Car insurance isn't just some legal box to tick, it's your lifeline when the road throws you a curveball. Whether you're dealing with a fender bender or staring down major damage, having the right payment car insurance policy can save you from financial disaster.

But here's the thing: with all those payment plans and coverage options flooding the market, finding affordable coverage that actually fits your budget? The Old Timers in this industry have made it ridiculously overwhelming on purpose.

That's where OCHO low or zero down payment car insurance comes in to beat the system. For drivers who need to get insured fast but don't have deep pockets, $20 down payment car insurance is your way to flip the script and activate coverage without breaking the bank.

This type of payment car insurance? It's a game-changer, especially if you're caught between paychecks or just bought a car and need to hit the road now.

By choosing a 20 down payment car policy, you're securing the protection you deserve without getting slammed with some massive upfront cost, making it easier to manage your finances and stay legal behind the wheel while giving the finger to those greedy insurance giants who think you should pay through the nose just to get started.

Let’s cut through the noise: for most insurance companies, $20 down payment car insurance is shorthand for “very low initial payment,” not a standard price you’ll see everywhere. It’s a promotional number that catches your attention, but it’s not what most drivers actually pay.

Here’s what’s really happening when you see those ads. The “down payment” on car insurance isn’t an extra fee or deposit—it’s simply the first chunk of your total 6- or 12-month premium. When an insurer says “from $20 down,” they mean the absolute lowest initial payment someone somewhere qualified for. That someone probably isn’t you. The initial payment also acts as a financial commitment, showing the insurer that you are committed to maintaining coverage, which helps reduce their risk and prevent fraud.

In most states and with most insurers, you must pay at least the first month’s premium before coverage starts. Even when the fine print says “from $20 down,” your actual amount due today will depend on your driving history, credit report, vehicle, location, and chosen coverage levels. Payment amounts can vary significantly based on factors like your credit score, the type of coverage you select, and whether you meet certain qualifying criteria.

Here’s a concrete example: a driver in Ohio or Texas with minimum coverage, a clean driving record, and an older sedan might genuinely see an initial payment near $20–$40 with certain online-only carriers. That’s the best-case scenario.

Now here’s reality for everyone else: drivers in high-cost states like Florida, Michigan, New York, and Louisiana are very unlikely to see $20 down unless they qualify for heavy discounts and bare-minimum coverage. In these markets, expect initial costs of $100–$300 or more, even with a spotless record.

OCHO, of course! We are the ONLY place where you can get genuine very cheap car insurance, no deposit. If we can’t offer our customers zero dollars down, we will get it as low as possible for you, sometimes $20 deposit.

We are able to give you such a low deposit because we finance your downpayment (at zero interest). It doesn’t mean that your insurance is free, just that you don’t have a massive upfront cost. So you can spread the cost of your insurance over the length of the policy, much more manageable that way, right?

For regular insurance companies (not OCHO):

Only a narrow slice of drivers qualifies for extremely low deposits like $20. We’re talking about low-risk profiles buying minimum coverage in affordable insurance markets. If you don’t fit that description, adjust your expectations now.

If you're interested in learning more about instant car insurance and how to qualify, check out our comprehensive guide.

Here are the key traits of likely qualifiers:

Example profile that might actually get $20 down: A 30-year-old driver in Indiana with state-minimum liability, 8,000 miles per year, and a 2016 Camry obtaining a quote in March 2026 and seeing ~$20–$35 due today with a national direct writer.

Who won’t see $20 down? Young drivers under 25, anyone with recent DUIs, SR-22 requirements, and brand-new financed vehicles. Lenders and insurance providers require fuller protection and higher initial payments for these situations. If you need full coverage auto insurance because of a car loan, $20 down is almost certainly off the table.

For OCHO:

Everyone qualifies for a lower downpayment with us. How low depends person to person, but we promise we will make it much more affordable for you.

