If you’re a high-risk driver searching for affordable coverage, you’ve probably come across Good2Go. This in-depth 2026 review breaks down everything you need to know about Good2Go auto insurance—from pricing and coverage options to claims handling and customer service—all from OCHO’s perspective as an independent digital broker that helps drivers compare real-time quotes. Good2Go primarily serves drivers in the Eastern and Southern U.S. states, operating exclusively within the United States, and does not provide coverage outside the country.

Good2Go Auto Insurance is a nonstandard auto insurance provider that’s been helping higher-risk and budget-constrained drivers get behind the wheel legally since the early 1990s. The company operates on a simple premise: provide minimum limits insurance so drivers can meet state requirements without breaking the bank.

The business traces its roots back to 1992 when it was established as American Independent Companies, Inc. (AICI). The company went through a rebranding around 2016, unifying its member companies under the Good2Go Auto Insurance name that customers recognize today. The insurance carrier is headquartered in Atlanta, Georgia, and has built its reputation around serving drivers that standard insurers often turn away.

So what exactly does “nonstandard” auto insurance mean? It refers to coverage designed for drivers who don’t fit the typical risk profile that companies like State Farm or GEICO prefer. This includes people with prior accidents on their record, lapses in coverage, DUI convictions requiring SR-22 filings, poor credit histories, or limited insurance experience. Good2Go has carved out its niche by saying “yes” when others say “no.”

The company’s slogan—“Drive legal for less”—captures their mission perfectly. Rather than pushing comprehensive packages with all the bells and whistles, Good2Go focuses on helping customers meet state minimum liability requirements at a price that won’t drain their hard earned money. You can buy policies directly through their website, by phone, or through agency partners. It’s worth noting that Good2Go sometimes functions as both insurer and broker depending on the state, which can occasionally cause confusion about who’s actually underwriting your policy.

From OCHO’s perspective, we see Good2Go as one of several options for high-risk drivers—not a one-size-fits-all solution. When you compare quotes through our platform, Good2Go often appears as a competitive choice for specific risk profiles, but it’s not always the best fit for everyone.

Good2Go is a regional player with a strong footprint in the Eastern U.S. and select Southern and Midwestern states. Unlike national giants that operate in all 50 states, Good2Go has a more focused geographic presence.

In 2026, Good2Go commonly writes policies in states including Pennsylvania, Georgia, Florida, South Carolina, Ohio, Indiana, Delaware, Illinois, Kentucky, Maryland, and Virginia. However, the company is not available everywhere. If you’re in Hawaii, Kansas, Massachusetts, Alaska, Rhode Island, or Montana, you will be unable to get a Good2Go policy. Coverage availability can also vary at the county level within states, so your specific location matters quite a bit.

The typical Good2Go customer fits a particular profile. These are drivers who need SR-22 filings after serious violations, people with recent lapses in coverage, those with multiple tickets or at-fault accidents, and budget-constrained consumers who only want state minimum liability to stay legal on the road. If you’ve been turned away or quoted sky-high premiums by standard insurers, Good2Go may be willing to work with you.

That said, Good2Go usually isn’t the right fit for everyone. Families with newer vehicles who want high liability limits, homeowners looking to bundle policies for deeper discounts, or drivers with pristine records will likely find better value and service elsewhere. Good2Go’s strength is getting high-risk drivers covered—not competing with full-service carriers on features and support.

Here’s a detail breakdown of Good2Go’s coverage options, including what each type of insurance covers and how it helps drivers meet legal requirements.

Good2Go emphasizes minimum limits car insurance policies designed to satisfy state law requirements. While the company does offer some optional coverages, the range is narrower than what you’d find with large national carriers.

