High risk car insurance is coverage for drivers that most auto insurance providers won’t touch. If you’ve got a DUI on your record, multiple speeding tickets, at fault accidents, or gaps in your coverage history, you’re probably in this category. The industry calls it “non-standard auto insurance,” but let’s be real, it’s insurance for people the big companies don’t want.

Here’s the thing: high risk car insurance isn’t some watered-down version of regular coverage. It’s the same product: liability, collision, comprehensive, the works, just priced differently because insurers view you as more likely to file claims. You’re not getting less protection; you’re paying more for it.

This type of auto insurance policy becomes especially important when:

In 2025, more drivers are falling into the high-risk bucket than ever before. Stricter underwriting, rising claim costs, and inflation have made many insurance companies more selective about who they’ll cover. That’s exactly why specialized providers, like the ones OCHO partners with, have become increasingly important for keeping people legally on the road.

There’s no single national definition of what makes someone a high risk driver. Each insurance provider sets its own rules. But most look at a combination of your driving record, age, credit history, prior insurance coverage, and even the type of car you drive.

Here are the most common reasons insurance companies place someone in the high-risk category:

New drivers, especially young drivers under 25, often get rated as higher risk simply because they lack experience behind the wheel. Similarly, some seniors over 70 face higher premiums due to declining reaction times, especially after minor accidents.

And here’s something that surprises people: gaps in coverage of just 30-60 days, or a poor credit-based insurance score, can push you into high-risk territory even if you’ve never had a single ticket.

The good news? The companies OCHO works with are built specifically to handle these profiles. Being high risk doesn’t automatically mean you’ll be denied coverage.

One major violation can instantly flip your status from “normal driver” to “high-risk” with most insurers. We’re talking about incidents that make insurance companies very nervous.

The typical triggers include:

In most states: California, Texas, Florida, and dozens more, these violations require you to file an SR-22 or FR-44 with your state’s department of motor vehicles. This is essentially proof that you’re carrying at least the minimum required liability coverage. Without it, your driving privileges stay suspended.

OCHO connects drivers who need SR-22 filings with carriers that handle them electronically. In many cases, the filing goes to the state within 24 hours, which means you can get your license reinstated faster than you’d expect.

Here’s the reassuring part: while your premiums will be high right after these violations, careful driving with continuous coverage through OCHO can potentially lower your car insurance costs after three to five years, or at least stop them from increasing dramatically.

Even drivers with a clean driving record can be classified as high risk if they’re very young or very old. It’s not personal, it’s statistics.

Teen and young adult drivers (roughly ages 16-24) have the highest crash rates of any age group. Insurance commissioners and actuaries have decades of data showing this. As a result, this group pays some of the highest high risk car insurance rates in the country, sometimes two or three times what a 40-year-old with the same car would pay.

On the other end of the age spectrum, some insurers rate drivers over 70 as higher risk, especially if there have been recent minor accidents or traffic violations. Slower reaction times and health-related factors play into this.

Here’s something many people don’t realize: you can be classified as high risk even without a DUI or major crash. Coverage gaps and payment problems count too.

Most insurers penalize drivers who have gone uninsured for 30, 60, or 90+ days. They see this as a red flag—if you’ve driven without insurance before, you might do it again. From their perspective, it’s a risk factor they’d rather avoid.

Other factors that trigger high-risk classification include:

This creates a frustrating cycle. You couldn’t afford insurance, so you went without. Now you’re labeled high-risk, which makes insurance even more expensive. Sound familiar?

OCHO focuses on getting these drivers back into continuous coverage quickly. By maintaining on-time payments over 12-36 months with OCHO’s partner carriers, drivers can begin repairing their risk profile and eventually qualify for standard-market rates again.

