Let’s clear something up right away: “dui car insurance” isn’t a special category of coverage you’ll find in any state’s insurance regulations. It’s a search term, a way for people to find auto insurance after getting a DUI conviction. Insurance companies simply treat you as a high risk driver and price your policy accordingly.

After a DUI (or DWI, OWI, or whatever your state calls driving under the influence), you generally must carry at least your state’s minimum requirements for liability coverage. These are the state's minimum requirements set by law, and SR-22 or FR-44 filings are official forms used to demonstrate that you meet these minimum coverage levels after a serious violation like a DUI. In some states, you’ll need to carry higher limits. Florida and Virginia, for example, require an FR-44 filing with significantly higher liability limits than the standard minimums.

The underlying policy types remain the same as for any driver: liability, collision, comprehensive, uninsured/underinsured motorist, and optional extras like roadside assistance or rental reimbursement. You’re not buying some special “DUI product.” You’re buying regular auto insurance coverage, just with a lot more scrutiny and a much higher premium attached.

One thing worth knowing: if you don’t own a vehicle but still need to meet state requirements to get your license back, some carriers offer “non-owner” SR 22 policies. The SR-22 or FR-44 is an official form filed with the state to prove you meet the required insurance coverage after a DUI. These provide liability coverage when you occasionally drive vehicles you don’t own, like rentals or borrowed cars.

Bottom line: “DUI insurance” equals standard auto coverage with higher prices and more hoops to jump through.

Here’s where things get real. When insurers see a DUI on your driving record, they immediately reclassify you as a high risk driver. The dui effect on auto insurance rates is significant, premiums typically spike sharply and this impact can last for three to five years, or even longer depending on your state and insurer. This directly drives up car insurance premiums and can limit which companies will even cover you.

The numbers are stark. As of 2024, national data shows average car insurance rates increase by 70%–90% after a single DUI. That translates to roughly $1,400–$1,800 more per year compared with someone holding a clean driving record. Research found that in California specifically, drivers face an average 186% increase, about $3,000 extra annually.

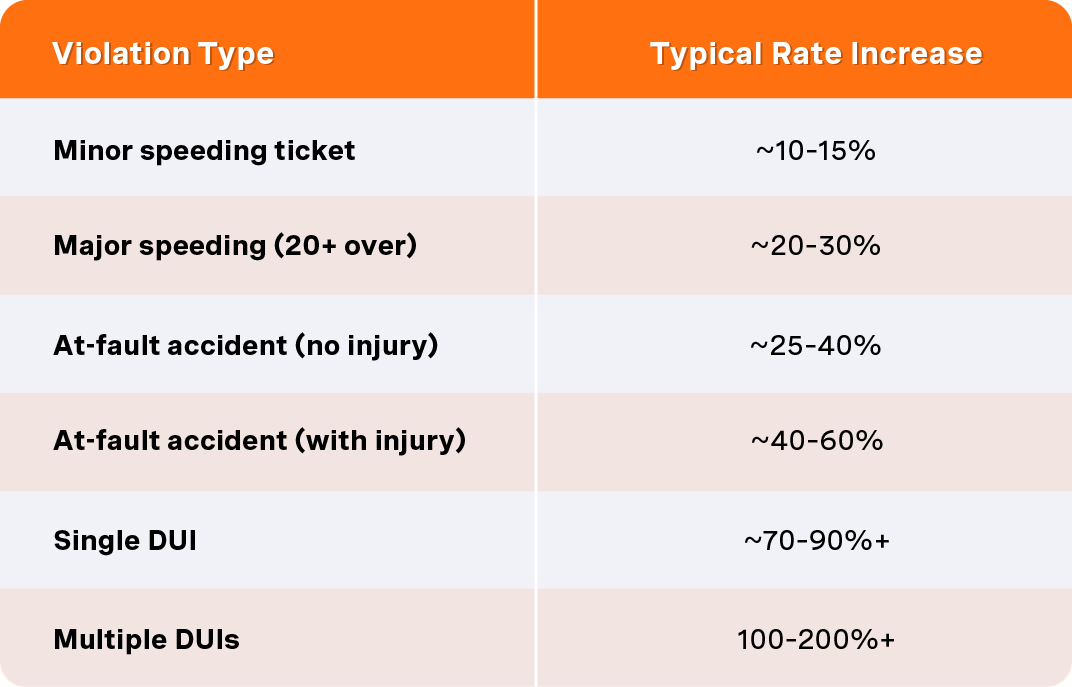

For underwriting purposes, a dui conviction is treated more severely than most other violations. Here’s how typical surcharges compare: For individuals without a personal vehicle, non owner car insurance may be relevant.

