Otto Insurance is a data-driven lead generation site founded in the mid-2010s and based in Miami Beach, Florida. It connects consumers with third party agents and partner insurers but is not an actual insurance company that underwrites policies or handles claims.

Otto does not sell or issue insurance policies directly. Instead, it collects your personal details and vehicle information, then sells those “leads” to 1,000+ partner carriers and insurance agencies—sometimes distributing your data to over 170 entities at once.

Many users report receiving 10–20+ unsolicited phone calls and text messages within hours of filling out Otto’s form. This happens because of broad data sharing and TCPA consent language buried in the fine print.

Otto has a mixed reputation online: a B– to B+ Better Business Bureau rating and largely negative Trustpilot reviews (averaging 1.9–2.4 out of 5), with consumer complaints focused on spam calls and deceptive practices.

If you value privacy or want instant, on-screen quotes without aggressive follow-up, consider alternatives like Insurify, The Zebra, Policygenius, or going directly to traditional insurers like State Farm or GEICO.

What Is Otto Insurance, Really?

Let’s cut to the chase. “Otto Insurance” (sometimes marketed as “OTTO Quotes” or “Otto Auto Insurance”) is not what most people think it is. It’s a digital marketing and lead generation platform, not a licensed insurer. Otto Insurance Group is the business entity operating the platform, and it acts as a lead generation platform that connects consumers with multiple insurance providers, not as an insurance company itself. The company launched around 2015 and operates out of Miami Beach, FL. When you see those ads promising to help you compare quotes and save money on coverage, you’re not dealing with an insurance provider—you’re dealing with a data collection machine.

Otto’s legal role is to capture consumer data and sell it as leads to licensed insurance agents and insurance carriers across the United States. While auto insurance is the primary focus, Otto also routes leads for home insurance, renters coverage, pet insurance, life insurance, and some commercial insurance products.

The website presents itself as an easy quote tool that will help you compare insurance rates in minutes. But here’s what it doesn’t do: Otto cannot provide binding quotes, handle claims, or issue proof of insurance. It’s a middle man, not an insurance company.

All transactions, policy documents, billing, and claims are completed on third-party carrier or agency websites—or by phone with those partners. Otto’s job ends the moment your data leaves their servers.

Public business records and the Otto website show limited transparency on ownership details beyond references to founder Joshua Keller and mentions of a distributed, remote team. If you’re looking for corporate accountability, you won’t find much beyond the Miami Beach address.

Is Otto Insurance Legit or a Scam?

This is the question everyone asks after getting their seventeenth call in two hours. The honest answer? Otto is “legitimate” in the narrow sense that it’s a real, registered business that operates legally. But many consumers experience it as deceptive due to its marketing tactics and aggressive data-sharing practices.

State regulators in places like Florida list no Otto entity as a licensed insurer. That’s because Otto is legally classified as a marketing and lead generation firm—not an insurance carrier that can write policies.

There’s a real contrast between Otto’s official status (a functioning legitimate business that partners with real insurers like Progressive and State Farm) and what you’ll find in otto insurance reviews online. Many people call it a “total scam” because the website overpromises instant quotes and underdelivers actual rates.

Otto’s website fine print typically discloses its lead-gen role and data-sharing practices. But let’s be real—these details are buried compared to the prominent “Get Your Quote Now!” language. Most people don’t read the fine print until it’s too late.

My advice? Treat Otto the same way you’d treat any aggressive lead-capture site. Read the privacy policy and terms carefully before submitting personal information. Assume your data will be sold multiple times to multiple buyers.

Otto Insurance’s Business Model Explained

Understanding otto works requires understanding how lead generation platforms make money. Spoiler: it’s not from premiums, underwriting, or claims handling. It’s from selling your data.

The typical flow looks like this: you complete a form with your personal info → Otto scores and packages that data → Otto distributes it to a network of 170+ carrier and agency partners in real-time.

Partners may pay Otto per validated lead, often in the $50–$200 range for auto insurance shoppers. Some arrangements involve revenue-share or commission structures where Otto gets a cut if you eventually buy a policy.

