Driving without insurance is illegal in almost every U.S. state, and the consequences hit fast and hard. Get pulled over without valid insurance, and you’re looking at immediate fines, license suspension, vehicle impoundment, and long-term financial fallout that can follow you for years. Your driver's license can be suspended or revoked as a result of being caught driving without insurance, and you may need to provide proof of insurance, such as an SR-22 form, to reinstate your driving privileges. Even a routine traffic stop for a broken tail light can spiral into a misdemeanor charge if you can’t produce proof of coverage.

The penalties get exponentially worse if you’re involved in a serious accident while uninsured. Suddenly, you’re not just facing tickets—you’re personally liable for every dollar of property damage and medical bills, which can easily run into tens of thousands or even hundreds of thousands of dollars.

Exact penalties depend heavily on your state. Many states use electronic databases to track insurance status, so you could face penalties even if you are not stopped by police. First offense fines typically range from about $100 to $1,000, while repeat offenses can reach $5,000 or more in places like Massachusetts, often paired with jail time. The rest of this article walks you through exactly what happens when you’re caught driving without insurance—from DMV notifications to traffic stops to accidents—and how being uninsured affects your future insurance rates and finances.

Driving without insurance is a risk that can have serious consequences for any motorist. When you’re caught driving without insurance, you’re not just facing a minor inconvenience—legal penalties, financial responsibility for damages, and even the loss of your driving privileges can follow. Driving uninsured means you’re exposed to significant risks every time you get behind the wheel, from hefty fines to the possibility of being personally liable for thousands of dollars in damages if an accident occurs. That’s why maintaining proper insurance coverage isn’t just a legal requirement—it’s a crucial step in protecting yourself, your finances, and others on the road. Understanding what’s at stake when driving without insurance is the first step toward making informed, responsible decisions about your coverage.

Every state sets its own rules for car insurance, but nearly all require drivers to carry at least a minimum level of liability insurance coverage. Liability insurance is designed to protect you from the financial consequences of causing an accident, covering the costs of property damage and medical expenses for other parties involved. In addition to basic liability insurance, many states require drivers to carry additional protections, such as uninsured motorist coverage—which helps pay for your injuries or damages if you’re hit by an uninsured driver—or personal injury protection (PIP), which covers medical expenses for you and your passengers regardless of fault. Failing to meet your state’s insurance requirements can lead to legal penalties, including fines, license suspension, and increased financial exposure if you’re involved in a crash. Knowing exactly what insurance coverage your state mandates is essential to staying compliant and safeguarding your financial future.

Here’s the reality: 49 states (plus Washington, D.C.) require auto liability insurance before you can legally operate a motor vehicle on public roads. New Hampshire is the only state that doesn’t mandate traditional liability coverage—but even there, you must prove financial responsibility if you cause a car accident. Penalties for driving uninsured generally include fines, license and registration suspension, and in many cases, vehicle impoundment or jail time.

The severity of legal penalties depends on several factors:

These consequences depend on:

Some states have gotten aggressive about catching uninsured drivers before they’re even pulled over. Electronic verification systems can flag your insurance status automatically, meaning you could face penalties simply because your policy lapsed—even if you never got behind the wheel.

Most auto insurers are required to electronically notify your state DMV when your liability insurance policy is started, changed, or canceled. This data gets cross-checked against vehicle registration records, creating a system where your insurance lapse can be detected without any traffic enforcement involvement.

When a lapse is reported, many states can take immediate action:

For example, some states charge administrative fees of $150–$300 just to reinstate your registration after a coverage gap. Repeat lapses lead to higher fees and longer suspensions. In Kansas, three insurance violations within a certain period can trigger a three-year license revocation under the state’s Habitual Driving Statute.

Here’s what catches many vehicle owners off guard: even if you’re not actively driving, allowing a registered motor vehicle to go uninsured can still trigger DMV penalties. You’ll face fees and suspension until you either purchase insurance or officially surrender your plates to the state.

Picture this: you’re driving home after work when you see those flashing lights in your rearview mirror. The officer walks up, asks for your driver’s license, registration, and proof of insurance. You hand over the first two, but you’ve got nothing for the third. Now what?