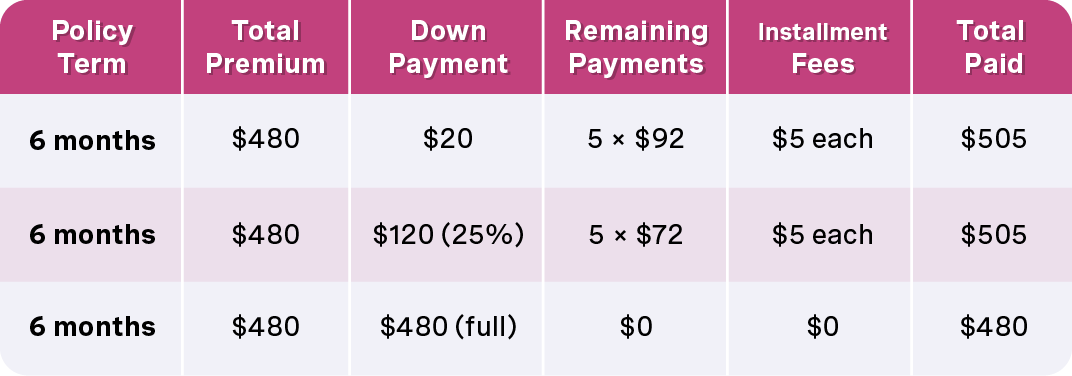

Auto insurance is typically structured over 6- or 12-month terms, with an initial payment followed by monthly installments. The total premium is the same whether you pay it all upfront or spread it out—but payment plans often include small fees that add to your costs.

When you see $20 down, it means the insurer is allowing a very small first installment because they’re confident you’ll make future payments on time. They’re taking a calculated risk on you.

Here’s a specific numeric example:

Notice the pattern: the lower your down payment, the higher your subsequent monthly bill. You’re not saving money, you’re shifting when you pay it. And those installment fees add up. OCHO doesn’t charge installment fees.

In 2026, many online insurers let you choose between different down payment and installment combinations. You might see options like pay 10%, 20%, or a full month upfront, each with slightly different total costs. The flexibility is nice, but read the numbers carefully before celebrating that $20 down offer.

Say goodbye to huge, unfair deposits. Start your coverage with zero upfront costs today. And if a $0 deposit isn’t possible, we’ll make sure it’s as small and affordable as it can be. With OCHO, financial accessibility is a priority.

Life happens. We offer custom payment plans that match your budget, so you stay protected without financial stress. Choose between monthly or biweekly installments and enjoy peace of mind with a payment schedule that fits your needs.

No gimmicks, no fine print—just clear, transparent pricing and excellent service. OCHO ensures you know exactly what you’re paying for, with no unexpected costs or charges.

Get insured in minutes, not days, with a simple, streamlined process. Our process is fully online, making it simple to manage your policy anytime, anywhere—right from your phone. There’s no need to visit an office or deal with excessive paperwork.

No major insurer guarantees $20 down nationwide. Anyone who tells you otherwise is misleading you. But several carriers routinely advertise “low down” or “from $20” initial payments in selected markets for qualified drivers.

National carriers with low down payment options:

Non-standard and regional insurers:

For higher-risk or budget-focused customers, carriers like Direct Auto, Dairyland, The General, and various regional insurers in Texas, North Carolina, and the Midwest often focus on flexible payment plans. These companies may advertise low down payment options more aggressively, though monthly premiums tend to be higher.

Important note: availability changes by state, ZIP code, and time of year. A deal your friend got in March might not exist in June. Always check fresh 2026 quotes rather than relying on what someone else paid.

Direct-to-consumer online insurers generally offer the most flexible down payments compared with local agents tied to one carrier. Shopping online isn’t just faster—it often gives you more payment options to choose from.

Here's the thing about low down payment car insurance that the traditional insurance world doesn't want you to know: it gives you the power to break free from their ridiculous upfront payment demands. Why should you be forced to fork over your entire premium at once? That's backwards thinking from an industry that's been taking advantage of working people for way too long. Instead, you can spread that cost out with monthly installments or custom payment options that actually make sense for real people with real budgets. This approach makes car insurance accessible for drivers who refuse to drain their bank account just to get legal coverage.

Think about it - why aren't more insurance companies offering you flexible payment structures that work with your life? The good news is that some forward-thinking providers are finally getting with the program, offering monthly payments, quarterly options, or even pay-per-mile plans for those who don't rack up tons of miles. The smartest companies let you sync your payment date with your actual payday, so your insurance fits your budget instead of the other way around. You deserve payment options that work for you - whether that means smaller monthly chunks, a tiny down payment, or a custom schedule that matches how money actually flows in and out of your life.

When you take advantage of these flexible payment plans, you're not just getting car insurance - you're beating a system that was designed to keep your money tied up in their pockets. It's about time someone offered you the coverage you need without the financial stress of massive upfront demands. This is how smart people handle their insurance: they keep their cash flowing and their finances on track.

The fastest path to $20 down (or as close as you can get) is using online quote tools strategically. Walking into a local agent’s office and asking for “$20 down” won’t get you far. Here’s how to actually find these deals.

