If you’re searching for pay as you go car insurance no deposit options, you’ve come to the right place.

The reason why you’ve probably heard that no deposit car insurance doesn’t exist from legitimate insurance companies is because we are the first company to offer it.

We saw that the insurance industry is incredibly unfair toward those who live paycheck to paycheck, and so we decided to do something about it. We finance your downpayment so you can afford your insurance straight away. We do this interest-free.

There are other companies who talk about no deposit car insurance in a misleading way, but rest assured that is not OCHO. You can check our reviews page and see how many happy customers we have helped already.

It is helpful to understand the differences between different types of pay as you go car insurance, as it isn’t a regulated term. Let’s dig in.

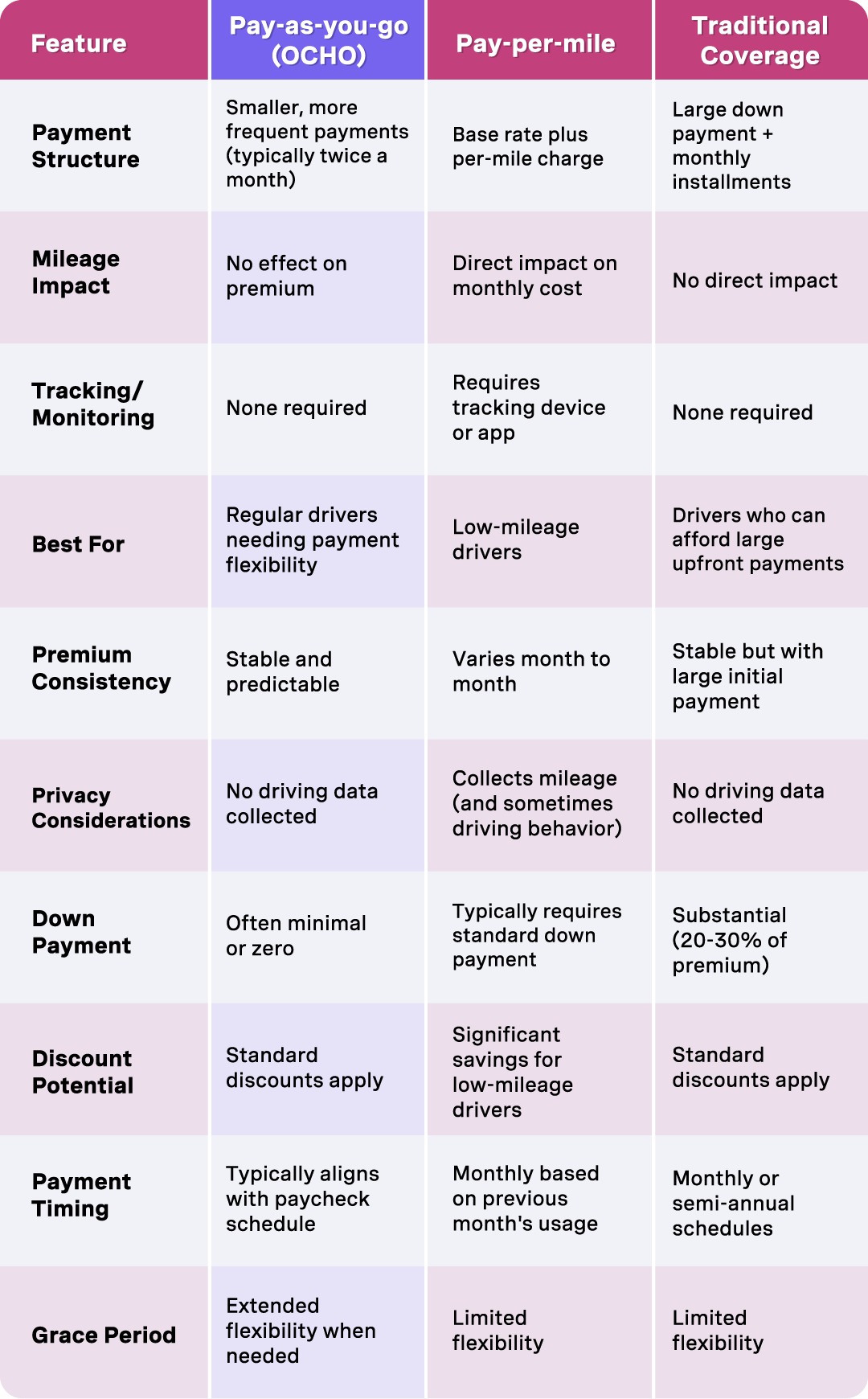

Pay as you go car insurance represents a fundamental shift from traditional annual policies to more flexible models. These can be usage based, micro-payments or like OCHO, steady pay as you go payments with no deposit, aligned to your paycheck.

