Cheap full coverage insurance refers to comprehensive auto insurance coverage that protects your vehicle and finances without the premium price tag. Unlike basic liability coverage required by most states, full coverage car insurance includes multiple types of protection that go far beyond minimum requirements to legally operate a vehicle.

When we talk about cheap car insurance, it doesn’t mean inadequate protection. Instead, it means finding affordable coverage that provides robust financial protection through strategic shopping and smart coverage choices. Full coverage typically costs significantly more than liability-only policies, but the additional protection can save you thousands in the event of a covered accident, theft, or natural disaster.

“Full coverage” sounds like it protects you from everything, but it actually doesn’t. It isn’t an official type of insurance—it's just a casual way people describe having both liability coverage and physical damage coverage (comprehensive + collision).

The term is misleading because:

A better approach is to look at the exact coverages included, not just the label. Make sure you always read the small print!

The key difference between cheap full coverage and state minimum policies lies in vehicle protection. While liability coverage only pays for damage you cause to others, full coverage also protects your own car and provides additional safety nets when other drivers lack adequate insurance. This comprehensive protection becomes essential when you consider that the average cost of a new car has reached $47,000, making vehicle replacement a significant financial burden.

Understanding that car insurance depends on numerous factors helps you appreciate why shopping for cheap full coverage requires a strategic approach. Your car insurance rate reflects your driving habits, location, vehicle type, and coverage choices, meaning there’s no one-size-fits-all solution for finding affordable coverage.

We have worked out a number of ways to make full coverage insurance affordable to everyone.

This means you get the protection of full coverage at the lowest possible price, without draining your bank account. No interest, no hidden fees, no credit checks—just flexible payments, lower rates, and the ability to stay insured without financial stress.

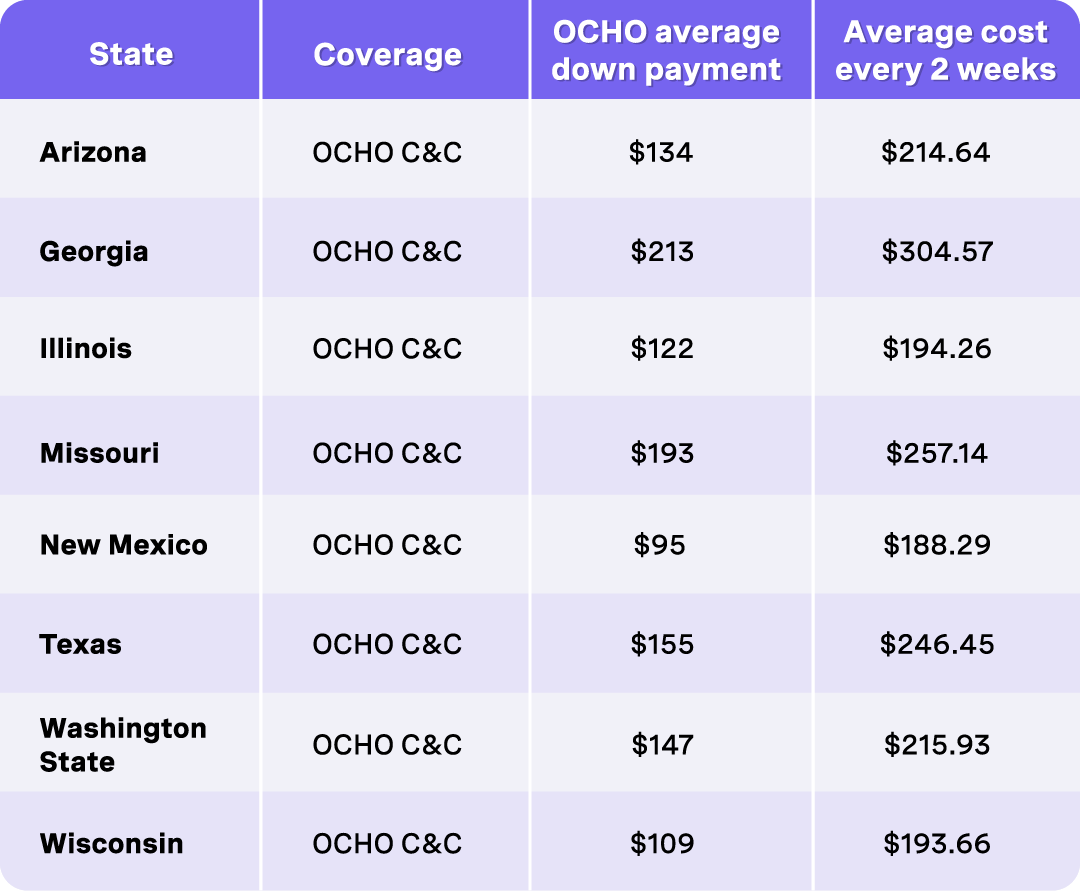

Our flexible payment plans are designed to turn full coverage—often too expensive upfront—into a realistic, affordable option. Check the table below to see exactly how OCHO lowers your upfront cost, unlocks discounts, and makes plans that are normally out of reach fit your budget:

Full coverage car insurance combines several distinct auto insurance coverages to create comprehensive protection. Understanding each component helps you make informed decisions about coverage options and identify areas where you might save money without compromising essential protection.

Liability Coverage forms the foundation of any auto insurance policy and remains mandatory in most states. This coverage includes bodily injury liability, which pays medical expenses and lost wages when you’re responsible for injuries to others, and property damage liability, which covers repairs to other vehicles and property you damage in an accident caused by you.

Collision Coverage protects your vehicle when it’s damaged in accidents with other cars, objects, or single-car incidents like rollovers. This coverage pays for vehicle repairs regardless of who caused the accident, making it particularly valuable for newer or more expensive vehicles. Your insurance company will pay up to your car’s actual cash value, minus your chosen deductible.

Comprehensive Coverage protects against non-collision incidents that could damage or destroy your vehicle. This includes theft, vandalism, fire, flood, hail damage, falling objects, and animal strikes. Like collision coverage, comprehensive pays up to your vehicle’s actual cash value minus your deductible, providing essential protection against unpredictable risks.

Uninsured/Underinsured Motorist Coverage protects you when other drivers lack adequate insurance coverage. This protection pays for medical bills, lost wages, and vehicle damage when an at-fault driver has no insurance or insufficient coverage limits to pay for your losses. Given that many drivers carry only minimum coverage, this protection can prevent significant out-of-pocket expenses.

Optional auto insurance coverages can enhance your protection but also increase costs. Medical payments coverage handles immediate medical expenses for you and your passengers regardless of fault, while personal injury protection provides broader medical and wage loss benefits. Gap insurance covers the difference between what you owe on a financed vehicle and its current value if it’s totaled, and rental reimbursement pays for rental cars while your vehicle undergoes repairs.

Finding cheap full coverage insurance shouldn’t feel like a second job. But the truth is, every insurance company prices coverage differently, so the only real way to save is by comparing a lot of quotes—accurately and side-by-side.

Most people don’t have the time (or patience) to gather five different quotes from national carriers, regional companies, and online-only insurers. And even if you do, making sense of different deductibles, limits, and fees can get confusing fast.

That’s where OCHO comes in.

We’re not just another place to get a quote—we’re your comparison tool. OCHO pulls options from multiple insurers, makes sure the coverage levels match, and shows you the real numbers clearly so you can spot the best deal.

Plus, we add something most comparison sites don’t:

PriceCheck AI.

It scans final rates—not just the teaser quotes—to make sure you’re actually getting the lowest price available to you. No guesswork. No surprises. Just the cheapest full coverage option that fits your budget.

Behind the scenes, OCHO works like the best independent agent you could ask for—shopping multiple carriers, explaining differences in coverage, and helping you balance affordability with real protection. Whether the best value comes from a big-name insurer, a regional carrier, or a tech-forward online company, we’ll show you.

With OCHO and PriceCheck AI, getting cheap full coverage finally becomes simple, transparent, and stress-free.

When you compare car insurance quotes, ensure you’re evaluating identical coverage limits and deductibles across all insurers. Small differences in coverage can significantly impact pricing, making it difficult to identify genuine savings opportunities. Request quotes with various deductible levels to see how adjusting these amounts affects your premiums.

Consider both traditional insurance companies and newer, technology-focused insurers that may offer lower rates through reduced overhead costs. Many drivers find that online-focused companies provide excellent value for cheap car insurance while maintaining great customer service through digital platforms and phone support.

Remember to compare more than just price when evaluating options. Research each company’s financial strength, customer satisfaction ratings, and claims handling reputation. The cheapest auto insurance quote means nothing if the company can’t pay claims promptly or provides poor customer service when you need assistance most.

Securing cheap full coverage insurance often depends more on available discounts than on choosing bare-minimum coverage. Most insurance companies offer numerous car insurance discounts that can substantially reduce your premiums when combined effectively.

Multi-policy discounts provide some of the most significant savings opportunities. By bundling your auto insurance with home insurance, renters insurance, or other policies from the same company, you can typically save 10-20% on your home and auto insurance premiums. This strategy not only reduces costs but also simplifies policy management and billing.