Because Otto benefits financially from sending your data to as many buyers as possible, your contact details can reach dozens of insurance brokers and call centers almost instantly. That’s why your phone starts ringing before you’ve even closed the browser tab.

The model incentivizes volume—more leads mean more money. This structure prioritizes quantity over a calm, curated streamlined experience for the consumer. Otto’s success metric isn’t your satisfaction; it’s how many times they can monetize your data.

How the Lead Generation Process Works Step by Step

Let us walk you through what actually happens when you use Otto:

You Google something like “cheap car insurance” and land on an Otto website. You see a promising pitch about low car insurance rates and decide to fill out the form. The multi-step process asks for your name, address, vehicle information, driving history, desired coverage options, and those sneaky consent checkboxes.

At the moment you hit submit, Otto’s system pings multiple affiliate platforms. These platforms auction or route your lead in real-time to agents at companies like Progressive, GEICO, Liberty Mutual, or regional insurance carriers. Your data is quite literally being bid on.

You’re often redirected to another comparison site or a single carrier’s website, where—surprise—you frequently have to re-enter many of the same details you just provided. The quote process starts all over again.

In parallel, call centers and independent agents start dialing, emailing, and texting you using the info Otto just sold. This can happen within seconds of form submission.

Otto itself usually disappears from the picture after the form. From that point forward, you’re dealing directly with third-party marketers and licensed producers. If something goes wrong, Otto shrugs and points you to the actual insurers.

How Otto Monetizes Your Information

Your collected data is Otto’s core asset. The more partners they can sell that data to, the more revenue they generate. It’s really that simple.

A single auto insurance lead might be sold to several buyers within seconds via a bid/auction system. Each buyer pays for the “right” to contact you—and they all exercise that right, often simultaneously.

The information shared includes contact details, vehicle info, location data, and inferred risk factors. All of this can later influence the insurance quotes you receive and what marketing offers flood your inbox.

The consent language in Otto’s forms often authorizes calls even to numbers on the National Do Not Call Registry. How? Because by submitting the form, you’re technically “requesting information” and opting in to be contacted by partner insurers.

Here’s the uncomfortable truth: once your data is widely distributed, Otto cannot realistically pull it back from every downstream buyer. Even if you later ask Otto to delete your record, your information may already be living in dozens of CRM systems and dialer queues.

What Otto Insurance Actually Offers (Types of Coverage)

Let’s be clear about something: Otto’s “products” are quote matches, not actual insurance policies. Otto insurance offers connections to several insurance categories, but the coverage terms always come from partner insurers.

Auto Insurance: This is Otto’s bread and butter. Through partner carriers, you might find liability coverage, collision, comprehensive, uninsured/underinsured motorist protection, and extras like roadside assistance or rental reimbursement. But otto auto insurance doesn’t exist—you’re buying from whoever Otto connects users with.

Home and Renters Insurance: Otto also routes leads for property coverage, including dwelling protection, personal property, liability, and loss-of-use coverages. These policies come from traditional home insurers, not Otto.

Life Insurance: Otto generates leads for term life, whole life, and possibly universal life policies. These connect shoppers with life insurers and insurance brokers who handle the actual underwriting and medical checks.

Pet Insurance: If you’re looking for accident-only, accident + illness, or wellness add-ons for your furry friend, Otto can route your lead to third-party pet insurers. Again, Otto doesn’t provide insurance—it provides introductions.

Because Otto is not a carrier, there’s no standardized coverage menu. Everything depends entirely on whichever insurer ultimately sells you a policy. Otto connects consumers to options but controls nothing about those options.

Otto vs. Real Insurance Companies

This comparison matters because many people don’t realize the difference until they’re drowning in spam calls.

Real insurance carriers file rates with state regulators, issue policies in their own name, and pay claims when you need them. Otto does none of these things.

Policy servicing—billing, endorsements, cancellations—is entirely handled by the insurer or agent you end up choosing. Otto cannot help you change your deductible or file a claim.