Step 1: Gather your information Before you start, have ready:

Step 2: Get multiple quotes within one day Insurance rates fluctuate. Get at least 5–7 quotes from different companies on the same day so you’re comparing apples to apples. Use each insurer’s direct website rather than just aggregator sites.

Step 3: Look for the “amount due today” line Most quote forms now show the initial payment separately from later installments. Don’t just look at the monthly estimate—find the specific “due today” or “first payment” amount for each quote.

Step 4: Toggle payment plan options Many insurers let you choose between different payment structures. Toggle between options to see how the “due today” amount changes. Sometimes switching from monthly to a different schedule reveals lower initial costs.

Step 5: Compare quotes and save screenshots Create a simple comparison of at least 3–5 companies, noting:

After you purchase a policy online, you can receive digital proof of insurance instantly. This digital proof is legally valid and can be used right away for car registration or to show coverage to lenders.

Concrete scenario: Entering a ZIP code in Ohio or Missouri in early 2026, choosing state-minimum liability coverage, and toggling payment plans until an option with $20–$40 down appears. It’s doable—but you need to actively look for it.

Many drivers assume that car insurance requires a hefty upfront payment due to outdated, traditional insurance carrier models. While most insurers still demand an initial payment, OCHO is changing the game by offering the world’s first truly no-deposit car insurance. By eliminating this financial hurdle, we make it easier than ever for drivers to secure affordable, reliable coverage. Here’s how it works:

Start by entering basic information about yourself, your vehicle, and your coverage needs. OCHO’s intuitive platform ensures a hassle-free process.

Select from affordable payment options designed to fit your lifestyle. Whether you prefer monthly payments or biweekly installments, OCHO has you covered.

Once approved, your policy becomes active immediately. There’s no waiting period, ensuring you’re protected as soon as you need it.

Here’s where we need to have an honest conversation. Chasing the absolute lowest down payment can lead to dangerously low coverage limits that won’t protect your assets after a serious crash. A $20 down payment isn’t worth it if you end up financially ruined after an accident.

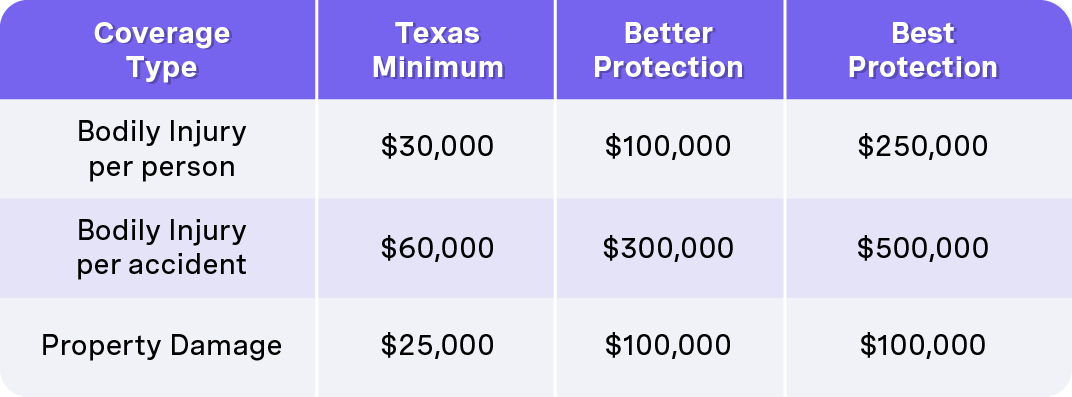

Understanding minimum vs. recommended coverage:

The minimum liability coverage might get you $20 down, but it leaves you personally liable for anything above those limits. If you cause an accident with $80,000 in medical bills and you only have $30,000 coverage, guess who pays the remaining $50,000? You do.

Example trade-off: A Texas driver could opt for minimum 30/60/25 coverage with $20 down versus 100/300/100 with a $60 down payment. That extra $40 upfront buys significantly more lawsuit protection.

For financed vehicles—say, a 2023 Toyota Camry under a bank loan—lenders typically require collision and comprehensive coverage. This makes $20 down payment car insurance extremely unlikely because full coverage auto insurance simply costs more. The lender will reject proof of insurance that doesn’t meet their requirements.

Never go below your state’s legal minimum just to chase a lower down payment. And if budget allows, consider adding medical payments, uninsured motorist coverage, and rental reimbursement. These add modest cost but provide real financial protection.

Here are realistic, high-level examples with approximate 2026 numbers:

Example 1: Georgia driver, low-cost scenario

Example 2: Florida driver, higher-cost reality

Florida’s minimum coverage requirements and higher insurance costs make $20 down nearly impossible, even for good drivers.