The first month’s premium for pay-as-you-go policies ranges from $43 to $150 depending on your coverage level, driving history, and chosen provider. This upfront payment isn’t technically a separate deposit but rather represents your first monthly premium payment. Most insurers structure this as a down payment that counts toward your total policy cost rather than an additional fee on top of your premium.

However, with OCHO, our car insurance starts at $0. Some of our customers pay nothing, but everyone will get a much lower down payment.

If the company advertising instant coverage with no money down, “zero down” or “no initial payment” offers and it isn’t OCHO, it is likely to be a scam or misleading. These promotions typically mean one of three things: the insurer offers a grace period (usually 10-30 days) before requiring payment, they provide financing options to spread the initial cost, or they simply charge the first month’s premium rather than requiring multiple months upfront.

Pay-as-you-go models particularly benefit drivers on a low income, students, gig workers and anyone living paycheck to paycheck who needs to minimize large upfront costs. Let’s take more of an in-depth look at the different options available.

Usage-based insurance is where your premium directly correlates to how much and how safely you drive. These programs use telematics devices plugged into your vehicle’s diagnostic port or smartphone apps to monitor factors like mileage, speed, braking patterns, and time of day you drive. Drivers who demonstrate safe behaviors can save 15-30% on their premiums compared to traditional policies.

Progressive’s Snapshot program pioneered this approach, offering discounts based on driving data collected over an initial monitoring period. State Farm’s Drive Safe & Save program provides similar benefits, with potential savings increasing over time as you demonstrate consistently safe driving habits. These programs typically require the standard first payment but often offer lower base rates that reduce your initial financial commitment.

Cons: you will be handing over a lot of data on how you drive, some people aren’t comfortable with this due to privacy reasons, but it can also cause your insurance costs to increase if you drive a lot or brake heavily when driving.

Pay-per-mile insurance charges a low base monthly rate plus a per-mile fee for each mile driven, making it ideal for drivers who travel less than 10,000 miles annually. Companies like Metromile and Mile Auto have built entire business models around this concept, with some customers paying as little as $30-50 per month for basic coverage when they drive minimal distances.

This model particularly benefits remote workers, retirees, urban dwellers who rely on public transportation, and anyone whose vehicle serves as backup rather than primary transportation. The savings can reach 30-40% compared to traditional annual policies for truly low-mileage drivers, though high-mileage drivers may find these plans more expensive than conventional coverage.

Traditional insurance companies increasingly offer monthly payment plans that spread annual premiums across twelve installments rather than requiring large lump sum payments. While these aren’t technically “pay-as-you-go” in the usage-based sense, they provide payment flexibility that makes coverage more accessible for drivers managing tight budgets.

Most insurers charge convenience fees ranging from $3-8 per month for monthly payment plans, but auto-pay discounts often offset these costs. Companies like GEICO, State Farm, and Allstate provide online account management that makes monthly payments seamless and reduces administrative overhead.

OCHO Pay As You Go Car Insurance with No Deposit is built for real life—not just short bursts of coverage. With OCHO, you can start your policy with $0 down and pay for your insurance in smaller, manageable installments that line up with your payday. There’s no turning coverage on and off, no surprise lapses, and no gaps that could get you in trouble with the DMV. Instead, OCHO gives you reliable, everyday protection with flexible payments and access to full-coverage options, something most pay-as-you-go companies don’t offer. It’s the no-deposit, budget-friendly way to stay insured consistently while still getting the level of coverage you actually need.