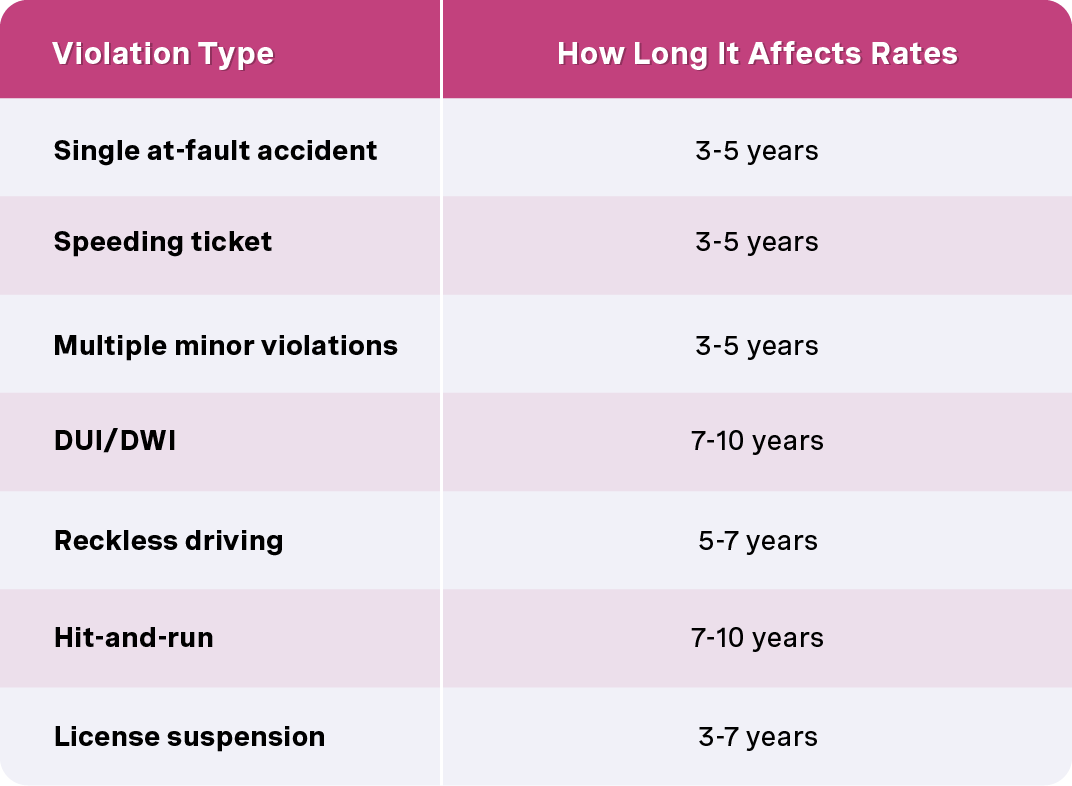

High-risk status isn’t permanent. The duration depends on state law, the type of violation, and each insurer’s underwriting rules.

Here’s the general timeline for SR-22 insurance requirements:

Insurers typically look most closely at the past 36 months when setting high risk car insurance premiums. That means clean driving during this window is especially important for lowering your rates.

OCHO helps drivers plan for this timeline. For example, if you have a DUI from 2024, you might stay with a high-risk carrier for the first 3-4 years through OCHO, then reevaluate your options as the violation ages off your driving history. The goal is to be strategic about when to shop for better rates.

Let’s talk numbers. Prices vary based on your state, age, vehicle, and specific record—but high risk car insurance is significantly more expensive than standard coverage. That’s just the reality.

Based on 2024-2025 industry data, here’s what you’re looking at:

Some carriers charge even more. For example, certain insurers quote over $4,500/year for drivers with a recent DUI. Higher rates are the trade-off for the higher premiums these customers represent.

For minimum liability-only coverage, high risk drivers might pay several hundred dollars more per year than standard customers. Full coverage with collision and comprehensive can easily exceed $2,000-$3,000 annually for challenging profiles. However, there are affordable car insurance options for low-income drivers that can help mitigate these costs.

The key thing to understand: non-standard carriers use more granular pricing. A driver with two minor speeding tickets will be priced differently than someone with one major violation like a DUI. This is where OCHO’s quoting engine shines, it can quickly sort through options from multiple high-risk-focused carriers to find you the best rates for your specific situation.