The likely immediate outcomes when caught driving without valid insurance include:

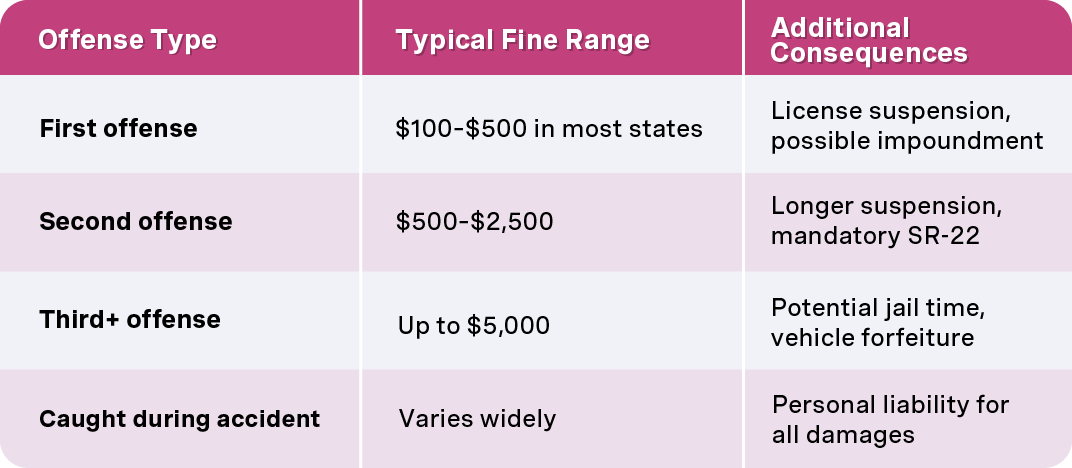

In states like Kansas, that first offense carries fines from $300 to $1,000, plus potential six months of jail time and a suspended license. Delaware hits even harder with fines up to $4,000 and six-month suspensions. Connecticut can add up to three months imprisonment.

Here’s a small silver lining: if you actually had valid insurance but simply couldn’t produce proof at the stop, some states let you show documentation to the court date or submit it online by a certain deadline. In these cases, the ticket may be reduced or dismissed—but don’t count on this as a strategy.

This is where consequences escalate dramatically. Regardless of whether you caused the collision, you’re violating state insurance laws and may have zero coverage for injuries or property damage. The financial consequences can be catastrophic.

If you’re the at fault driver:

You become personally liable for everything—medical bills, vehicle repairs, lost wages, and pain and suffering claims from injured parties. A serious accident can easily generate costs in the tens of thousands, and severe injuries push that into hundreds of thousands of dollars. Without an insurance company absorbing these costs, you face:

As one Wichita attorney notes, even state minimum coverage limits of $25,000 per person/$50,000 per accident often fall short of covering modern repair and medical costs. Without any coverage, you’re completely exposed.

If you’re not at fault:

The other driver’s liability coverage may still pay for your damages—but there’s a catch. Some states have “no pay, no play” laws that can limit your ability to collect non-economic damages like pain and suffering compensation if you were driving uninsured. You saved a few hundred dollars on premiums but potentially gave up thousands in legitimate compensation.

Regardless of fault, accidents while uninsured commonly lead to:

In practical terms, driving without complying with your state’s financial responsibility law is illegal everywhere in the U.S., even though the specific rules differ slightly by state.

Forty-nine states plus Washington, D.C. require at least minimum liability insurance to register and legally operate a vehicle on public roads. These coverage limits vary—Kansas requires $25,000/$50,000 for bodily injury liability coverage, while other states set different thresholds.

New Hampshire is the exception—sort of. The only state that doesn’t mandate traditional liability insurance, New Hampshire instead requires drivers to prove they can pay for damages after an at fault accident. If you cause a crash and can’t cover the costs, you’ll lose your driving privileges until you pay up or file proof of future financial responsibility.

Some states allow alternatives to traditional insurance:

These alternatives exist, but they’re generally impractical for individual drivers. The required amounts are steep, and maintaining an auto insurance policy is almost always the simpler and more affordable route.

The laws surrounding driving without insurance can vary dramatically from state to state, making it important to understand the specific requirements where you live. For example, California mandates that drivers carry at least $15,000 in bodily injury liability coverage per person, $30,000 per accident, and $5,000 for property damage. These minimums are designed to ensure that drivers can cover the costs of injuries and property damage if they’re at fault in a crash. On the other hand, New Hampshire stands out as the only state that does not require auto insurance by default. However, even in New Hampshire, drivers must prove financial responsibility if they cause an accident—meaning you could still face severe financial consequences if you’re found at fault without insurance coverage. Understanding your state’s liability coverage requirements and the penalties for driving without insurance is key to avoiding costly legal trouble and ensuring you’re protected in the event of an accident.