With direct carrier websites, you usually see actual rates on screen immediately. With Otto, you mostly trigger follow-up outreach rather than instant pricing. The “verification successful waiting” message often just means your data is being distributed.

If you already know which insurer you prefer, going directly to that carrier’s website or a local agent is usually more efficient. You’ll skip the middle man and avoid the data privacy concerns.

Insurance Agents and Partners: Who’s Really Behind Your Quote?

When you use Otto Insurance, you’re not just interacting with a single insurance company—instead, you’re entering a network of insurance agents and partner companies ready to compete for your business. Otto’s lead generation service is designed to connect consumers with licensed insurance agents who can provide a variety of car insurance quotes from different insurance carriers. After you submit your information, expect to receive phone calls and emails from several insurance agents and brokers, each representing their own insurance company. These agents are there to answer your questions, walk you through coverage options, and help you secure a policy that fits your needs.

Otto partners with a wide range of companies, including major names like State Farm, Progressive, and GEICO, as well as regional insurers. This broad network allows Otto to offer a streamlined experience, giving you access to competitive insurance rates from multiple sources with just one form submission. However, it’s important to remember that Otto itself is not an actual insurance company—it simply connects consumers to the companies and agents who provide insurance. The result is a fast, if sometimes overwhelming, way to compare insurance quotes and find coverage, but it also means you’ll be dealing directly with the insurance agents and companies who reach out to you, not Otto.

State Availability and Operations: Where Does Otto Work?

Otto Insurance’s lead generation platform is available in many states across the U.S., but the specific insurance products and partner insurers you’ll see depend on your location. When you enter your zip code on the Otto website, the platform matches you with insurance providers that are licensed to operate in your state. This means that while Otto’s services are broadly accessible, the actual insurance options and companies you’re connected with will vary based on where you live.

It’s important to note that Otto is not a licensed insurance company and does not directly provide insurance products. Instead, Otto acts as a connector, linking you to partner insurers who can offer you quotes and policies tailored to your state’s requirements. If you’re unsure whether Otto’s services are available in your area or want to know more about the insurance products offered, you can reach out to their customer support team for clarification. Ultimately, Otto’s role is to facilitate your insurance shopping experience by connecting you with insurers and services that fit your location and needs.

Costs and Fees: What You Might Pay (and When)

One of the appealing aspects of using Otto Insurance is that the platform itself is free—there are no upfront costs for comparing insurance quotes or connecting with insurance agents. You won’t pay Otto anything for using their lead generation service. However, when you decide to purchase a policy through one of Otto’s partner carriers, you’ll pay your insurance premium directly to the insurance company you choose. The price of your policy will depend on several factors, including your location, the type of vehicle you drive, your driving history, and the coverage options you select. You might also consider alternative providers that offer affordable car insurance with flexible payment options.

Some insurance companies may offer additional services, such as roadside assistance or rental car coverage, which could come with extra fees. It’s always a good idea to review your policy documents carefully and ask your insurance agent about any potential costs before finalizing your purchase. While Otto may receive a commission or referral fee from the insurance company for connecting you as a customer, this does not affect the price you pay for your coverage. The focus should always be on understanding your policy and making sure it fits your needs and budget.

Claims and Support: What Happens If You Need Help?

If you ever need to file a claim or require assistance with your insurance policy, your main point of contact will be the insurance company that issued your policy—not Otto. As a lead generation platform, Otto’s role ends once you’re connected with an insurer or agent. After purchasing a policy, you’ll receive contact information for your insurance company’s claims department and customer support team. These are the people who can help you file a claim, answer questions about your coverage, or provide support services like roadside assistance.

Many insurance companies now offer convenient support options, such as 24/7 claims hotlines, online claim filing, and mobile apps for managing your policy. If you’re unsure who to contact, refer to your policy documents or the welcome materials provided by your insurer. Remember, Otto does not handle claims or provide direct support services, but the insurance companies you connect with through the platform are equipped to help you with any issues that arise.

Cancellation and Refund Policies: Can You Change Your Mind?