A DUI can also lead to non-renewal of your insurance policy, cancellation mid-term in some circumstances, or being shifted into your state’s high-risk (assigned-risk) pool. And the impact differs by state, smaller average increases have been reported in Florida and Alaska, while North Carolina drivers often see some of the most dramatic jumps.

Insurers also look at your age, prior traffic violations, claims frequency, and whether the DUI involved an accident. All of these factors compound to determine your final rate increase.

Getting a DUI sets off a chain of events that can feel overwhelming. Here’s a chronological overview from arrest through getting back on the road legally:

Immediate consequences (first 24–72 hours):

Court and sentencing phase (weeks to months): A first-offense DUI in many states can result in:

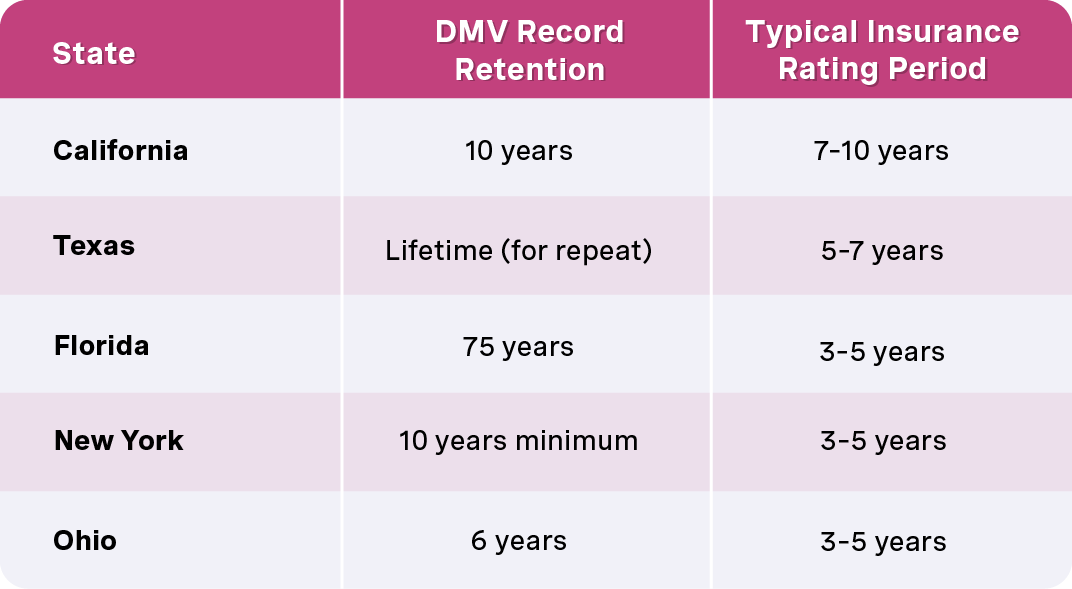

State-specific examples: California often imposes a 4-month license suspension for a first DUI, while Virginia may impose an immediate 7-day administrative suspension before further penalties are decided. Many states mandate SR 22 filings for three to five years.

Insurance impact timing: Once a DUI appears on your driving record and your insurer pulls your motor vehicle report (commonly at renewal), your premium can spike dramatically. Some drivers get non-renewed entirely and must find a new policy with a carrier willing to write high risk drivers.

States use different labels for essentially the same serious offense. Here’s the breakdown:

Some states distinguish offenses based on blood alcohol content or age. For example, drivers under 21 often face separate offenses with lower BAC thresholds like 0.02% instead of the standard 0.08%. A driver's BAC at the time of arrest is a key factor in determining the severity of the offense and can influence both insurance rates and legal requirements.

Here’s what matters for your car insurance costs: regardless of the label, any conviction involving driving with a driver’s BAC above the legal limit is treated as a major violation. Auto insurers don’t care whether your state called it DUI, DWI, or OWI, they all see it as a serious offense that dramatically elevates your risk profile.

An SR 22 is a certificate your insurer files with your state DMV proving you carry at least the state’s minimum liability coverage after a serious violation like a DUI. It’s not a policy, it’s paperwork that proves you have a policy.