While Hugo is one of the most well-known names in the pay-as-you-go, no-deposit car insurance space, their model works best only for very short-term or occasional drivers. Hugo lets you buy coverage in small increments — sometimes just a few days at a time — and skip the traditional down payment. But the tradeoff is that their policies usually provide only state-minimum liability coverage and come with strict limitations. Drivers looking for consistent, long-term protection often find that Hugo’s turn-on/turn-off structure creates gaps in coverage, DMV complications, and unexpected costs. For people who need reliable everyday insurance with real protection, a pay-as-you-go option that offers broader coverage and steady, affordable payments tends to be a better fit.

GEICO consistently offers the most affordable monthly premiums for minimum coverage, averaging $43 per month across fifteen states according to recent analysis. This translates to the lowest possible first payment for drivers seeking to minimize upfront costs while maintaining legal compliance. GEICO’s streamlined online application process allows for same-day coverage activation with immediate payment via credit card or electronic bank transfer.

The company’s competitive pricing stems from their direct-to-consumer model that eliminates agent commissions and reduces overhead costs. GEICO also provides multiple payment options including autopay discounts that reduce monthly premiums by 3-5%, effectively lowering both ongoing costs and the required initial payment amount.

Travelers offers competitive rates in northeastern states, with monthly minimums averaging $48-52 depending on location and driving history. The company provides flexible payment schedules and often waives processing fees for electronic payments, making them attractive for budget-conscious drivers in their coverage areas.

Erie Insurance serves customers in thirteen states with monthly premiums starting around $46 for minimum coverage. Erie’s local agent network provides personalized service while maintaining competitive pricing, particularly for drivers with good credit history and clean driving records.

State Farm maintains strong regional pricing in many markets, offering monthly plans starting at $50-55 with extensive discount opportunities. Their broad agent network and comprehensive customer service make them accessible for drivers who prefer in-person assistance with their coverage decisions.

Moving from minimum to full coverage dramatically increases both monthly premiums and required initial payments. The same GEICO policy that costs $43 monthly for minimum coverage might cost $120-180 monthly for comprehensive and collision protection, depending on your vehicle’s value and chosen deductible levels.

However, full coverage becomes more cost-effective when financed through monthly payments rather than annual lump sums. A $1,440 annual premium becomes manageable as twelve $120 monthly installments, though convenience fees typically add $36-96 annually to the total cost.

OCHO makes pay-as-you-go, no-deposit car insurance simple. Instead of the large upfront costs most insurers require, OCHO spreads your premium into smaller, predictable payments that match your budget and your payday. That means you can stay insured without sacrificing essentials like rent or groceries — real coverage that actually fits real life.

Our payment plans vary by state, but the goal never changes: make starting and keeping coverage as affordable and stress-free as possible. The table below breaks down how OCHO’s payment structure works across the states we serve, including:

Use this as a quick guide to understand how OCHO keeps pay-as-you-go insurance accessible, consistent, and budget-friendly — without the coverage gaps or surprises you get with other providers.

[table]

Using a credit card to pay for car insurance can create a short-term buffer, because you’re essentially getting up to 30 days before the charge hits your bank account. Your coverage activates immediately, but the money doesn’t leave your account until your credit card bill is due. For drivers who are paid monthly, this can help smooth out cash flow and make that first payment feel more manageable.

Most major insurers accept credit cards without extra fees, though some smaller carriers may add a 2–3% processing charge that reduces the benefit. Credit cards also offer fraud protection and can contribute to building credit if payments are made on time.

That said, OCHO doesn’t recommend relying on this strategy. It’s easy for a “one-time workaround” to snowball into revolving debt, leaving you in a worse financial position than where you started. Instead of pushing customers toward credit card balances, OCHO focuses on payment plans that keep coverage affordable without adding risk to your budget.

Some insurers provide grace periods ranging from 10-30 days for first payments, allowing customers to secure coverage immediately while providing time to arrange payment. These grace periods aren’t true “no deposit” coverage but rather deferred payment arrangements that maintain legal compliance while providing financial flexibility. You are unlikely to get this grace period if you are a high-risk customer, but you can with OCHO.

State regulations typically require insurers to provide minimum grace periods for initial payments, though specific timeframes vary by location. Understanding your state’s requirements helps you maximize available time while ensuring continuous coverage and avoiding potential legal complications from driving uninsured.