If you decide to cancel your insurance policy after purchasing through an Otto partner, you’ll need to work directly with the insurance company that issued your policy. Each insurance company has its own cancellation and refund policies, which may include a cancellation fee or require a certain notice period. In some cases, you may be eligible for a refund of any unused premiums, but this will depend on the company’s specific rules and applicable laws in your state.

Before buying a policy, it’s wise to review the cancellation and refund terms outlined in your policy documents and ask your insurance agent any questions you may have. If you’re dissatisfied with your experience—whether with the insurance company or with Otto’s business practices—you can file a complaint with the Better Business Bureau or your state’s insurance department. These organizations can help mediate disputes and ensure that companies are following fair business practices. Ultimately, understanding your rights and the fine print can help you avoid surprises if you ever need to change or cancel your coverage.

User feedback on Otto from 2024–2026 is heavily polarized, and it skews negative. The main themes? Spam and transparency issues.

The Better Business Bureau lists Otto as not accredited, with a B– or B+ rating depending on when you check. The rating reflects a growing number of complaints about business practices and unwanted phone calls.

Trustpilot ratings hover around 1.9–2.4 out of 5. Roughly 70%+ of reviews give one star, citing misleading advertising and relentless follow-ups from insurance agents they never asked to hear from.

Reddit threads and forum posts are particularly illuminating. Users report receiving 10–17 calls within a couple of hours after submitting the Otto form, often from different insurance agencies using several factors to personalize their pitch.

To be fair, there are some positive experiences. A minority of reviewers managed to save money on auto or home coverage and appreciated having multiple agents compete for their business. But these voices are outnumbered by the frustrated majority.

Common Complaints About Otto Insurance

Certain themes appear repeatedly across BBB complaints, Trustpilot reviews, Reddit discussions, and consumer review sites. Let me break them down:

Spam Communications: This is complaint number one. Users describe receiving numerous calls, text messages, and emails from carriers and independent agents—often beginning within minutes of form submission. Some report their phone number being called 20+ times in a single day.

Misleading Branding: Many consumers feel the name “Otto Insurance” falsely implies they’re dealing with a real insurance company. They expect to get insurance quotes from Otto, not to have their data sold to whoever pays the highest bid.

No Actual Quotes: Users frequently express frustration at never seeing an actual on-screen quote from Otto itself. Instead, they’re redirected to other sites or asked to talk to agents on the phone. The promised “compare quotes” experience never materializes.

Difficulty Opting Out: People report having to block dozens of phone numbers, send multiple emails, and still receive calls weeks later. The data, once distributed, is nearly impossible to recall.

Bait-and-Switch Rates: Some reviewers felt they were promised unrealistically low teaser rates that were never honored by the carriers they were passed to. The potential customers who respond to “save 40%!” ads often discover the actual rates are much higher.

Positive Experiences and When Otto Might Help

Not everyone hates Otto. Some users report genuine value from the service—though they’re definitely in the minority.

Shoppers with time to field calls and text messages have used Otto to receive multiple competing auto quotes in a single afternoon. They then leveraged those offers to negotiate better deals with their preferred carrier.

Users in high-premium states like Florida have appreciated access to alternative carriers during difficult market conditions when traditional insurers were limiting new policies.

Occasionally, reviews praise specific agents by name (like “Ray I was so helpful!”)—though these agents work for partner agencies, not Otto itself. The client communication experience varies wildly depending on which agent happens to call first.

Bottom line: Otto may be beneficial for people who are comfortable trading privacy for aggressive outreach and a high volume of quote offers. If that sounds like you, it might work. If that sounds like a nightmare, steer clear.

Privacy & Data Sharing: What Happens to Your Info?

The major concern with Otto isn’t just marketing annoyance—it’s long-term data privacy and control. When you submit your information to a lead generation site, you’re giving up more than you might realize.

Otto’s privacy policy typically allows the company to share your information with “affiliates, marketing partners, and service providers.” This category can include dozens or hundreds of entities you’ve never heard of.