Here’s a breakdown of the major coverage types Good2Go typically offers in 2026:

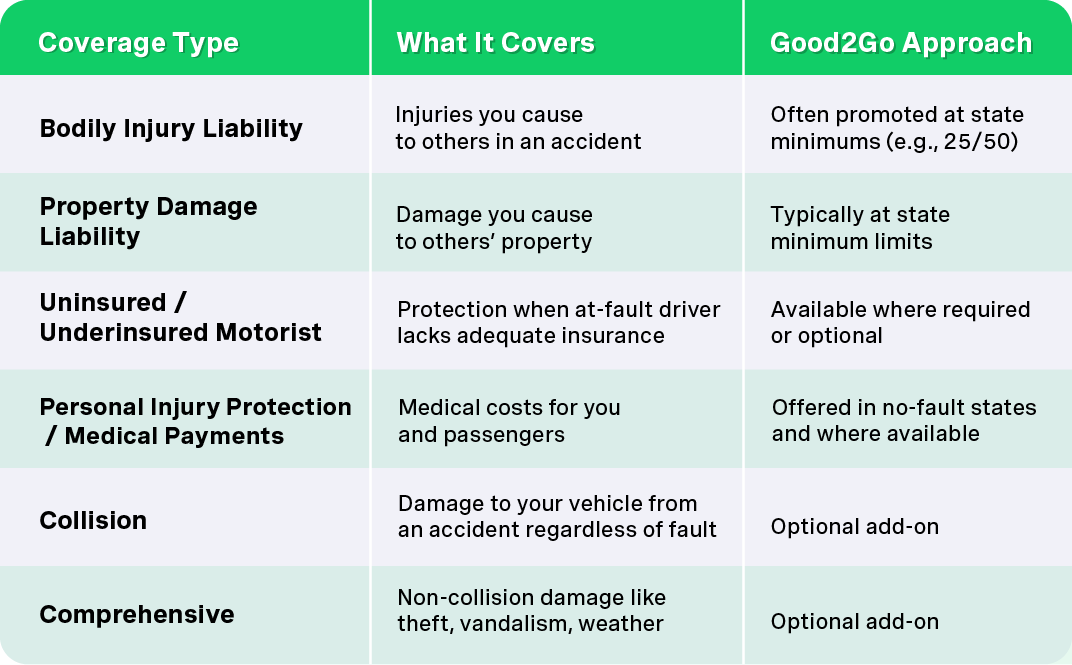

Collision coverage pays for damage to your vehicle from accidents, regardless of who is at fault. Bodily injury liability pays for medical expenses and legal fees of others if you are at fault in an accident. Comprehensive coverage protects against damage to your vehicle from non-collision incidents such as theft or vandalism. Liability auto insurance helps drivers meet state minimum requirements for bodily injury and property damage.

Good2Go offers standard coverages including liability, collision, comprehensive, uninsured/underinsured motorist, and PIP.

Good2Go commonly promotes minimum limits such as 25/50/25 (that’s $25,000 per person for bodily injury, $50,000 per accident, and $25,000 for property damage) or whatever the specific state mandates. Higher limits are sometimes available, but they’re not the company’s primary selling point.

The insurance company also offers a few low-cost add-ons that can provide extra peace of mind:

These extras typically run approximately $3–$15 per month depending on your state and vehicle.

However, there are notable gaps in Good2Go’s offerings. The company doesn’t have an accident forgiveness program, offers limited options for new-car replacement coverage, doesn’t provide rideshare endorsements for Uber or Lyft drivers, and lacks advanced telematics or pay-per-mile programs that some competitors use to reward safe driving.

From OCHO’s perspective, Good2Go works best as a way to get legal quickly at low limits. If you need more robust coverage, our platform can show you side-by-side quotes from other carriers to help you find the right balance of price and protection.

Good2Go can be competitively priced for high risk drivers compared with other nonstandard carriers. The company has built its business around serving people who would pay even more elsewhere. That said, Good2Go’s typical premiums still sit above the U.S. average because of the higher-risk pool it serves.

In 2026, an estimated average annual premium for a typical driver profile with Good2Go runs around $2,900–$3,000. That’s roughly 20–25% above the national average for car insurance. However, context matters: if you have serious violations on your record, this price may actually represent significant savings compared to what companies like Progressive or GEICO would charge you—assuming they’d even offer you a policy.

Several key rating factors determine what you’ll actually pay:

To give you a better estimate of what to expect, consider these scenarios:

A 28-year-old driver in Atlanta with one at-fault accident in the past three years, seeking minimum limits coverage, might see Good2Go offer rates 15–30% lower than what mainstream carriers quote. Meanwhile, a 45-year-old in Philadelphia with a recent lapse in coverage but no accidents could find Good2Go willing to offer a policy when others decline or add heavy surcharges.