The true cost of driving uninsured goes far beyond the initial ticket. Between fines, fees, increased premiums, and potentially life-altering judgments after an accident, the financial hardship can compound quickly.

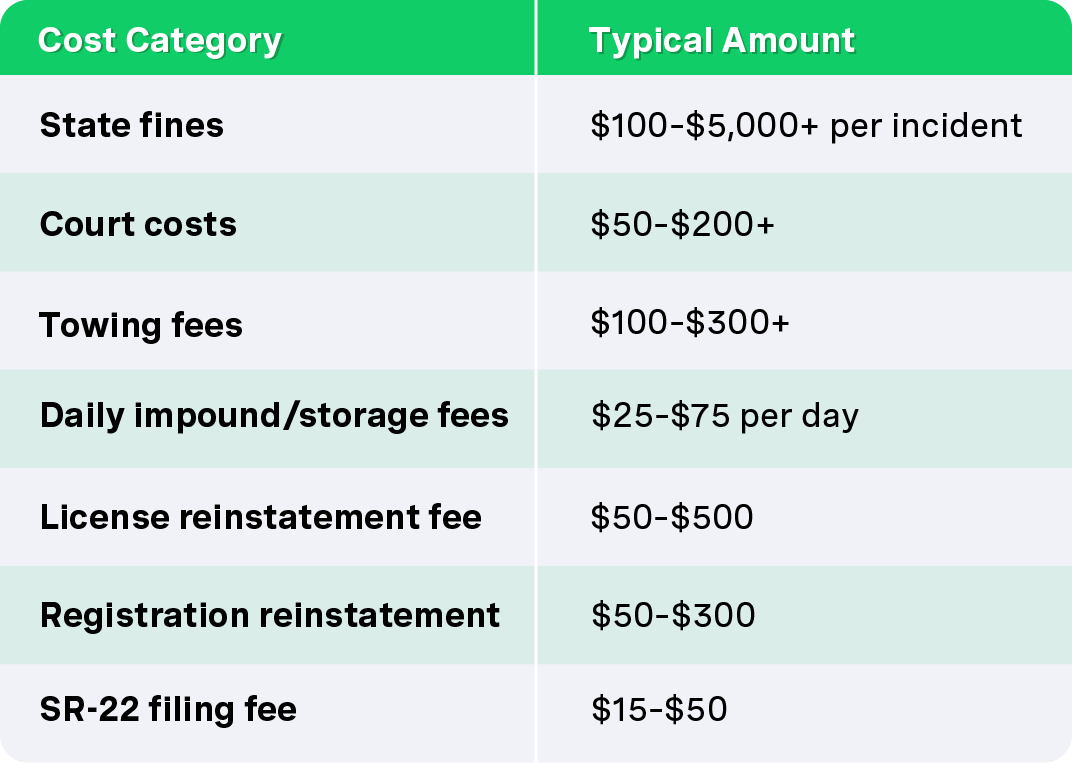

Direct costs when caught:

If you cause an accident while uninsured, add:

Now compare all this to the cost of staying properly insured. The national average for minimum liability coverage runs roughly a few hundred dollars per year—sometimes just $40–$60 per month. That’s a fraction of what you’ll pay if caught driving without coverage even once.

An insurance violation for driving uninsured gets recorded on your driving history and treated by auto insurers as a serious red flag. This isn’t like a minor speeding ticket that fades into the background.

An uninsured-driving violation can:

Here’s how insurers typically react when they see this violation:

Combine a no-insurance violation with an at fault accident, and you’re likely looking at the highest-risk tier. Full-coverage policies can cost several thousand dollars per year in these situations—assuming you can find an insurer willing to write the policy at all.

The irony is brutal: people often skip insurance to save money, only to end up paying far more in insurance rates once they’re caught.

Having the right insurance coverage is about more than just following the law—it’s your primary defense against the financial consequences of an accident. Without insurance, you could be personally liable for medical bills, property damage, and other expenses that arise from a crash. These costs can quickly add up, leading to financial hardship or even bankruptcy for uninsured drivers. Car insurance provides a crucial safety net, covering many of the expenses that would otherwise come out of your own pocket. In addition, your insurance company can guide you through the claims process, helping you handle paperwork, negotiate with other parties, and resolve disputes. This support can make a stressful situation much more manageable, allowing you to focus on recovery instead of worrying about how you’ll pay for damages or medical care. Ultimately, maintaining insurance coverage is the best way to protect yourself from being personally liable for potentially devastating financial losses.