Data shared may include personal identifiers (name, phone number, email, birth date), vehicle details, driving history, IP address, approximate location, and browsing behavior on the Otto website. All of this becomes a profile that’s packaged and sold.

Once your data reaches 170+ partners, it can be copied into their CRMs, dialer systems, and retargeting platforms. At that point, it’s beyond Otto’s direct control—even if Otto wanted to help you, they couldn’t.

Even if you later submit a deletion or “do not sell” request to Otto under applicable laws like CCPA, some downstream companies may retain your record for their own legal or marketing reasons. Your personal info takes on a life of its own.

How to Reduce Unwanted Calls if You Used Otto

If you’ve already submitted your information and you’re dealing with the aftermath, here’s what you can do:

Send a clear written request to Otto’s published support email or contact form. Ask them to delete your data and stop selling or sharing it. Include your name, email, and phone number so they can locate your record.

Register or confirm your number on the National Do Not Call Registry (donotcall.gov). This won’t stop all calls—your prior consent may still authorize some—but it should reduce future unrelated solicitations.

Use your phone’s built-in call-blocking features and third-party spam-filter apps to block recurring caller IDs from insurance agencies that continue to contact you.

If calls continue at an abusive level, document the dates and times. You may file complaints with the FTC, FCC, or your state insurance regulator about specific agencies’ telemarketing practices.

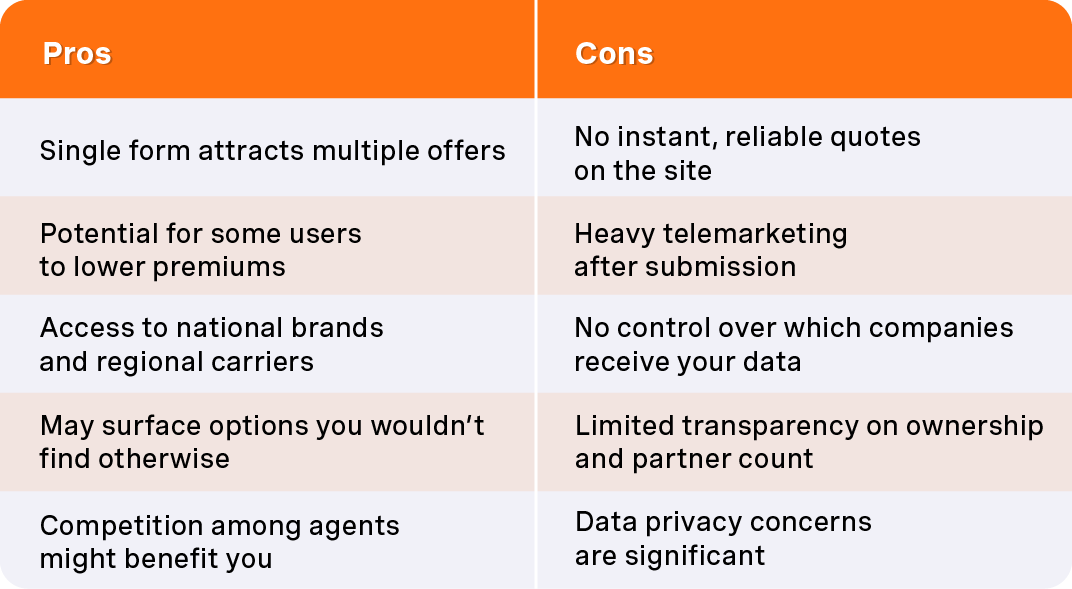

Pros and Cons of Using Otto Insurance

Otto has clear trade-offs. Here’s an honest assessment:

People comfortable with being contacted heavily and fielding multiple offers may find Otto acceptable. The aggressive approach can work in your favor if you’re a skilled negotiator.

Privacy-conscious or time-pressed shoppers should avoid Otto entirely. The services offered don’t justify the data sharing for most consumers.