Safe driving discounts reward drivers who maintain clean records and demonstrate responsible driving habits. Many insurers offer discounts for accident-free periods, while others provide usage-based insurance programs that monitor your driving habits through smartphone apps or plug-in devices. These programs can reduce premiums by up to 30% for drivers who demonstrate safe driving patterns, low mileage, and responsible vehicle use.

Multi-vehicle discounts apply when you insure more cars with the same company. Families with multiple vehicles often save significantly by consolidating all auto policies with one insurer rather than shopping separately for each car. The savings typically increase with each additional vehicle added to the policy.

Vehicle-related discounts can also reduce your car insurance coverage costs. Cars equipped with modern safety features like automatic emergency braking, blind-spot monitoring, and anti-theft systems often qualify for lower rates. Additionally, some insurers offer discounts for low-mileage drivers or those who park in garages rather than on streets.

Payment and administrative discounts provide easy savings for policy management choices. Many companies offer discounts for automatic payment setup, paperless billing, paying your full policy online rather than in installments, and maintaining continuous coverage without lapses. These small discounts can add up to meaningful annual savings.

Students can access education-related discounts through good student programs that reward high academic achievement. Professional associations, military service, and employer partnerships may also provide group discounts worth investigating when shopping for affordable coverage.

Strategic adjustments to your coverage limits and deductibles can significantly reduce your car insurance policy costs while maintaining appropriate protection. Understanding how these changes affect both your premiums and potential out-of-pocket expenses helps you make informed decisions about coverage optimization.

Higher deductibles represent the most direct way to lower your insurance rate. Increasing your collision and comprehensive deductibles from $500 to $1,000 or $1,500 can reduce your premiums by 15-30%, depending on your insurer and vehicle. However, ensure you can comfortably afford the higher deductible amount in case you need to file a claim for vehicle repairs.

For older vehicles with lower market values, consider whether collision and comprehensive coverage remain cost-effective. If your car is worth less than $4,000-5,000, and you’re paying high premiums for comprehensive and collision coverage, dropping these coverages might make financial sense. You can continue carrying liability coverage while self-insuring for physical damage to your older vehicle.

Coverage limit adjustments require careful consideration of your assets and potential lawsuit exposure. While you shouldn’t reduce liability limits below reasonable levels, you might adjust them based on your state’s requirements and personal financial situation. However, many experts recommend carrying liability limits well above state minimums to protect against serious accidents that could result in significant property damage or medical expenses.

Consider your vehicle financing situation when adjusting coverage. Lenders typically require collision and comprehensive coverage for financed or leased vehicles, limiting your ability to drop these coverages to save money. However, you can often adjust deductibles or choose different coverage limits within your lender’s requirements.

Some drivers benefit from adjusting their uninsured motorist coverage based on their location and the percentage of uninsured drivers in their area. While this coverage provides valuable protection, you might be able to adjust limits based on your other insurance coverage, such as health insurance that covers medical bills from car accidents.

Remember that small premium savings from inadequate coverage can result in massive financial losses if you experience a serious accident. The goal is finding the right balance between affordable premiums and adequate protection for your specific situation.

Understanding your state’s minimum insurance requirements provides the foundation for building a cheap full coverage insurance policy that exceeds basic legal requirements while remaining affordable. Each state sets different minimum liability limits, and some require additional coverages that affect your overall insurance costs.

Most states require liability coverage split between bodily injury per person, bodily injury per accident, and property damage. For example, a state might require 25/50/25 coverage, meaning $25,000 for bodily injury per person, $50,000 for bodily injury per accident, and $25,000 for property damage. Full coverage policies typically exceed these minimums significantly to provide better protection.

No-fault states require personal injury protection (PIP) or medical payments coverage in addition to liability insurance. This additional requirement increases the cost of basic coverage but provides valuable benefits by covering your medical expenses regardless of who caused an accident. Understanding your state’s no-fault laws helps you optimize your coverage choices and avoid duplicate protection.

Fault states operate under traditional liability systems where the at-fault driver’s insurance pays for damages. In these states, uninsured motorist coverage becomes particularly important since you rely on other drivers having adequate insurance to cover your losses. Many drivers in fault states choose higher uninsured motorist limits to protect against inadequately insured drivers.

Lender requirements often mandate coverage levels that exceed state minimums for financed or leased vehicles. Most auto loans and leases require collision and comprehensive coverage with relatively low deductibles to protect the lender’s investment. This requirement makes full coverage essential rather than optional for many drivers, emphasizing the importance of finding affordable comprehensive protection.