Example 3: Deductible adjustment impact

All figures are illustrative and will vary daily with underwriting updates and state filings. The point is to show what’s realistic versus what’s marketing fantasy.

Look, where you live plays a massive role in how much you'll fork over for car insurance—and whether that sweet $20 down payment car insurance is even within reach! State regulations basically dictate the minimum liability coverage you've got to carry, and guess what? These requirements can absolutely drive up the cost of your premium and your down payment. Think about it—states with higher minimum liability coverage? They're going to hit you with higher upfront costs for payment car insurance. It's that simple.

But here's the thing—it's not just the law that's working against you. Local factors like traffic congestion, crime rates, and even those crazy weather patterns can seriously impact your insurance rates. Texas drivers, for instance? They're getting slammed with higher insurance rates and down payments because of the state's massive population, those frequent storms that seem to never end, and higher accident rates that'll make your head spin! On the flip side, if you're lucky enough to live in states with fewer claims and lower risk, you might actually find it easier to qualify for that elusive $20 down payment car policy. Lucky you!

Want some real talk? Understanding your state's regulations and risk factors can absolutely help you find affordable car insurance options and set realistic expectations for your down payment. But don't just take our word for it—always compare quotes from multiple insurance providers in your area to make sure you're getting the best deal for your payment car insurance needs. Because why settle for getting ripped off when you don't have to?

Low upfront costs are appealing when cash is tight, but they come with trade-offs that can cost more over the policy term. Let’s be honest about both sides.

Benefits of very low down payments:

Drawbacks to consider:

In this example, the $20 down plan costs $40 more over 6 months than paying in full. That’s the real price of spreading out payments with low initial costs.

$20 down makes sense when:

$20 down doesn’t make sense when:

Here’s what nobody else tells you: a cancellation for non-payment appears on your insurance history and can make future down payments even higher. That $20 down you got today might cost you hundreds extra next year if you can’t keep up with the larger monthly payments and get canceled.

Getting affordable coverage isn't just about finding the lowest down payment—it's about beating the insurance game and unlocking every single discount you can get your hands on! Think about it: why should you pay full price when these insurance companies are sitting on a goldmine of discounts they're not even telling you about? Many auto insurance companies offer a variety of discounts that can help you qualify for lower premiums and make your payment car insurance way more budget-friendly. But here's the thing—you've got to know how to work the system.

Safe driving is one of the most common ways to save, and if you have a clean driving record, you'd better believe you should be getting those safe driving discounts! Students with good grades? Don't let them sleep on that discount—those insurance companies should be rewarding academic excellence. And here's where it gets good: bundling your auto insurance with other policies, like homeowners or renters insurance, can lead to some serious additional savings. Drivers with excellent credit also tend to qualify for lower premiums, which honestly should be the standard, not some special favor they're doing you.

Another way to absolutely crush your insurance costs is through usage based insurance programs. These programs track your driving habits—like how far and how safely you drive—and actually reward you with lower rates if you demonstrate responsible behavior. Revolutionary concept, right? By stacking these discounts like a pro, you can seriously reduce your insurance costs and make it way easier to afford the coverage you need, even if you're aiming for a low down payment or monthly payments. Don't let these insurance companies keep you in the dark—demand every discount you deserve!

Many readers will discover $20 down isn’t available in their state or for their risk profile. That’s okay—there are still real ways to reduce your upfront cost and get affordable car insurance.

Pay slightly more down for better terms: Instead of fixating on $20, consider $40–$80 down in exchange for better coverage or lower monthly payments. The difference may be manageable while still easing your cash flow. Sometimes an extra $30 upfront saves you $15 per month going forward.

Explore pay-per-mile or usage-based insurance programs: In 2026, carriers like Metromile (where available), Allstate’s Milewise, and Progressive Snapshot offer mileage based programs that can significantly lower total premiums for low mileage drivers. Lower premiums mean lower deposits. If you drive under 10,000 miles per year, usage based insurance programs might get you closer to that $20 down than traditional policies.

Check state-sponsored programs: California’s CLCA program offers affordable coverage for low-income drivers. Some states have community credit union partnerships that offer reduced deposits to qualifying residents. These programs exist—most people just don’t know about them.

Consider very short-term or non-owner policies: If you temporarily borrow cars or need a brief coverage bridge, monthly policies or non-owner policies can serve as a stopgap until your budget supports a more traditional policy with a higher down payment.

Bundle with homeowners insurance or renters insurance: If you have homeowners insurance or renters coverage, bundling with the same carrier often unlocks discounts that lower your auto premium and, by extension, your minimum deposit requirements.