Good2Go typically advertises low down payments to get you started, which helps when money is tight. However, even a “low” down payment can be a stretch for working-class drivers living paycheck to paycheck. This is where OCHO’s financing model can help: we can often spread that upfront cost into smaller, interest-free installments synced with your pay cycle, potentially reducing your out-of-pocket expense to $0 at checkout.

Since everyone’s situation is different, we always recommend getting real-time quotes through OCHO to see exactly how Good2Go compares in your ZIP code and risk profile. Don’t rely on national averages—your actual price could be quite a bit different.

Here’s a detail on the discounts and savings options available with Good2Go, providing a comprehensive breakdown to help you understand how you can lower your premium.

One of Good2Go’s strengths is offering discounts that don’t always require a perfect driving history. This is unusual among many insurers and can be genuinely helpful for drivers rebuilding their insurance record.

Multi-Vehicle Discount: If you’re insuring more than one car or adding multiple drivers in your household, Good2Go often provides discounts up to about 25% off your premium. This can add up to real money when you’re covering a family’s vehicles.

Prior Insurance Discount: Here’s where Good2Go really stands out. Drivers who can show 6–12 months of continuous coverage may qualify for discounts up to about 40%, even if they have past infractions. This rewards people who maintain coverage—a smart incentive that helps customers save while reducing risk for the company.

Other Available Discounts: Depending on your state and the specific underwriting company handling your policy, you might also qualify for safe driver discounts, homeowner discounts, defensive driving course discounts (typically requires a state-approved course), and pay-in-full discounts if you can pay your entire premium upfront.

It’s important to understand that discount availability and exact percentages vary by state and underwriting company. Since Good2Go policies can be written by different affiliated insurers depending on where you live, the specific savings you qualify for may differ from what a friend in another state receives.

The takeaway? To maximize your savings with Good2Go, focus on these concrete steps:

Let’s be direct: Good2Go has a mixed reputation in 2026. Some customers praise helpful individual agents by name and appreciate the patience shown when explaining minimum-coverage options to first-time buyers. Customers consistently praise the staff for their positive attitude, knowledge, and efficiency, and reviewers specifically mention individual agents by name, expressing gratitude for their professionalism and kindness. Many positive reviews also note that the company fosters an environment of respect for its employees, which is reflected in positive staff interactions. Others have reported frustrating experiences that range from inconvenient to terrible.

Looking at third-party metrics, Good2Go’s NAIC complaint index sits significantly above 1.0, indicating substantially more complaints than expected for an insurance company of its size. Average star ratings on consumer review sites tend toward the lower end, and there are numerous concerns related to billing issues, unexpected cancellations, and claims delays. Good2Go has consistently low customer service ratings due to complaints about long wait times and unresponsive claims adjusters.

Common complaint themes include:

On the positive side, some reviewers highlight agents who were eager to assist with documentation for dealerships, representatives who took time explaining coverage details, and phone service that was appreciated for its friendliness. When things go right with Good2Go, customers have reported smooth experiences getting their proof of insurance and ID cards quickly.

Here’s a practical concern: Good2Go does not currently offer a fully featured mobile app. The company relies on a web portal for payments and managing policy documents, and claims must be reported by phone rather than through a modern online or in-app process. If you need to file a claim after an accident, be prepared to speak with a claims representative who will reach out to review the details of the incident, and keep detailed written records of all communication.

OCHO’s perspective? We advise drivers to weigh price savings against service risk. Read recent reviews specific to your state, and if you do go with Good2Go (or any nonstandard insurer), keep careful records of every interaction—emails, call logs, photos of damage, and a copy of the police report if applicable. This documentation can prove invaluable if you ever need to settle a claim or dispute.

If you are unable to access Good2Go’s website or services due to a network security block and believe this was a mistake, you should report it by filing a ticket for resolution.

If you have a Good2Go Auto Insurance auto insurance policy, you can manage your account through the company’s online customer portal. From there, policyholders can typically view policy documents, make payments, update certain account details, and access claims information using a desktop or mobile browser.

For drivers with busy schedules or irregular pay cycles, having online access to payment and policy details can be helpful. However, Good2Go does not currently offer a dedicated mobile app for policy management. While many insurers now provide app-based account access, Good2Go relies on its browser-based portal for digital servicing.