The FR-44 is a stricter version used in only two states: Florida and Virginia. Under FR-44 requirements, you must carry significantly higher liability limits. In Virginia, for example:

How the process works:

To better understand why maintaining continuous coverage is important, read about the hidden costs of a lapse in insurance coverage.

The filing fee itself is cheap. The real cost comes from the higher insurance premiums you’ll pay while the filing is required. Most states require an SR 22 for about three years after a DUI, while FR-44 obligations in Florida or Virginia typically last 3–4 years depending on the case.

No single insurer is always the cheapest company for every driver with a DUI. But recent national data highlights some consistently competitive options worth checking. Rate differences are often company based, meaning that average rates and premium increases can vary significantly depending on the insurance company and how they assess DUI risk.

Based on 2024 average rates for drivers with one DUI seeking full coverage:

Rate changes after a DUI are not uniform across companies. Some insurers might raise rates only 20–30%, while others may double or triple them. This makes comparison shopping absolutely critical.

Availability notes:

Young drivers (ages 21–25): Younger drivers typically see the steepest surcharges after a DUI. Progressive often leads for 21- and 25-year-old DUI drivers compared with the national average. State Farm can also be competitive depending on your state.

Middle-aged drivers (around 40): Progressive and State Farm frequently emerge as competitive choices for 40-year-olds with a DUI. Erie, where available, often provides attractive rates for this age group.

Seniors (around 70): Progressive or Erie often rank among the lowest for 70-year-olds with a DUI. Some regional companies offer particularly good rates for older drivers with otherwise clean records.

Military members and veterans: USAA is known for competitive rates, but Progressive and other insurers sometimes still win on price. Always compare—don’t assume any single company is automatically cheapest.

State variations: The cheapest car insurance companies vary widely by location. Smaller regional carriers occasionally beat national brands, and local independent agents can identify lesser-known low-cost options for DUI drivers in your area.

Note: All figures are approximate 2024 averages for typical full-coverage policies and should not be considered guaranteed quotes.

While a DUI is the largest single factor driving up your insurance costs, insurers still consider your full risk profile when setting rates.

Common rating factors beyond the DUI:

Having multiple recent violations—like reckless driving, major speeding, or at-fault crashes—alongside the DUI can push you into very high-risk tiers or your state’s assigned-risk pool where auto insurance rates are even higher.

Even small but frequent comprehensive or collision claims can make a high risk driver appear more expensive to insure. Poor credit in states that allow credit-based scoring can compound the problem further.

The good news: improving everything you can control—mileage, vehicle choice, claims behavior, and maintaining continuous coverage—helps offset the cost of the DUI over time.

Here’s a practical path from conviction to being fully insured and back on the road legally:

Step 1: Confirm your court and DMV requirements

Step 2: Decide on owner vs. non-owner coverage If you own, lease, or have regular access to a vehicle, you need an owner policy. If you don’t own a car but need to satisfy DMV requirements, a non-owner SR 22 policy is typically cheaper and keeps you compliant.

Step 3: Gather your information Before calling or quoting online, have ready (and consider reading about gap insurance if applicable):

Step 4: Request quotes from multiple insurers Get quotes from at least 3–5 car insurance companies that explicitly write high-risk or SR 22 policies in your state. Include at least one national brand and one regional or specialty carrier.

Step 5: Confirm your SR 22/FR-44 filing Once you choose a new policy, have the insurer file the SR 22/FR-44 electronically. Confirm with your DMV that it’s been received before you resume driving, especially if you’re on a restricted license.

A DUI conviction doesn’t just affect your wallet, it can put your driving privileges and auto insurance coverage at risk. In most states, a DUI triggers an immediate suspension or revocation of your driver’s license, often lasting anywhere from 30 days to several years depending on your driving history and the severity of the offense. To get back on the road legally, you’ll typically need to meet your state’s minimum insurance requirements and provide proof through an SR-22 or, in some states like Florida and Virginia, an FR-44 certificate.

Insurance companies view drivers with a DUI conviction as high risk, which means you’ll likely see a significant rate increase, often 60% to 90% above the national average for drivers with a clean record. Some insurers may even choose to non-renew your policy, forcing you to seek coverage from companies that specialize in high-risk or DUI insurance. These companies understand the unique challenges faced by drivers with a DUI on their record and can help you find the coverage options you need to stay legal.

During your license suspension, you may be eligible for a restricted license, which allows you to drive to essential destinations like work or school. However, most states require you to install an ignition interlock device in your vehicle, which checks your blood alcohol content (BAC) before the car will start. This device is an added cost, but it’s often a necessary step to regain your driving privileges and maintain continuous insurance coverage.