The fastest way to see real numbers? Get a personalized quote through OCHO using your current vehicle, address, and violation dates.

OCHO isn’t like the big-name insurance companies that focus on customers with perfect records. We’re a marketplace built specifically for high risk car insurance, partnering only with insurers that actively want to write high-risk business.

Here’s what makes us different:

Many insurance companies treat high-risk drivers as customers they’d rather not have. OCHO treats them as customers who deserve options and a path forward.

Getting covered through OCHO is straightforward. Here’s how it works:

Step 1: Enter your details online or in our app Provide your name, address, vehicle information (year, make, model), and specific incidents with approximate dates. For example: a DUI from June 2023, an at-fault accident from October 2022.

Step 2: Get matched with carriers OCHO’s system matches you with high risk car insurance companies comfortable with your exact history. You’ll typically see multiple quotes if carriers are competing for your business.

Step 3: Review your coverage options Compare state minimum liability, higher coverage limits, and optional collision and comprehensive coverage. Select a deductible and payment schedule that fits your budget.

Step 4: Handle SR-22/FR-44 requirements If your state requires a filing, OCHO routes your application to a carrier that files electronically—typically within one business day.

Step 5: Pay and get instant proof. Make your first payment and immediately receive digital proof of insurance. You can show this to the DMV, your lender, or law enforcement if needed.

The whole process can happen in a single session. No phone tag with agents, no waiting days for callbacks, no repeated rejections.

Here’s what the insurance industry doesn’t want you to know: the key to leaving high-risk status behind isn’t a single policy. It’s a pattern of safe driving habits and on-time payments over several policy terms.

Staying insured without lapses through OCHO for 12-36 months, while avoiding new tickets and accidents, makes you progressively more attractive to both non-standard and eventually standard carriers. Your history starts showing consistency, not chaos.

This is the OCHO difference: we’re not just a one-time quote machine. We’re a long-term partner that helps turn high risk car insurance into a stepping stone back to normal pricing.

You can’t erase past mistakes from your driving history overnight. But you can make choices starting today that steadily reduce your risk profile and premiums.

Core strategies that work:

OCHO can show you in real-time how each strategy affects quotes from different high-risk carriers before you commit to a policy. Want to see how raising your collision deductible from $500 to $1,000 changes your monthly cost? We can show you that across multiple companies instantly.

Some OCHO partner companies offer discounts for:

The single biggest factor in leaving high-risk status is preventing new accidents and tickets. Full stop.

Consider these steps:

Check your motor vehicle record once a year to ensure old violations are removed when state timelines expire. Sometimes errors stay on records longer than they should.

Consistently safe driving over three to five years can transform you from high-risk to standard in most markets—especially when combined with continuous coverage through OCHO.

Here’s something most drivers overlook: continuous coverage is a major rating factor. Insurers value it highly, especially for high-risk drivers trying to rehabilitate their profiles.

Practical advice:

At renewal time, OCHO can shop the market again to find you better quotes, your improved payment history makes you more attractive to carriers.

This is OCHO’s model: helping drivers maintain a string of consecutive policies with specialist carriers so they can eventually graduate from high risk car insurance.

The car you drive and the coverage options you select significantly impact affordability for high-risk policies.

Vehicle recommendations for high-risk drivers:

Coverage balancing tips:

OCHO shows you in real-time how different cars and coverage combinations change quotes from high-risk companies. This lets you pick the mix that best fits your recovery plan and budget.