Better Alternatives to Otto Insurance

If you want to compare quotes without the worst downsides of lead-gen platforms, you have options. Here’s practical guidance:

OCHO: Not to toot our own horn too much, but if you're looking for low downpayment auto insurance, with flexible payments, payment extensions when you need it - look no further than OCHO! We are a human-centered car insurance agency, here to help you out.

Comparison Sites with Real-Time Quotes: Insurify, The Zebra, Compare.com, and NerdWallet typically show actual insurance quotes on-screen without immediately selling your data to dozens of partners. Their privacy practices are generally clearer than Otto’s.

Policygenius: For life insurance, home insurance, or disability coverage, Policygenius offers guided, broker-style advice with fewer random phone calls. They work more like a traditional broker than a lead auction.

Direct Carrier Websites: Going directly to trusted car insurance companies like State Farm, GEICO, Progressive, Amica, or Travelers provides accurate, immediate pricing with predictable follow-up. You know exactly who has your data.

Local Independent Agents: A reputable independent agent can shop multiple carriers for you while maintaining a single point of contact. This gives you the comparison benefit without the spam.

Before choosing any policy, check insurer financial strength (AM Best ratings), complaint ratios (NAIC data), and customer satisfaction scores (J.D. Power). These matter more than which website gave you the quote.

How to Safely Shop for Insurance Online

Here’s actionable advice for consumers comparing auto or home insurance in 2025–2026:

Create a dedicated email address and possibly a secondary phone number (Google Voice or another VoIP service) specifically for quote forms. This protects your primary contact channels from spam.

Before clicking “submit” on any insurance shopping site, skim the privacy policy and terms. Look for phrases like “we may sell or share your information with marketing partners.” If you see that, proceed with caution.

Prioritize sites that display multiple carrier prices instantly, on screen. If a site only promises that “an agent will contact you,” expect the lead generation service treatment.

Keep a simple spreadsheet of insurance quotes, coverage options, deductibles, and available discounts. This lets you compare offers objectively without relying on any one platform’s messaging.

Once you find a good quote, you can often bypass the original lead-gen path and finalize coverage directly on the insurer’s own website or with a single trusted agent. Cut out the middle man when possible.

FAQs About Otto Insurance

Q: Is Otto Insurance an actual insurance company that can pay my claims?

A: No. Otto is not a carrier or claims administrator. All claims must go through the insurer that issued your policy—companies like Progressive, GEICO, or a local agency. Otto cannot process claims, issue payments, or even access your policy details after you’ve purchased coverage.

Q: Can I use Otto Insurance if I live outside the United States?

A: Otto’s lead-gen services and partner network are primarily targeted to U.S. residents. If you’re in Canada, the U.K., the EU, or other regions, you generally won’t be matched with carriers and should use local comparison tools instead.

Q: How can I tell which company Otto sent my information to?

A: There’s usually no single answer because your lead can be sold to multiple buyers simultaneously. The best clues are the caller IDs that contact you, the email domains in your inbox, and the first carrier website you were redirected to after form submission. Keep notes on who reaches out—that’s your data trail.

Q: Can Otto Insurance help me change or cancel a policy I bought through one of its partners?

A: No. Policy changes and cancellations must be handled directly with the insurer or agent who wrote the policy. Otto cannot adjust premiums, coverage limits, or billing dates. Once you’ve purchased a policy, your relationship is with the carrier, not Otto.

Q: Is it safe to provide my Social Security number on sites like Otto?

A: I’d strongly recommend against it. Avoid entering SSNs or highly sensitive data on broad lead-gen platforms. Only provide such information directly to a reputable carrier or licensed agent after verifying their identity and confirming they actually need it for underwriting purposes.

Get the OCHO app now!

Compare & get covered fast

Find and compare auto insurance in minutes, and get your free credit score.

Choose when you pay

Select payment dates that line up with your payday.

Manage everything in one place

Track your policy, manage payments, and request a payment extension right from your dashboard.

Finally, car insurance you can afford.

Start your OCHO journey today.

Thank you! Your submission has been received!

Oops! Something went wrong while submitting the form. Please try again later.

.svg)