Setting up automatic payments can reduce monthly premiums by 3-10% with most major insurers, effectively lowering both ongoing costs and the required initial payment amount. These discounts compound over time, potentially saving hundreds of dollars annually while simplifying payment management.

Auto-pay arrangements also reduce the risk of missed payments that could result in coverage lapses or additional fees. Most insurers allow customers to choose payment dates that align with paycheck schedules, improving cash flow management for drivers living paycheck to paycheck.

OCHO is the ONLY place where you can start your car insurance with zero down payment. That’s because we finance your downpayment (interest-free) for you. Instead of paying hundreds of dollars upfront, you spread that cost into small, manageable payments that line up with your paycheck. There’s no credit check, no hidden fees, and no tricks — just a simple way to get insured today without draining your bank account. It’s a real alternative for drivers who need coverage now but can’t afford the impossible deposits most insurers require.

Combining auto insurance with renters or homeowners coverage often provides discounts ranging from 5-25% on total premiums, reducing both monthly costs and initial payment requirements. Insurance companies prefer customers who purchase multiple policies because it increases customer retention and reduces marketing costs, savings they pass along through bundling discounts.

Young drivers and college students can often bundle with parents’ existing policies to achieve significant savings, even when maintaining separate coverage for their own vehicles. This strategy requires coordination but can dramatically reduce the cost of getting covered when starting independent insurance coverage.

Completing defensive driving courses can reduce premiums by 5-15% in most states, with some insurers offering additional discounts for advanced safety training. These courses typically cost $25-75 but can save hundreds annually on insurance premiums, making them highly cost-effective investments for budget-conscious drivers.

Good student discounts benefit drivers under 25 who maintain B+ averages or higher, with savings often reaching 10-25% of total premiums. Military personnel, government employees, and members of certain professional organizations may qualify for additional occupational discounts that further reduce coverage costs.

Drivers who travel less than 7,500 miles annually often qualify for low-mileage discounts that reduce premiums by 5-20% depending on the insurer and actual miles driven. These discounts stack with other available savings and can significantly impact both monthly costs and required upfront payments.

Safe driver programs reward customers with accident-free and violation-free driving records through premium reductions that increase over time. Maintaining clean driving records becomes increasingly valuable as these discounts can reach 20-30% after several years of safe driving with the same insurer.

Monthly payment plans transform potentially unaffordable annual premiums into manageable monthly obligations. A $1,200 annual policy becomes twelve $100 monthly payments (plus convenience fees), making coverage accessible for drivers who cannot pay large lump sums upfront.

These plans improve cash flow management and allow drivers to align insurance payments with their income cycles. The convenience fees typically range from $3-8 monthly, adding $36-96 annually to total costs, but this expense often proves worthwhile for drivers who would otherwise struggle to afford coverage.

Automatic payment options for monthly plans often qualify for additional discounts that partially or completely offset convenience fees. Most insurers provide online account management that makes payment tracking and plan modifications simple and accessible.

Let’s be real: micropayment pay-as-you-go insurance like Hugo insurance can be a gamble. It sounds flexible, but there are hidden costs. Here’s why:

1. Frequent Lapses in Coverage: Policies cancel without warning, leaving you exposed to financial and legal risks.

2. Unpredictable Premium Hikes: Rates can increase unexpectedly, making budgeting difficult.

3. Missed Discounts: Without continuous coverage, you lose out on savings tied to being “currently insured.”

4. Credit Damage: Missed payments or policy cancellations can hurt your credit score, affecting your ability to secure affordable insurance in the future.

OCHO is here to rewrite the rules. We prioritize consistent, reliable coverage with no surprises, helping you avoid the cascading consequences of temporary setbacks.

Whether you need basic auto coverage or full coverage car insurance, OCHO's pay-as-you-go model offers:

💰 No Coverage Gaps: OCHO’s policies stay active, so you’re always protected, even during tough times.

💰 Smaller Payments, Every Two Weeks: Avoid the stress of lump-sum premiums with manageable, predictable payments that sync with your pay day.