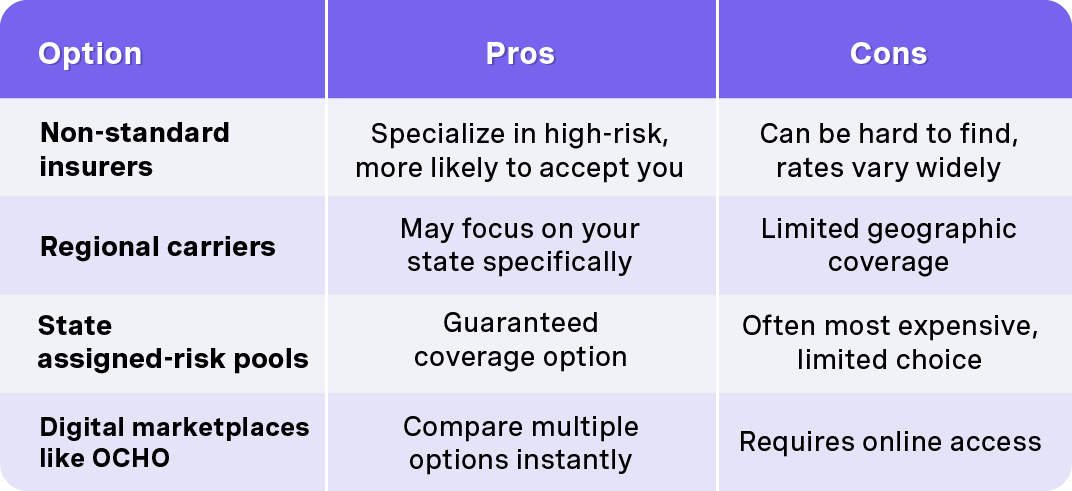

Most large, brand-name insurers focus on standard and preferred drivers. They don’t want customers with DUIs, multiple accidents, or coverage gaps—those drivers hurt their loss ratios. High risk car insurance is typically handled by specialized non-standard companies that most people have never heard of.

Your options include:

Going directly from company to company is time-consuming, especially for drivers with complex histories. You fill out forms, wait for callbacks, get rejected, and start over. It’s exhausting.

OCHO centralizes this process. All our partner companies are comfortable with high-risk profiles, which reduces the frustration of repeated denials or unusable quotes.

If you suspect you’re in the high-risk category, or you’ve already been turned down elsewhere, OCHO should be your first stop.

These questions address common issues that weren’t fully covered above, focused on practical concerns high-risk drivers face every day.

Can I get high risk car insurance if I don’t own a car?

Yes. Non-owner high risk policies are available through OCHO’s partners for drivers who need to file an SR-22 or maintain insurance for license purposes, even without a vehicle. This is common for drivers whose licenses are suspended but who need to show proof of insurance before reinstatement.

Does high risk car insurance cover me to drive for rideshare or delivery apps?

Some high-risk insurers offer endorsements or separate policies for Uber, Lyft, or delivery work—but not all do. Standard personal auto policies typically exclude commercial use.

Will filing an SR-22 through OCHO automatically remove my high-risk status?

No. The SR-22 is only proof of coverage required by the state—it’s not a magic ticket to better rates. High-risk status changes gradually as violations age off your record and you maintain clean, continuous coverage. The SR-22 just keeps you legal while you work toward that goal.

Can I switch from a standard insurer to a high-risk policy with OCHO after a major ticket or DUI?

Absolutely. Many drivers come to OCHO when their standard insurer non-renews them or drastically raises rates after a serious incident. OCHO helps find a high-risk company willing to take you, often the same day.

How soon after an accident or DUI should I shop for high risk car insurance?

Start looking as soon as you know about a suspension, SR-22 requirement, or non-renewal notice. OCHO can often line up coverage to begin the same day your old policy ends or your license becomes eligible for reinstatement. Don’t wait until the last minute—that creates stress and potential coverage gaps.

High risk car insurance doesn’t have to be a permanent sentence. With the right approach: continuous coverage, clean driving, and a partner like OCHO who understands the system, you can work your way back to affordable auto insurance rates.

Ready to see what options are available for your specific situation? Get a quote through OCHO today and start your path back to standard rates.

Compare & get covered fast

Find and compare auto insurance in minutes, and get your free credit score.

Choose when you pay

Select payment dates that line up with your payday.

Manage everything in one place

Track your policy, manage payments, and request a payment extension right from your dashboard.

.svg)