Across the broader insurance industry, mobile apps have become standard. Major carriers such as GEICO, Progressive, and State Farm offer mobile apps that allow customers to view ID cards, make payments, track claims, request roadside assistance, and receive push notifications. According to industry reports from firms like J.D. Power, digital experience—including ease of navigation, payment processing, and claims tracking—plays an increasing role in overall customer satisfaction.

Because Good2Go relies solely on its website portal, customers who prefer app-based functionality may find the experience more limited compared to competitors. As with any online system, occasional technical issues or processing delays can occur, so it’s wise to confirm that payments have successfully processed and to keep confirmation records for important account changes.

If you encounter issues, contacting customer service directly is often the fastest way to resolve time-sensitive concerns. As digital tools continue to evolve across the insurance industry, many drivers now expect streamlined, mobile-friendly policy management. Whether Good2Go expands its digital capabilities in the future remains to be seen—but for now, policyholders should understand how its current system works and plan accordingly.

Getting a Good2Go quote in 2026 typically happens through three channels: the company’s website, a direct phone call, or through a broker or agency like OCHO.

If you visit Good2Go’s website directly, be aware that the site sometimes routes visitors to partner carriers or third-party comparison tools. This can be confusing for drivers who assume they’re buying directly from Good2Go as the insurance carrier, only to find a different company name on their actual policy documents.

Common experiences reported by reviewers include multiple transfers between representatives, being redirected to another branded insurer (like Allstate or a regional partner) without clear disclosure, and needing to confirm who is actually underwriting the policy before binding. The business structure can make it unclear who you should contact if you have questions later.

OCHO’s process is designed to be simpler and more transparent. When you request a quote through our platform, you may interact with a knowledgeable representative who can assist you in obtaining quotes and clarifying policy details. We pull live rates from multiple insurers—including Good2Go where available—and clearly label which company is offering each option. You see coverage details and prices side by side, with no mystery about who’s backing the policy.

For high-risk drivers especially, this comparison approach helps you understand when Good2Go is truly the best value versus when another carrier offers better coverage or service at a comparable price. We’ve seen plenty of cases where Good2Go comes out ahead, and plenty where a lesser-known regional carrier beats them on both cost and customer satisfaction.

Regardless of which insurer you choose through OCHO, we provide instant digital proof of insurance so you can manage registration, leave the dealership lot, or handle DMV requirements the same day. We can also coordinate start dates, documents for dealers, and SR-22 filings where needed—all within a single experience.

Buying directly from Good2Go can work fine if you already know exactly what coverage you want, you’ve done your homework on competitors, and you have the cash on hand for their down payment. For everyone else, using OCHO often makes more sense.

Here’s what you gain by buying your insurance through OCHO:

The financing advantage is where OCHO really shines for working-class drivers. Good2Go may advertise low down payments, but even “low” can feel steep when you’re managing a tight budget. OCHO can often turn that required down payment into smaller, interest-free installments synced with your pay cycle—whether you get paid biweekly, or monthly. In many cases, we can reduce your upfront obligation to $0 at checkout.

When it comes to payment methods, keep in mind that paying your Good2Go insurance premium by phone may incur an additional fee.

There’s also a credit-building benefit. OCHO reports on-time payments to help customers build or strengthen their credit over time. For high-risk or credit-challenged drivers using OCHO as a stepping stone to better rates in the future, this can be genuinely valuable. Improve your credit and driving record, and you may qualify for standard insurers with lower premiums within a year or two.

Additionally, OCHO doesn’t charge late fees for short delays within our grace terms. This gives drivers a bit more breathing room than some insurers that cancel quickly for missed payments—a frequent source of complaints with nonstandard carriers.

For many customers, OCHO’s payment flexibility is more practical than dealing with the insurer alone, especially when budgets are tight and cash flow is irregular.

Good2Go is a niche option that can be helpful for getting legal quickly if you’re a high-risk driver in a state the company serves. It’s not ideal for drivers who prioritize top-tier claims handling, extensive coverage options, or digital convenience—but it fills an important gap in the market for people who’ve been turned away elsewhere.

Key Pros:

Key Cons:

Who should consider Good2Go? Drivers with a recent lapse in coverage, multiple violations, DUI convictions requiring SR-22, or an immediate need for state-minimum proof of insurance. If your primary goal is to get insured quickly at the lowest possible cost, Good2Go deserves a look.