Some states offer low-cost auto insurance programs for qualifying drivers with limited incomes. These programs provide basic coverage at reduced rates, though they typically offer lower coverage limits than traditional full coverage policies. Research whether your state offers such programs if cost is a primary concern.

Understanding your state’s insurance regulations also helps you avoid coverage gaps that could result in penalties, license suspension, or legal liability. Most states require continuous coverage, making it important to maintain your auto insurance policy without lapses to avoid penalties and higher future rates.

Selecting the right insurance company for cheap full coverage requires evaluating multiple factors beyond just price. Different insurers use varying underwriting criteria, offer different discounts, and provide different levels of service, making comprehensive comparison essential for finding the best value.

Financial strength ratings from agencies like AM Best, Moody’s, and Standard & Poor’s indicate an insurer’s ability to pay claims. Choose companies with strong financial ratings to ensure they can fulfill their obligations when you need to file a claim. A cheap auto insurance quote from a financially unstable company can become expensive if they can’t pay your claim or go out of business.

Customer satisfaction scores from J.D. Power and consumer review websites provide insights into real customer experiences with different insurers. Pay attention to ratings for claims handling, customer service, billing, and overall satisfaction. These metrics help you understand what to expect beyond just premium costs.

Different insurers excel in different areas, and their competitive advantages can affect your costs. Some companies specialize in high-risk drivers, others focus on safe drivers with clean records, and some target specific demographics like military families or good students. Understanding each company’s focus helps you identify which insurers are most likely to offer competitive rates for your profile.

Digital capabilities vary significantly between insurance companies and can affect both convenience and cost. Companies with robust mobile apps, online policy management, and digital claims filing often offer lower rates due to reduced operational costs. Consider whether you prefer traditional agent relationships or are comfortable managing your auto policy online for potential savings.

Claims handling reputation becomes crucial when you need to use your insurance coverage. Research how quickly different companies process claims, their settlement practices, and customer satisfaction with the auto claims process. The cheapest coverage provides poor value if claims handling is slow, difficult, or unfair.

Regional insurers sometimes offer competitive rates in specific geographic areas where they focus their business. While national companies provide broader recognition and standardized service, regional insurers might offer better rates or more personalized service in their target markets.

Consider each company’s approach to rate increases and long-term pricing stability. Some insurers use aggressive initial pricing to attract customers, then raise rates significantly at renewal. Others maintain more stable pricing over time, potentially providing better long-term value even if their initial quotes are slightly higher.

While seeking cheap full coverage insurance, certain situations warrant considering higher coverage limits despite increased costs. Understanding when additional protection provides good value helps you make informed decisions about coverage enhancement versus cost savings.

High personal assets increase your exposure to lawsuits following serious accidents. If you own valuable property, have significant savings, or earn a high income, carrying liability limits well above state minimums protects these assets from potential judgments. The additional cost for higher liability limits is often relatively modest compared to the protection provided.

High-traffic areas with frequent accidents increase your likelihood of being involved in serious collisions that could result in multiple injuries or significant property damage. If you regularly drive in congested metropolitan areas, consider whether minimum liability limits provide adequate protection for worst-case scenarios.

Uninsured motorist coverage becomes particularly important in states with high percentages of uninsured drivers. If data shows that many drivers in your area lack adequate insurance, increasing your uninsured motorist limits protects you from having to pay for medical bills and vehicle damage when at-fault drivers can’t cover your losses.

Consider umbrella insurance as a cost-effective way to add significant liability protection beyond your auto policy limits. Umbrella policies typically provide $1-5 million in additional liability coverage at relatively low annual costs, offering excellent value for high-asset individuals who need extensive protection.

Comprehensive and collision coverage limits should reflect your vehicle’s value and your ability to replace it. For expensive vehicles or situations where losing transportation would create significant hardship, maintaining full replacement value coverage makes sense even if it costs more than minimum coverage.

Medical payments coverage or personal injury protection limits should align with your health insurance coverage and potential medical costs in your area. If you have excellent health insurance, you might choose lower medical payments limits, but if your health coverage has high deductibles or limited coverage, higher auto insurance medical limits provide valuable backup protection.

Evaluate whether the additional cost for higher limits fits within your overall budget and risk tolerance. Sometimes paying slightly more for enhanced coverage provides better value than trying to minimize costs at the expense of adequate protection.

Pursuing cheap full coverage insurance can expose you to companies and policies that seem affordable but provide poor value or inadequate protection. Recognizing warning signs helps you avoid costly mistakes that could leave you underprotected or dealing with problematic insurers.