If $20 down isn’t realistic today, here’s how to get there by your next renewal:

Pay all bills on time: Your credit report influences insurance rates in most states. Six months of on-time payments can meaningfully improve your credit-based insurance score. Reduce credit card balances where possible.

Maintain continuous coverage: The magic number is 201 days of continuous insurance coverage to move you from the high-risk box to the preferred customer box. Don’t let your policy lapse, even if it means keeping minimum coverage for a while.

Complete a defensive driving course: In states like Texas, New York, or Florida, approved courses yield 5–10% discounts and can lower both premiums and deposits. It’s a few hours of your time for years of savings.

Avoid tickets and at-fault accidents: Easier said than done, but safe driving is the single biggest factor in getting lower insurance rates and smaller initial payment requirements.

Reevaluate your vehicle: Before your next renewal, consider whether your current car makes financial sense. Trading a high-performance or luxury vehicle for a safer, cheaper-to-insure model can reduce both premiums and down payments.

Set a savings goal: Between now and your next renewal, aim to save $200–$300 specifically for your insurance deposit. A larger upfront payment unlocks lower monthly installments and often better coverage options.

Missing a payment on your car insurance? Brace yourself for some seriously unfair consequences. The Old Timers in the insurance industry will cancel your policy faster than you can say "grace period," leaving you completely exposed to financial disaster if you get into an accident. Why do they do this? Because the system is ridiculously broken and designed to punish people who are already struggling. A lapse in coverage doesn't just leave you vulnerable—it brands you as "high-risk" in their backwards system, making it much more expensive to get insured later. How is that fair?

Want to beat this rigged game? You need to stay one step ahead of these companies and their payment schemes. Many insurers offer automatic payment plans—and honestly, you should take advantage of them because missing even one payment can send you spiraling into their expensive penalty system. Some companies throw you a bone with a short grace period, but don't count on their generosity. The truth is, they're not looking out for you—they're protecting their own profits while you're left scrambling to avoid cancellation.

Here's what no one else will tell you: if you're struggling to keep up, don't wait until it's too late. Reach out to your insurer immediately—not because they care about you, but because it's better than letting them trap you in their high-risk penalty box. They might adjust your payment schedule or offer solutions, but remember, they're doing this to keep you paying, not out of kindness. The real truth? Keeping continuous coverage is everything. It's not just about protecting yourself on the road—it's about refusing to let the insurance industry label you as high-risk and charge you inflated rates for the rest of your life. Don't let them win.

Is true $20 down payment car insurance available in every state?

No, it’s not. $20 down is far more common in lower-cost states like Ohio, Indiana, and parts of Texas than in expensive markets such as Florida, Michigan, New York, or California’s major metro areas. State regulations, average claim costs, and regional insurers all affect what’s possible. If you live in a high-cost state, expect to pay significantly more upfront regardless of what national ads promise.

Can I get $20 down payment car insurance with bad credit or an SR-22?

Very unlikely. High risk drivers and those with SR-22 filing requirements almost always face higher upfront payment requirements. Many non-standard insurers will ask for 25–50% of the premium at sign-up because they view you as more likely to cancel or file claims. Focus on maintaining continuous coverage and improving your credit over 6–12 months to qualify for better terms at your next renewal.

Does a $20 down policy affect my coverage quality?

The deposit amount itself doesn’t change your coverage terms—$50,000 of liability is $50,000 whether you paid $20 down or $200 down. However, drivers chasing the absolute lowest down payment often choose bare-minimum limits that may be inadequate after a serious accident. The coverage you select matters far more than the payment structure you choose.

Can dealerships set up $20 down insurance for me when I buy a car?

Some dealerships connect buyers to partner insurance providers, which can be convenient. But the down payment amount still depends on underwriting—your driving history, credit, and the coverage required for your loan. Dealers cannot force a legitimate insurer to offer $20 down if you don’t qualify. Always compare quotes independently rather than accepting whatever the dealership offers.

How often should I re-shop my policy if I’m aiming for a lower down payment?

Check quotes at each 6- or 12-month renewal, after major life changes (moving ZIP codes, paying off a car loan, improving credit), and at least once per year even if nothing has changed. Insurance rates and payment options shift constantly. You might not qualify for $20 down today but could easily qualify in six months after building continuous coverage and improving your credit score.

Compare & get covered fast

Find and compare auto insurance in minutes, and get your free credit score.

Choose when you pay

Select payment dates that line up with your payday.

Manage everything in one place

Track your policy, manage payments, and request a payment extension right from your dashboard.

.svg)