For many drivers, the cost of car insurance is a real concern—especially as insurance rates continue to rise. However, there are practical ways to afford insurance and avoid the much greater financial risks of driving uninsured. Start by shopping around and comparing quotes from different insurers, as rates can vary widely. Bundling your car insurance with other policies, such as homeowners or renters insurance, can also lead to discounts. Many insurance companies offer additional savings for safe driving, good grades, or installing safety features in your vehicle. If you’re struggling to afford insurance, some states offer low-cost insurance programs specifically for low-income drivers, making it possible to get the coverage you need without breaking the bank. By exploring these options and understanding what factors influence your insurance rates, you can find a policy that fits your budget and keeps you protected on the road.

Being caught without insurance is serious, but it’s not the end of the road. You can take concrete steps to regain legal driving status and financial protection.

Basic steps to get back on track:

Understanding SR-22/FR-44 filings:

An SR-22 isn’t actually insurance—it’s a certificate your insurance company files with the state to prove you carry at least the required minimum coverage. Think of it as the state keeping tabs on you after a violation.

Key things to know about SR-22:

Ways to control costs after a lapse:

Some states offer assigned-risk programs or low-cost insurance options for drivers who can’t find coverage in the regular market. Ask potential insurers about these programs.

Once you have insurance again, preventing another lapse becomes crucial. Repeat offenses trigger increasingly significant penalties, and each violation pushes your insurance rates higher.

Set up payment protection:

If you decide not to drive for a period:

Annual policy review checklist:

Maintaining continuous insurance is the single most effective way to keep your rates down long-term. The claims process becomes smoother when you have uninterrupted coverage history, and insurers reward that consistency.

Can I go to jail for driving without insurance?

Jail time is uncommon for first offense violations in most states, but it becomes more likely with repeat offenses, accidents while uninsured, or combined offenses like DUI. States like Kansas and Connecticut explicitly include jail time as a possible penalty—up to six months in Kansas for a first offense, though actual imprisonment is rare without aggravating factors. If you cause a serious accident while uninsured, criminal charges become much more likely.

Can I drive someone else’s insured car if I don’t have my own insurance?

Generally, yes—car insurance typically follows the vehicle, not the driver. If you borrow a friend’s properly insured car for occasional use, their insurance policy usually provides coverage. However, if you’re a regular driver of that vehicle, you should be listed on the policy. The vehicle itself must have valid insurance, and driving a car you know to be uninsured carries the same penalties as driving your own uninsured vehicle.

What if I can’t afford car insurance?

This is a real problem for many people, and there are realistic options beyond going uninsured:

The math almost always favors minimum coverage over no coverage. A basic liability policy might cost $40–$80 per month in many states, while a single uninsured driving ticket can cost $300–$1,000 plus impound fees, towing fees, and years of higher premiums afterward.

What happens to the other driver if I hit them while uninsured?

The other driver can file a claim against you personally for all damages, medical costs, and losses. If they carry uninsured motorist coverage on their own policy, their insurer may cover their damages and then pursue you for reimbursement. Either way, you become personally liable for everything, and collection efforts can include lawsuits, wage garnishment, and property liens.

How long does an uninsured driving violation stay on my record?

Most insurance violations remain on your driving record for 3–5 years, though this varies by state. Some states keep certain violations visible for longer periods. Insurers can see these violations when you apply for coverage, and the impact on your rates gradually decreases over time—but only if you maintain continuous coverage going forward.

The safest and most cost-effective approach is simple: maintain continuous, legal insurance coverage that at least meets your state’s minimum requirements. The few dollars you might save by going without coverage pale in comparison to the financial consequences of getting caught driving without insurance—let alone the potential disaster of causing an accident while uninsured.

If you’ve been driving without coverage, today is the day to fix it. Compare quotes, find an affordable policy, and get back on the road legally. Your future self will thank you.

Compare & get covered fast

Find and compare auto insurance in minutes, and get your free credit score.

Choose when you pay

Select payment dates that line up with your payday.

Manage everything in one place

Track your policy, manage payments, and request a payment extension right from your dashboard.

.svg)