Companies with poor financial stability pose significant risks regardless of their attractive rates. Avoid insurers with low financial strength ratings or recent financial difficulties. If a company can’t pay claims or goes out of business, even the cheapest premiums provide no value. Research each potential insurer’s financial ratings before purchasing coverage.

Extremely low coverage limits that barely meet state minimums often indicate inadequate protection for modern vehicle values and medical costs. Be suspicious of quotes that seem too good to be true, especially if they include unrealistically low liability limits or high deductibles that would create financial hardship if you needed to file a claim.

Hidden fees and charges not included in initial quotes can make seemingly cheap coverage expensive once you factor in all costs. Ask about processing fees, installment charges, policy fees, and any other costs beyond the quoted premium. Some companies advertise low rates but add significant fees that weren’t disclosed during the initial quote process.

Poor customer service records indicate potential problems when you need assistance with your auto insurance policy or filing claims. Research customer satisfaction ratings and online reviews to identify companies with patterns of poor service, delayed claim payments, or difficult policy management processes.

Pressure tactics from sales representatives often indicate companies more focused on closing sales than providing appropriate coverage. Reputable insurers allow you time to review proposals, compare options, and make informed decisions. Be wary of companies demanding immediate decisions or using high-pressure sales techniques.

Coverage gaps or unusual exclusions in policy terms can leave you without protection when you expect coverage. Carefully review policy documents to ensure standard coverages are included and that exclusions are reasonable and clearly explained. Some companies reduce rates by excluding common coverage elements that most drivers expect.

Inconsistent pricing between initial quotes and final premiums often indicates bait-and-switch tactics or poor business practices. If final pricing differs significantly from initial quotes without reasonable explanation, consider other options rather than proceeding with questionable companies.

How much does full coverage insurance typically cost compared to liability-only policies?

Full coverage car insurance typically costs 2-3 times more than liability-only coverage, with the average annual cost exceeding $4,000 for comprehensive protection. However, the exact difference varies significantly based on your location, driving record, vehicle type, and chosen coverage limits. While liability-only policies might cost $1,000-1,500 annually, adding collision and comprehensive coverage often increases costs to $2,500-4,500 or more. The additional cost reflects the increased protection for your own vehicle and enhanced coverage for medical expenses and uninsured motorist situations.

Can I get full coverage insurance with a poor driving record or bad credit?

Yes, you can obtain full coverage insurance with a poor driving record or bad credit, though you’ll typically pay higher premiums. Many insurance companies, like specialize in high-risk drivers and offer full coverage options, though rates will be substantially higher than those offered to preferred customers. Some insurers focus specifically on drivers with traffic violations, accidents, or credit challenges. Shopping with multiple companies becomes even more important in these situations, as different insurers weigh risk factors differently and may offer more competitive rates despite your driving or credit history.

What’s the difference between actual cash value and replacement cost coverage?

Actual cash value coverage pays for your vehicle’s current market value minus depreciation at the time of loss, while replacement cost coverage pays the amount needed to replace your vehicle with a similar one. Most auto insurance policies use actual cash value, which means you’ll receive less than what you originally paid for your car due to depreciation. For newer vehicles or situations where you owe more than your car’s current value, gap insurance can cover the difference between actual cash value and your loan balance, providing more complete financial protection.

How often should I shop around for cheaper full coverage insurance rates?

You should compare car insurance quotes at least annually during your renewal period, and potentially more frequently if your circumstances change significantly. Insurance companies regularly adjust their rates and underwriting criteria, meaning the cheapest option can change from year to year. Additionally, life changes like moving, getting married, buying a new vehicle, or having traffic violations resolved can affect your rates with different insurers. Many experts recommend shopping every 6-12 months to ensure you’re getting the best available rates for your current situation.

Is it worth switching insurance companies to save $20-30 per month on premiums?

Switching insurance companies for monthly savings of $20-30 is generally worthwhile, as this represents $240-360 in annual savings. However, consider factors beyond just price when making the switch. Research the new company’s financial stability, customer service reputation, and claims handling practices to ensure you’re not sacrificing service quality for lower rates. Also factor in any switching costs, loss of loyalty discounts with your current insurer, and the time required to make the change. If the new company offers comparable or better service with significant savings, switching typically makes financial sense.

Compare & get covered fast

Find and compare auto insurance in minutes, and get your free credit score.

Choose when you pay

Select payment dates that line up with your payday.

Manage everything in one place

Track your policy, manage payments, and request a payment extension right from your dashboard.

.svg)