Who should look elsewhere? Families with new cars needing comprehensive protection, homeowners who want bundled policies for better discounts, or drivers with clean records who can qualify for preferred rates with standard insurers.

Remember: our flexible, interest-free payment plans can reduce or eliminate the upfront down payment burden, making affordable coverage accessible even when your budget is stretched thin.

Looking ahead, Good2Go Auto Insurance? They're sitting pretty when it comes to serving high risk drivers and folks who've been left out in the cold by other companies. You know what we're talking about - drivers who just need affordable coverage and minimum limits without the runaround. Good2Go's whole thing about helping drivers stay legal with fast, easy, and budget-friendly auto insurance? That hits home for tons of people who've been turned away everywhere else. But here's the thing - if they want to stay in the game while the insurance world keeps changing, they've got some serious work to do.

First up, customer service and claims processing needs a major overhaul, and fast. Too many customers are griping about sitting on hold forever and getting the silent treatment when they need help with claims. Come on, it's 2024! They could totally fix this with online claims filing and real-time updates that actually tell you what's going on. Give drivers who're counting on that coverage some peace of mind when they're dealing with an accident - it's not rocket science.

Second, let's talk digital upgrades. We're talking mobile app, user-friendly website - the works. Make it dead simple for customers to manage their accounts, pay their bills, and grab their documents without jumping through hoops. These aren't just nice-to-haves anymore - they're make-or-break features that'll help Good2Go blow past the competition when it comes to winning over high risk and underserved drivers.

And here's the bottom line - keeping premiums affordable while actually delivering reliable service isn't optional if you want customers who stick around. Listen to what people are saying, fix problems before they blow up, and throw in some flexible payment options that actually work for real people's budgets. That's how Good2Go builds its rep as the go-to choice for minimum limits and affordable coverage that doesn't suck.

So what's it gonna be? Good2Go's future comes down to this: can they balance rock-bottom prices with service that doesn't leave people hanging? Can they get with the program on digital tools that customers expect? Focus on these areas, and they'll keep delivering on their mission to help drivers who need it most. Miss the mark? Well, there's always room for someone else to come in and do it better.

Good2Go primarily markets state-minimum liability policies, but the company can offer collision and comprehensive coverage in many states. Together, these options can approximate what people call “full coverage” for older vehicles. However, Good2Go typically doesn’t specialize in high-limit or feature-rich packages for brand-new or luxury cars. Options like new-car replacement, gap insurance, or advanced endorsements are usually limited or unavailable.

Yes, Good2Go is often willing to file SR-22 forms in states that require them after serious violations like DUIs or driving without insurance. This makes the company a common option for drivers who need to prove financial responsibility to reinstate their license. After purchasing a qualifying policy, Good2Go electronically files the SR-22 with your state’s DMV. OCHO can help you compare SR-22-friendly insurers, handle the documentation, and structure payments to make the higher SR-22-related premiums more manageable through interest-free installments.

In typical cases, Good2Go issues digital proof of insurance within minutes of binding a policy by phone or online. This can be emailed or printed for registration or dealership purposes. Some customer reviews specifically highlight agents quickly sending ID cards and declarations pages directly to car dealerships to speed up vehicle delivery.

Good2Go operates as both, depending on the state. The company is associated with multiple underwriting companies (legacy AICI companies and other affiliates) and also acts as an agency or broker in some markets, placing policies with partner insurers. This structure sometimes causes confusion for customers about which company is actually responsible for claims and billing—especially when the brand on the website doesn’t match the insurer named on the policy documents.

Like most nonstandard insurers, Good2Go may have relatively short grace periods and can move quickly to cancel policies for non-payment. This is a frequent source of complaints and can leave you uninsured if you’re not careful. Review your billing schedule and any grace period language in your Good2Go policy carefully, and set up reminders or automatic payments if possible. When purchasing through OCHO, customers can often align payments with their pay cycle and avoid late fees on our side. This reduces the chance of lapses and helps preserve eligibility for continuous-coverage discounts over time—a real benefit when you’re working to rebuild your insurance history.

Compare & get covered fast

Find and compare auto insurance in minutes, and get your free credit score.

Choose when you pay

Select payment dates that line up with your payday.

Manage everything in one place

Track your policy, manage payments, and request a payment extension right from your dashboard.

.svg)