💰 Path to Lower Rates: Insurance companies penalize drivers with lapses in coverage by categorizing them as high-risk, leading to inflated premiums. OCHO helps you break free from this cycle by keeping you consistently covered. After 12 months of uninterrupted coverage, you can graduate out of the high-risk category, unlocking access to better premiums and long-term savings—an industry secret designed to keep people with limited resources stuck in higher-cost plans.

It’s not just about staying insured today—it’s about creating a better future for your finances.

Successful applications for affordable coverage begin with gathering required documentation including driver’s license, vehicle registration, and previous insurance records. Having this information readily available streamlines the application process and enables same-day coverage activation when needed.

Credit history information becomes particularly important for securing low initial payment requirements, as insurers use credit scores to assess risk and determine down payment amounts. Drivers with excellent credit may qualify for reduced down payment options, while those with bad credit might face higher upfront requirements.

Comparing quotes from multiple insurers ensures you find the lowest possible monthly premium, which directly translates to the smallest required initial payment. Online comparison tools allow rapid evaluation of different coverage options and payment structures without committing to any particular provider.

The most effective approach involves requesting quotes for identical coverage levels from at least three different companies, then comparing both monthly costs and down payment requirements. This process often reveals significant price differences that can save hundreds of dollars annually while minimizing upfront financial commitments.

If you use OCHO, we will not only help you compare first quotes, we will help you compare final quotes, too! This means you know you are always getting our best price.

Many insurance agents possess flexibility to adjust payment timing within company guidelines, particularly for customers with good driving records or credit history. Discussing your specific financial situation and payment preferences during the application process may reveal options not immediately apparent through online applications.

Some insurers allow customers to schedule their first payment for specific dates that align with paycheck schedules or other financial commitments. This coordination helps ensure successful payment processing while providing time to arrange necessary funds without rushing into coverage decisions.

Most major insurers provide immediate coverage activation for customers who complete applications and submit payments during business hours. Electronic payment methods enable instant processing, while paper checks typically require 3-5 business days to clear before coverage becomes effective.

Understanding the distinction between coverage binding and payment clearing helps avoid confusion about when protection actually begins. Coverage typically binds immediately upon payment authorization, even if funds haven’t yet transferred from your account, providing legal protection while payment processing completes.

Can I really get car insurance with absolutely no money down?

Yes! Only at OCHO.

What happens if I miss my first insurance payment during the grace period?

Most insurers provide 10-30 day grace periods for initial payments, but coverage terminates immediately if payment isn’t received within this window. Driving without valid insurance violates state laws and can result in fines, license suspension, and personal liability for accidents. Contact your insurer immediately if you anticipate payment difficulties to discuss possible extensions or payment arrangements.

Is pay-per-mile insurance worth it for occasional drivers?

Yes, drivers who travel less than 10,000 miles annually typically save 30-40% with pay-per-mile insurance compared to traditional policies. This model particularly benefits remote workers, retirees, urban residents who use public transportation, and anyone whose vehicle serves as backup transportation rather than daily commuting. However, frequent drivers may find pay-per-mile options more expensive than conventional coverage.

Can I switch from annual to monthly payments mid-policy?

Most insurers allow payment plan changes during active policies through online portals or customer service, though some charge administrative fees ranging from $25-50 for mid-term modifications. The switch typically takes effect at your next payment due date, and any refunds for prepaid coverage are processed according to company policy.

Does using a credit card for insurance payments affect my credit score?

Paying for insurance with a credit card won’t directly affect your credit score as long as you pay your card on time and avoid carrying a balance. On-time payments can even help strengthen your credit history over time. The main advantage is that it lets you delay out-of-pocket costs for up to 30 days while keeping your coverage active—essentially an interest-free short-term loan.

That said, we don’t recommend relying on this method. Large payments can become difficult to manage if unexpected expenses come up, potentially putting you in a worse financial position than before. OCHO’s flexible payment plans offer a safer, more manageable way to stay insured without relying on credit card timing.

Compare & get covered fast

Find and compare auto insurance in minutes, and get your free credit score.

Choose when you pay

Select payment dates that line up with your payday.

Manage everything in one place

Track your policy, manage payments, and request a payment extension right from your dashboard.

.svg)