything. Get multiple quotes, compare them side by side, and don’t settle for the first price you’re offered.

At OCHO, we offer SR22 insurance in selected states, just check in our app to see if the state you need is available. With us, you can get a low downpayment, and easy installments every 2 weeks. This means you can easily stay on top of your payments and not get into any lapses.

Many people need cheap sr22 insurance even when they don’t own a car, or when one state requires the filing but they’ve moved to another. These situations are common and navigable, you just need to understand your options.

Non-Owner SR 22 Policies

A non-owner auto insurance policy provides liability coverage when you occasionally drive cars you don’t own. It typically excludes vehicles regularly available to you (like a spouse’s car garaged at your address), but covers situations like renting a car or driving a borrowed car occasionally.

Non-owner policies are usually cheaper than standard car insurance because insurers assume you’re driving less frequently. If you don’t have your own vehicle registered in your name, this can be an affordable way to prove financial responsibility and satisfy your SR22 requirement.

Non-owner SR 22 works well for:

Be honest with your insurance provider about your situation. If you have regular access to a household vehicle, a non-owner policy probably won’t cover you properly and could create problems if you need to file a claim.

Out-of-State SR 22 Filings

If you moved from Illinois to Colorado but Illinois still demands an SR 22, you need an insurer licensed in Colorado that can file an SR 22 form with Illinois while your actual policy follows Colorado’s rules.

This can get complicated. Not every insurer handles out-of-state filings, and you may need to work with a specialized insurance agent or high-risk carrier to find coverage that satisfies both states’ requirements.

Failure to maintain an out-of-state SR 22 can lead to license suspension in the original state, and that suspension can sometimes create problems when you try to renew or transfer your driver’s license where you currently live. Don’t let this slip through the cracks.

Time, clean driving, and consistent payment history are the biggest long-term cost savers for drivers with SR 22 requirements. The habits you build during your filing period directly affect what you’ll pay—both now and after the requirement ends.

Avoid any new violations

This seems obvious, but it’s worth emphasizing. Even a minor speeding ticket during your SR 22 period can prevent your insurance premiums from decreasing when the filing ends. Courts and insurers are watching to see if you’ve changed your behavior. Multiple traffic violations or another at fault accident will only dig the hole deeper.

Pay on time, every time

Set up automatic payments if possible. A coverage lapse, even for a few days, triggers an SR-26 notice to your state’s department of motor vehicles, which can lead to immediate license suspension and potentially restart your filing period. Some states are stricter about this than others, but it’s not worth the risk anywhere.

Complete a defensive driving course

Many states offer point reduction or other benefits for completing state-approved defensive driving or DUI education courses. Some insurers also offer small discounts for course completion. Check what’s available in your state and take advantage of it.

Re-shop your coverage annually

The high-risk insurance market is competitive, and rates change. Get new quotes every 12 months, or shortly before your SR 22 requirement ends. Some carriers become significantly more competitive once you’ve gone several years without a new violation. An insurance agent who specializes in high-risk policies can help you navigate this.

Improve other risk factors

While you can’t change your driving history overnight, you can improve other factors that affect your rates:

The SR 22 requirement feels like a punishment, but it’s also a countdown. Every month you maintain continuous coverage and drive legally without new incidents, you’re one step closer to lower rates and eventually having the filing no longer required.

Can I cancel my SR-22 policy early if I sell my car or stop driving?

Selling your car doesn’t automatically remove your SR 22 requirement. The court or DMV date controls when you’re no longer required to maintain the filing, not your vehicle ownership status. If you sell your car, you might switch to a cheaper non-owner SR 22 policy instead, but canceling your insurance entirely before the mandated end date will trigger an SR-26 notice and can re-suspend your driving privileges. You need to maintain continuous coverage for the full required period, regardless of whether you own a vehicle.

Will every insurance company see my SR-22 history if I switch providers?

The SR 22 form itself doesn’t transfer between insurers, but that doesn’t help much. Every car insurance company pulls your motor vehicle report when you apply for coverage, and that report shows your underlying violations, conviction dates, and any driver’s license suspension history. They’ll price your policy based on those factors whether or not they know about your previous SR 22 filing specifically. There’s no way to hide a DUI or other penalties from a new insurer.

Is it cheaper to pay SR-22 insurance monthly or in full?

Many insurers offer a pay-in-full discount when you pay for your entire 6-month or 12-month term upfront, typically saving 5–10% compared to monthly installments. Monthly billing often includes additional fees that add up over time. If you can swing the lump sum payment, it’s usually the cheaper route. That said, if paying in full would strain your finances and risk a lapse later, monthly payments with automatic billing might be the safer choice for maintaining continuous coverage.

Does filing an SR-22 affect my ability to get car loans or leases?

Lenders primarily focus on your credit score, income, and debt-to-income ratio—not your SR 22 status specifically. However, the higher insurance premiums you’ll pay can affect the total cost of vehicle ownership, which some lenders factor into affordability assessments. If a lender requires full coverage (collision and comprehensive) on a financed vehicle, your SR 22 status will make that coverage more expensive, which could impact how much car you can afford.

What happens after my SR-22 period ends—do my rates go back to normal right away?

When your SR 22 requirement ends and your insurer removes the filing, your rates may drop somewhat. But “normal” pricing typically only returns once the major violation ages off your driving record entirely. For a DUI, that might take 5–10 years depending on state law. You’ll likely see gradual improvements each year the violation gets older, but don’t expect your rates to snap back to pre-violation levels the moment your SR 22 period concludes. The underlying offense still matters to insurers even after the filing is no longer required.

The SR 22 requirement won’t last forever, but how you handle it determines what you pay—both now and for years afterward. Start by confirming your state requires, get quotes from multiple insurers, and make the small choices that keep costs manageable. With patience and clean driving, you’ll work your way back to standard rates. Get those quotes today and take control of your situation.

Compare & get covered fast

Find and compare auto insurance in minutes, and get your free credit score.

Choose when you pay

Select payment dates that line up with your payday.

Manage everything in one place

Track your policy, manage payments, and request a payment extension right from your dashboard.

.svg)