There are three separate “clocks” running after a DUI:

Even when the DUI technically remains on file longer, the extra premium impact usually diminishes if you maintain a clean record, carry continuous auto coverage, and avoid claims.

Important note on expungement: Record sealing or expungement (where available) usually does not erase the incident from insurance rating for the period insurers are allowed to consider it. A DUI stays visible to auto insurers even if it’s no longer on your criminal record.

You likely can’t avoid a significant rate increase immediately after a DUI. But you can meaningfully reduce what you pay compared with doing nothing.

Shop around regularly: Comparison shopping at renewal every 6–12 months is essential for the first few years after conviction. Different carriers change their appetite and pricing for DUI drivers over time. The cheapest company today might not be cheapest next year.

Adjust your coverage strategically:

Take approved courses: Completing a defensive driving course or state-approved DUI education program can qualify you for discounts with some insurance companies. Ask your insurance provider what’s accepted.

Maintain perfect payment and coverage history: Late payments and coverage lapses can push you into even higher-risk tiers. Continuous coverage is one of the fastest ways to rehabilitate your driving history in insurers’ eyes.

Try OCHO for flexible payments: With a low down payment, and easy installments, you could get a custom plan that’s much more manageable.

An ignition interlock device (IID) is a breath-test unit wired to your vehicle’s ignition system. It prevents the engine from starting if your blood alcohol content is above a preset limit—usually 0.02% or 0.025%.

When courts or DMVs typically require an IID:

Does an IID lower your car insurance premium? Generally, no. Having an IID doesn’t directly reduce what you pay. However, it may be required for you to legally drive at all while your SR 22 or FR-44 is in force. Without it, you might not be able to maintain coverage—which creates bigger problems.

Additional IID costs to budget for:

Some insurers consider successful IID completion as a positive factor when reevaluating your risk over time. It demonstrates you’re taking rehabilitation seriously.

Do I have to tell my insurance company about my DUI right away? If you're exploring different insurance options after a DUI, consider learning about pay as you go car insurance with no deposit for flexible, low-cost coverage solutions.

Laws rarely require immediate self-reporting. However, your insurer will typically learn of it at renewal when they pull your driving record, or sooner if you need an SR 22 filed. Failing to disclose when directly asked on an application can lead to policy cancellation for misrepresentation, which makes finding new coverage even harder, and may expose you to additional penalties and consequences.

Can I get car insurance if I have multiple DUIs?

Yes, but your options narrow significantly. Coverage is often only available through high-risk specialty insurers or your state’s assigned-risk pool, with much higher premiums. Working with agents who specialize in non-standard or DUI-focused coverage is your best bet. Expect to pay substantially more than after one DUI.

Will my policy cover a crash that happened while I was driving drunk?

Liability coverage usually still pays for injuries and property damage you cause to others, up to your policy limits. However, the insurer may non-renew you afterward, and you remain personally responsible for any amounts exceeding your limits. Some policies may restrict coverage for damage to your own vehicle depending on specific exclusions. Either way, expect your insurance policy to become much more expensive or get cancelled after the claim.

Can an SR 22 or FR 44 be filed without buying a new policy?

No. You must have an active qualifying auto or non-owner policy for your insurer to file an SR 22 or FR-44. The certificate proves you have coverage—it can’t exist on its own. If your current insurer won’t file one (many standard insurers won’t), you’ll need to switch to a company that specializes in high risk drivers.

What happens if my DUI is reduced to a lesser charge?

If a DUI is pled down to reckless driving or another lesser offense, insurers may still see a serious violation depending on how it appears on your motor vehicle record. A “wet reckless” (alcohol-involved reckless driving) is still treated as a major violation by most auto insurers. Ask your agent how the final charge codes in your state’s database before assuming your rates will be dramatically lower.

Getting dui insurance isn’t fun, but it’s absolutely doable with the right approach. The drivers who save the most are the ones who shop aggressively, maintain continuous coverage, and steadily rebuild their driving record over time.

Start comparing quotes from multiple car insurance companies today. Every month of clean driving gets you closer to normal rates again—and the sooner you lock in coverage, the sooner that clock starts running.

Compare & get covered fast

Find and compare auto insurance in minutes, and get your free credit score.

Choose when you pay

Select payment dates that line up with your payday.

Manage everything in one place

Track your policy, manage payments, and request a payment extension right from your dashboard.

.svg)